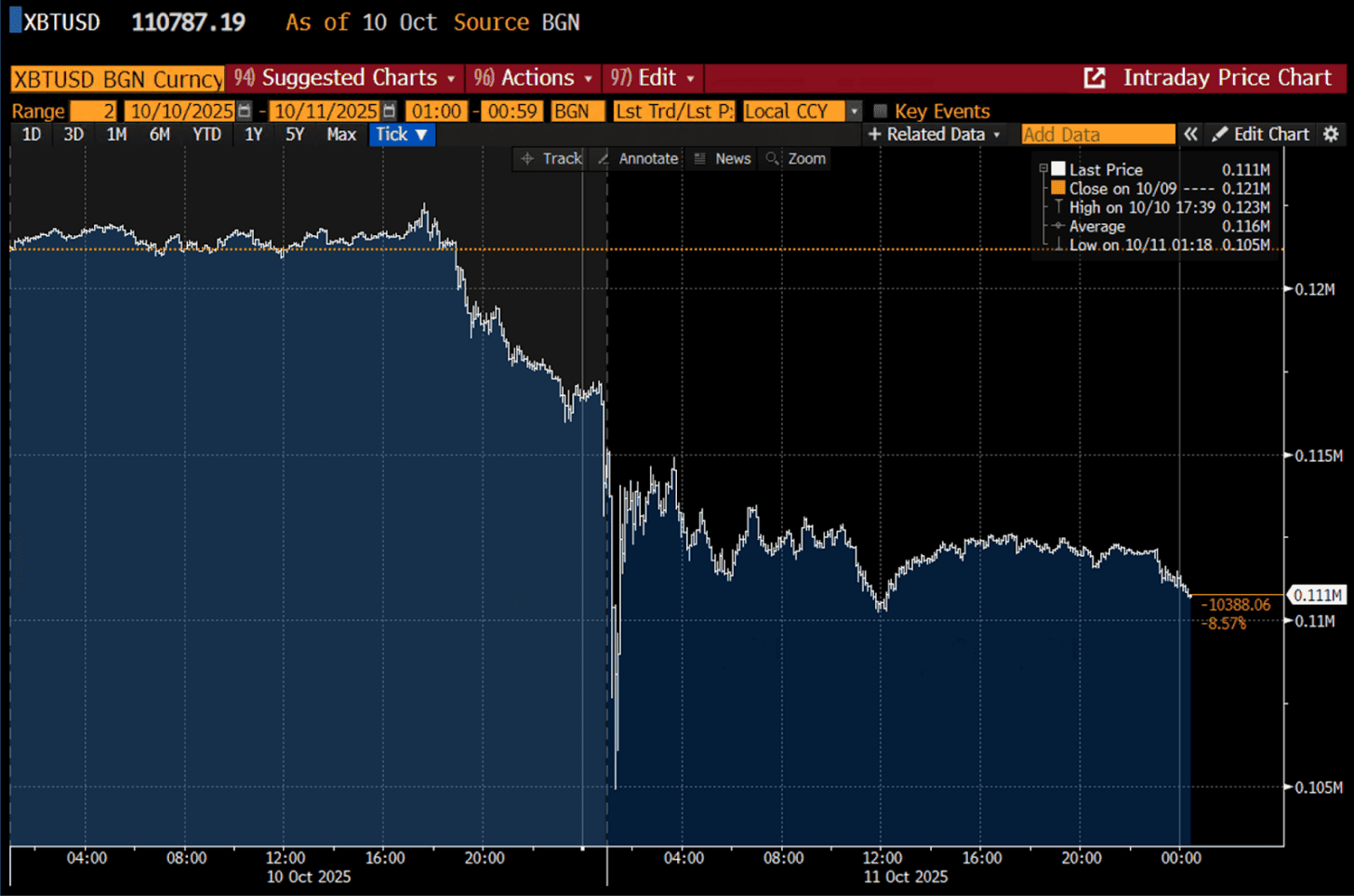

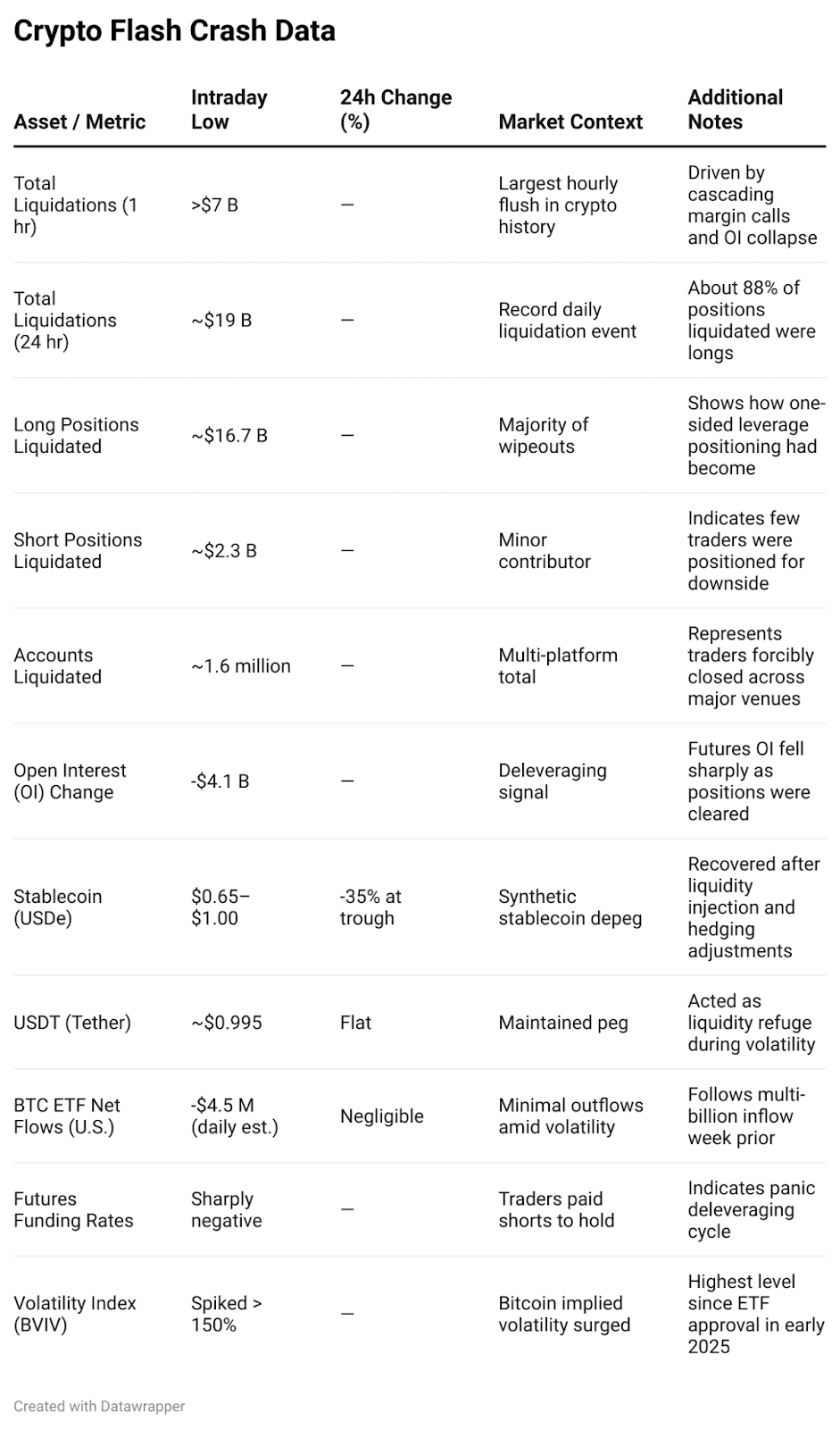

Bitcoin plunged into a violent selloff late Friday, printing as low as $101,000 on some venue, and wiping out nearly $7 billion of leveraged positions within an hour. Over a 24-hour window, total liquidations swelled to $19 billion, the largest on record, according to multiple derivatives trackers.

The spark was political, not technical. A surprise announcement from U.S. President Donald Trump pledging 100% tariffs on Chinese imports and new export controls on “critical software” reignited trade war fears and knocked risk assets globally.

For GCC and UAE investors accessing crypto through U.S. spot Bitcoin ETFs, European exchange-traded products (ETPs), or the Nasdaq Dubai-listed 21Shares Bitcoin ETP (ABTC), the event became a live stress test of product structure, liquidity, and market plumbing.

What Just Happened

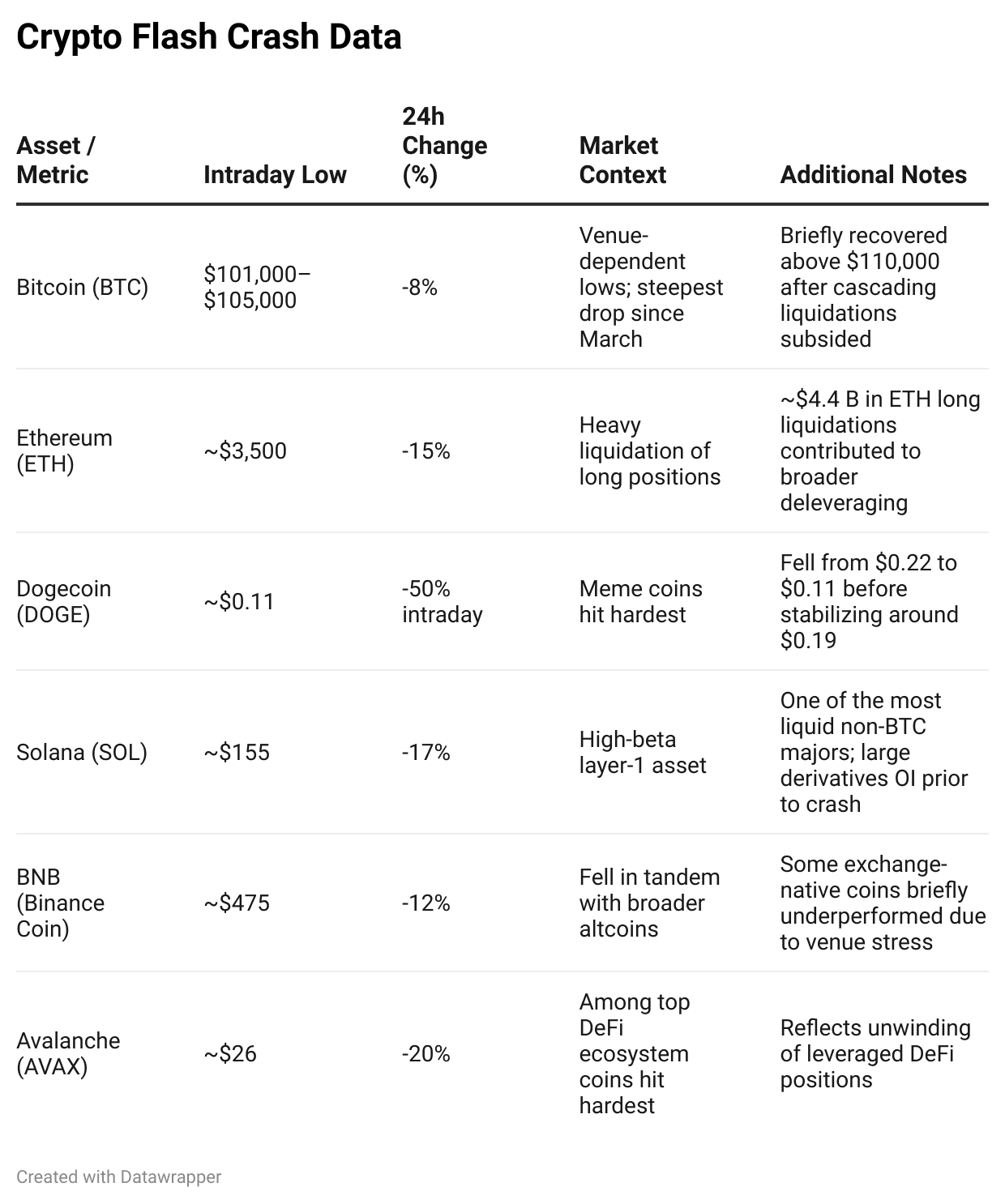

Bitcoin fell sharply on Friday, dropping roughly 8% to around $105,000 by evening trading, with some exchanges recording trades as low as $101,000 during the worst of the selloff. Ethereum (ETH) tumbled more than 15%, and Dogecoin (DOGE) briefly lost half its value before stabilizing near $0.19 as panic subsided.

The rout triggered a cascade of forced liquidations, with more than $7 billion in leveraged positions wiped out within an hour and nearly $19 billion cleared over the full day, the largest single-day washout in the modern crypto era.

Even the stablecoin complex showed strain, as Ethena’s yield-bearing token USDe briefly depegged to about $0.65 on major exchanges before recovering toward its $1 target.

Definitions:

Liquidations are forced closures of leveraged trades when margin is insufficient.

Open Interest (OI) measures the number of outstanding futures and options contracts, a key indicator of leverage in the system.

Why It Happened: Tariffs, Leverage, and a Crowded Derivatives Market

The immediate trigger was clear, a sudden escalation in the U.S.–China trade tensions. The tariff threat sent shockwaves through global risk assets, with equities tumbling and investors rushing into safe havens. Crypto, burdened with historically high leverage, exaggerated the move.

As Bitcoin slid from around $126,000 to below $120,000, open interest fell by more than $4 billion, signaling a mass deleveraging. The cascade resembling classic “leverage resets” seen in previous crypto cycles is painful at the moment but sometimes healthy for long-term price stability.

Options activity likely compounded the decline. In recent months, options open interest has rivaled futures exposure, creating hedging feedback loops where selling accelerates into weakness.

ETF and ETP Angle: The Wrappers Held, but the Plumbing Was Tested

In the week leading into the crash, U.S. spot Bitcoin ETFs saw multi-billion-dollar inflows, underscoring strong institutional participation. Early data suggests Friday saw only a modest net outflow of a few million dollars across the U.S. ETF cohort, which is negligible compared with the scale of derivatives liquidations. Still, those flow numbers remain subject to later revision.

For regional investors, 21Shares’ physically backed Bitcoin ETP (ABTC) remains the flagship product listed on Nasdaq Dubai. The delisting of 3iQ’s Bitcoin Fund (QBTC) earlier this year reduced the number of locally listed crypto products, even as offshore ETF volumes expanded dramatically.

GCC and UAE Investor Lens: Five Practical Implications

- UCITS vs. U.S. ETFs

Most European crypto products are structured as ETPs or exchange-traded commodities (ETCs), not UCITS funds. They are debt securities with physical crypto backing, while U.S. spot Bitcoin ETFs are trust-like vehicles regulated under U.S. investment laws. Product rules, disclosures, and collateral models differ widely.

- Tax and Estate Exposure

Holding U.S.-domiciled ETFs can expose non-U.S. investors to U.S. estate tax. While crypto ETFs rarely pay dividends (so withholding tax is minimal), estate exposure remains a factor. Many international investors prefer Irish, Swiss, or Channel Islands-domiciled ETPs to mitigate this.

- Local Access

Nasdaq Dubai’s ABTC offers trading in regional hours with AED settlement through local brokers, a valuable feature when volatility strikes during U.S. market closures.

- Regulatory Framework

Dubai’s Virtual Assets Regulatory Authority (VARA) continues to expand its licensing regime. Institutional service providers, such as BitGo, have secured brokerage and custody licences, improving the region’s infrastructure for professional crypto participation.

- Sharia Considerations

Most crypto ETPs do not carry formal Sharia certification. Interpretations vary among scholars regarding the permissibility of holding or trading digital assets. Institutional allocators often seek bespoke guidance or third-party opinions.

What Broke (and What Didn’t)

Stablecoins Blinked: USDe’s brief collapse to $0.65 highlighted the fragility of synthetic dollar models that rely on derivatives and collateral efficiency rather than full reserves. Though the peg recovered, the episode will reignite scrutiny of design, collateralization, and liquidity management.

Exchanges Strained but Stayed Up: Trading venues reported intermittent slowdowns as volumes spiked, but derivatives markets largely remained operational. The liquidation engines, however, ensured the deleveraging continued at full speed.

Derivatives Did the Damage: The bulk of the turmoil stemmed from leverage unwinding, not from spot selling. Billions were erased from futures open interest as traders’ margin positions were forcibly closed. Once liquidations ran their course, volatility began to subside.

Reading the Data with Caution

The data surrounding Friday’s crypto crash should be interpreted with care. Intraday lows varied by several thousand dollars across exchanges, a reflection of the market’s fragmented structure and inconsistent price discovery during periods of extreme volatility. ETF flow figures released immediately after the event are also preliminary, as issuers typically revise these numbers once daily settlements are finalized. Even stablecoin data require caution, depeg events can differ significantly by venue and trading pair, meaning that most reported prices are indicative rather than definitive snapshots of the broader market reality.

Lessons from the Flash Crash: A Macro Jolt in a Leverage-Driven Market

For GCC and UAE investors, the sudden selloff was a vivid reminder that crypto’s biggest risks often stem from macro events, not technology. A single policy headline magnified by excessive derivatives leverage was enough to trigger a historic wave of liquidations across exchanges.

Exchange-traded funds (ETFs) and products (ETPs) provided orderly access but could not buffer investors from the violent price swings. Even so, steady inflows earlier in the week pointed to a deep and continuing institutional appetite for Bitcoin exposure.

With only the 21Shares Bitcoin ETP (ABTC) listed on Nasdaq Dubai, regional investors still depend largely on offshore ETFs to gain regulated exposure, underscoring the importance of expanding local listings and market depth.

More broadly, the episode highlighted a crucial reality: Bitcoin had just set new all-time highs above $125,000, buoyed by record ETF inflows, before a single macro shock erased weeks of gains in minutes.

It was not a failure of crypto’s foundation but a demonstration of how global sentiment and leverage interact in real time. As the dust settles, one clear takeaway emerges for regional allocators. The future of digital assets will be shaped as much by macro policy and market structure as by innovation itself.