The launch of the KraneShares Wahed Alternative Income Index ETF (Ticker: KWIN) brings a rare offering to the GCC ETF market: a Shariah-compliant income strategy that doesn’t rely on Sukuk, dividends, or traditional fixed income. Instead, KWIN generates income through an options overlay on a portfolio of Shariah-screened U.S. equities—making it less a conventional ETF and more a listed structured strategy.

The KraneShares Wahed Alternative Income ETF is a Shariah-compliant fund that seeks to implement an option strategy to generate options income. KWIN is designed for investors seeking option income or alternatives to earning traditional interest. The fund is issued by KraneShares and subadvised by Wahed Invest LLC.

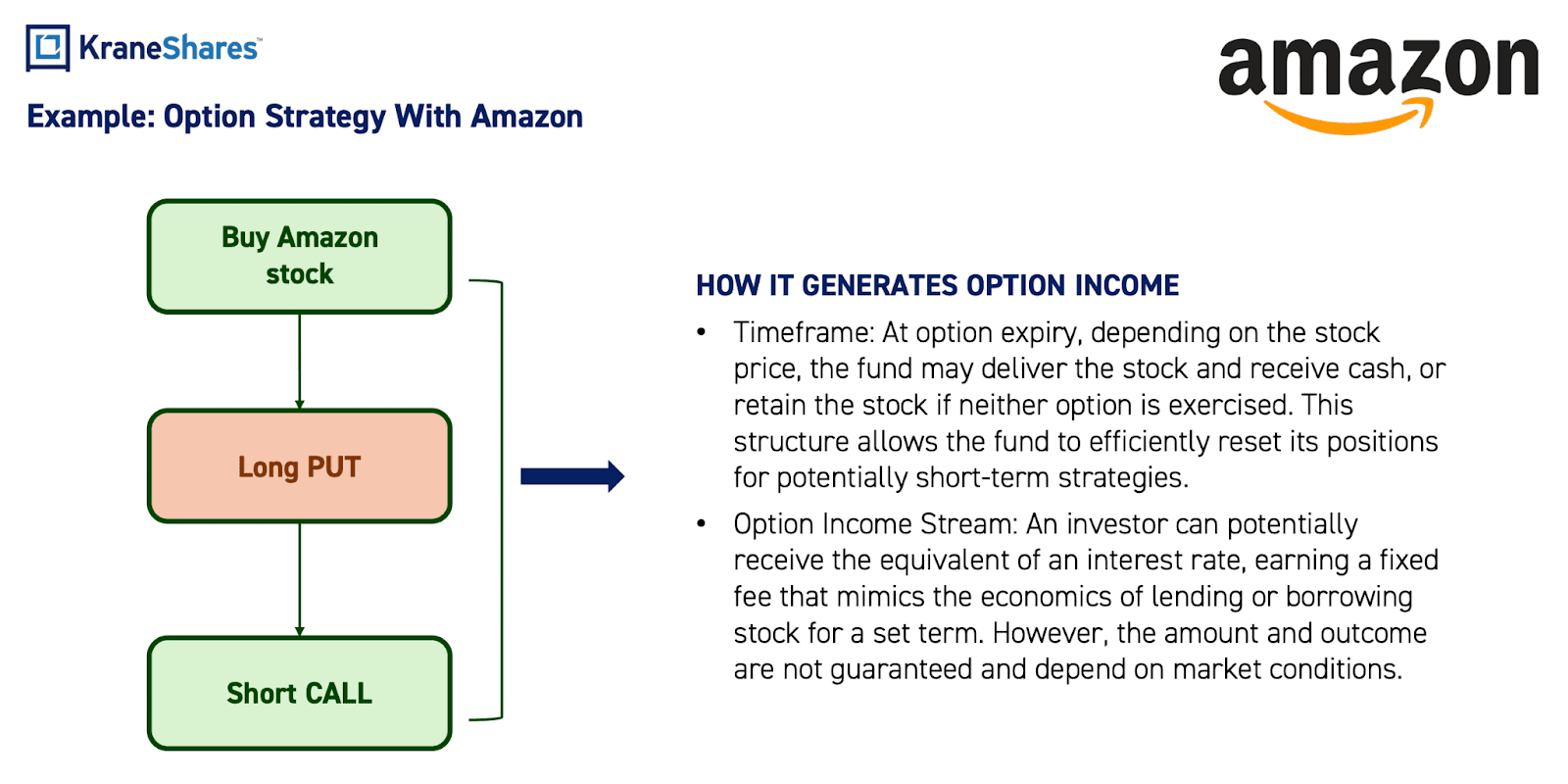

Here is an overview of the strategy

- The IOP will be from April 15th to the 21st, and listing on ADX shortly after

- An options-based Shariah-compliant strategy that aims to deliver ~5% per year

- The fund goes long US equities, long a put option, and short a call option

- Income is accumulated, not distributed, for tax reasons

- Investors can sell the accumulated shares monthly to generate tax-free income

- Strategy is managed by Kranshares and Wahed Invest

The strategy is designed to produce a delta-neutral outcome, meaning the overall portfolio is intended to be less sensitive to changes in the price of the underlying stocks, while generating a target income of 5% per annum from the option overlay.

How the ETF Is Structured

Structurally, KWIN is best understood as a three-layer product.

1. The equity sleeve

First, the fund holds a basket of Shariah-screened U.S. equities. These are non-dividend-paying securities reviewed by Wahed for compliance. This sleeve gives the ETF its permissible investment base and keeps it aligned with Islamic finance principles as interpreted within the index framework.

2. The options overlay

Second, KWIN overlays listed options on those stocks. For each long stock position, the fund writes a call and buys a put. This is the mechanism that converts a growth-oriented stock basket into an income strategy. Rather than collecting interest or coupon payments, the fund monetises volatility and option pricing.

3. The ETF wrapper

Third, all of that sits inside an ETF. That means investors can buy and sell it intraday on the exchange, get daily transparency, and access an options-based income strategy without having to build collars themselves on dozens or hundreds of individual stocks. That is a meaningful point of access. Strategies like this have historically lived in private banks, structured notes, or bespoke mandates. KWIN puts one into a listed fund format.

Here is an example

KWIN uses what is effectively a collar strategy on each selected stock. The fund buys the stock, sells a call option against that position, and buys a put option on the same stock. The income comes from the spread between the premium received from the short call and the premium paid for the long put.

This matters because it changes the source of return. In a normal equity ETF, investors mostly depend on capital appreciation, and sometimes dividends. In KWIN, the return engine is different. The equity position provides the underlying exposure, but the options overlay is designed to turn that exposure into a stream of alternative income. The short call helps generate premium income, while the long put provides downside protection. In broad terms, the fund is sacrificing some upside in exchange for a more controlled return profile.

KWIN vs. Sukuk

Risks: Sukuk fund vs KWIN

- Sukuk funds: EM credit and political risk, rate/duration risk, sector and oil‑exporter concentration, and liquidity risk.

- KWIN: Options‑strategy risk (roll, execution, path‑dependence).

Net‑net: sukuk funds behave more like Investment Grade (IG) EM bond portfolios with Shariah overlay, while KWIN behaves like a delta-neutral Sharia-compliant U.S. equity basket with a systematic options‑income engine on top.

Top 10 Holdings

The underlying equity sleeve is made up of non-dividend-paying, U.S.-domiciled securities reviewed for Shariah compliance. As of late February, the fund’s largest positions were concentrated in high-quality U.S. growth names rather than classic income stocks.

That holdings list tells an important story. KWIN is not sourcing income from mature, dividend-heavy sectors like utilities, banks, or telecoms. In fact, because of its Shariah framework, the eligible universe excludes financial companies and interest-paying bonds, which narrows the opportunity set. Instead, the fund owns growth-oriented stocks and seeks to extract income from option premiums, not from the businesses’ cash distributions.

Why the Structure Is Unusual

Most income products make a relatively simple promise: own bonds, own dividend stocks, or sell covered calls. KWIN is more specialized. It combines Islamic screening, growth equities, and a derivatives overlay in one structure. That is unusual enough in the U.S. ETF market; it is even more notable from a GCC perspective, where income products are still heavily associated with Sukuk or cash-like instruments.

The trade-off is straightforward. KWIN may provide a more stable source of income than a pure equity fund, but investors are giving up some upside because the call options cap gains above certain strike prices. At the same time, the protective puts are not free; they have to be paid for, and the strategy works only if the option premium captured is attractive enough relative to the cost of protection. The fund also uses FLEX options, which can be less liquid than standard listed options.

What Investors Should Watch

The design of KWIN is significant. It shows how the ETF wrapper is evolving beyond passive market exposure and increasingly being used to deliver engineered outcomes. For GCC investors in particular, it also signals that Shariah-compliant investing is moving into more sophisticated territory. KWIN is not simply another halal equity fund. It is a listed, liquid, rules-based income strategy for investors who want something other than interest and something more dynamic than Sukuk.