When headlines say “oil is up” or “oil is down,” they are referring to benchmarks, not a single global price. WTI, Brent, and regional grades such as Oman, Dubai, and Murban each reflect different parts of the market, while Saudi pricing adds another layer through official selling prices, making oil far more complex than a single number.

Why Oil Has Multiple Prices

Oil is not a uniform commodity, and that is why it does not have a single global price. Differences in pricing come down to three key factors: quality, location, and market structure. Some types of crude oil are lighter and contain less sulfur, making them easier and cheaper to refine into fuels such as gasoline and diesel. Location also matters, as oil stored inland behaves differently from oil that is readily available for global shipping. Finally, pricing mechanisms vary, with some benchmarks driven by highly liquid futures markets and others by physical cargo transactions. Together, these factors explain why oil prices can move in different directions at the same time.

WTI: The U.S. Benchmark

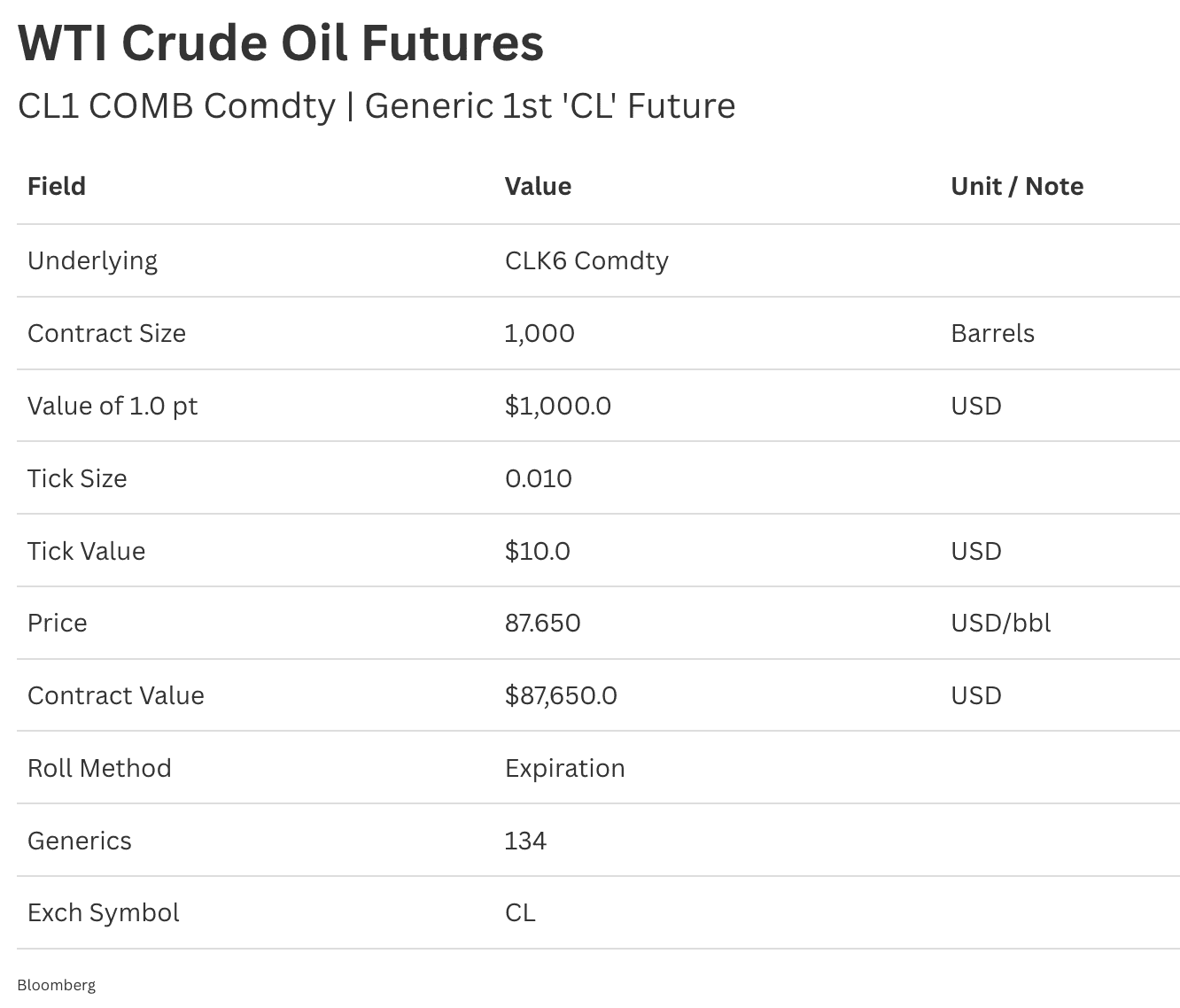

West Texas Intermediate (WTI) is the main oil benchmark in the United States. It is traded through futures contracts and delivered in Cushing, Oklahoma, one of the country’s key storage and pipeline hubs. WTI is considered a high-quality crude because it is light and low in sulfur, making it relatively easy to refine.

Its price is largely influenced by domestic factors such as U.S. production levels, inventory data, and pipeline infrastructure. As a result, WTI often reflects conditions in the American energy market more than global shipping dynamics.

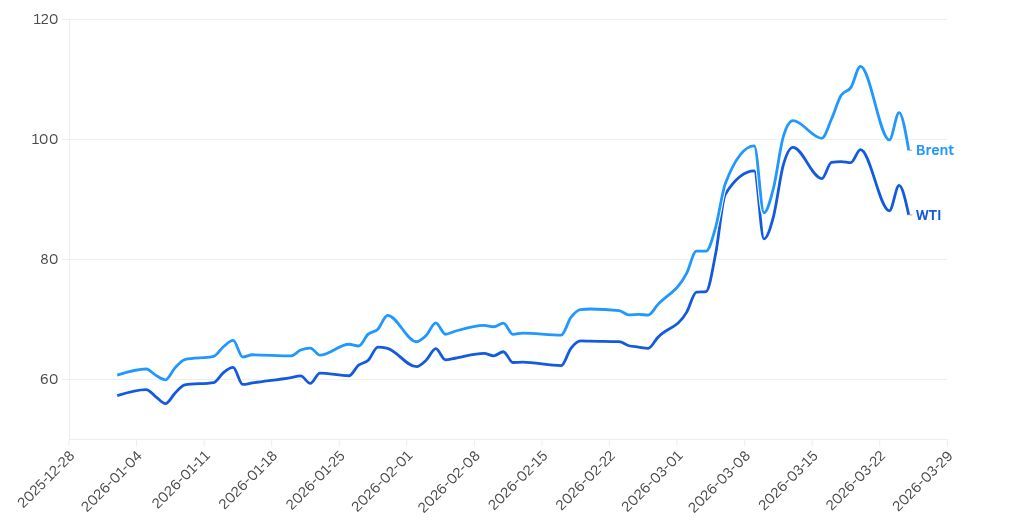

Brent: The Global Benchmark

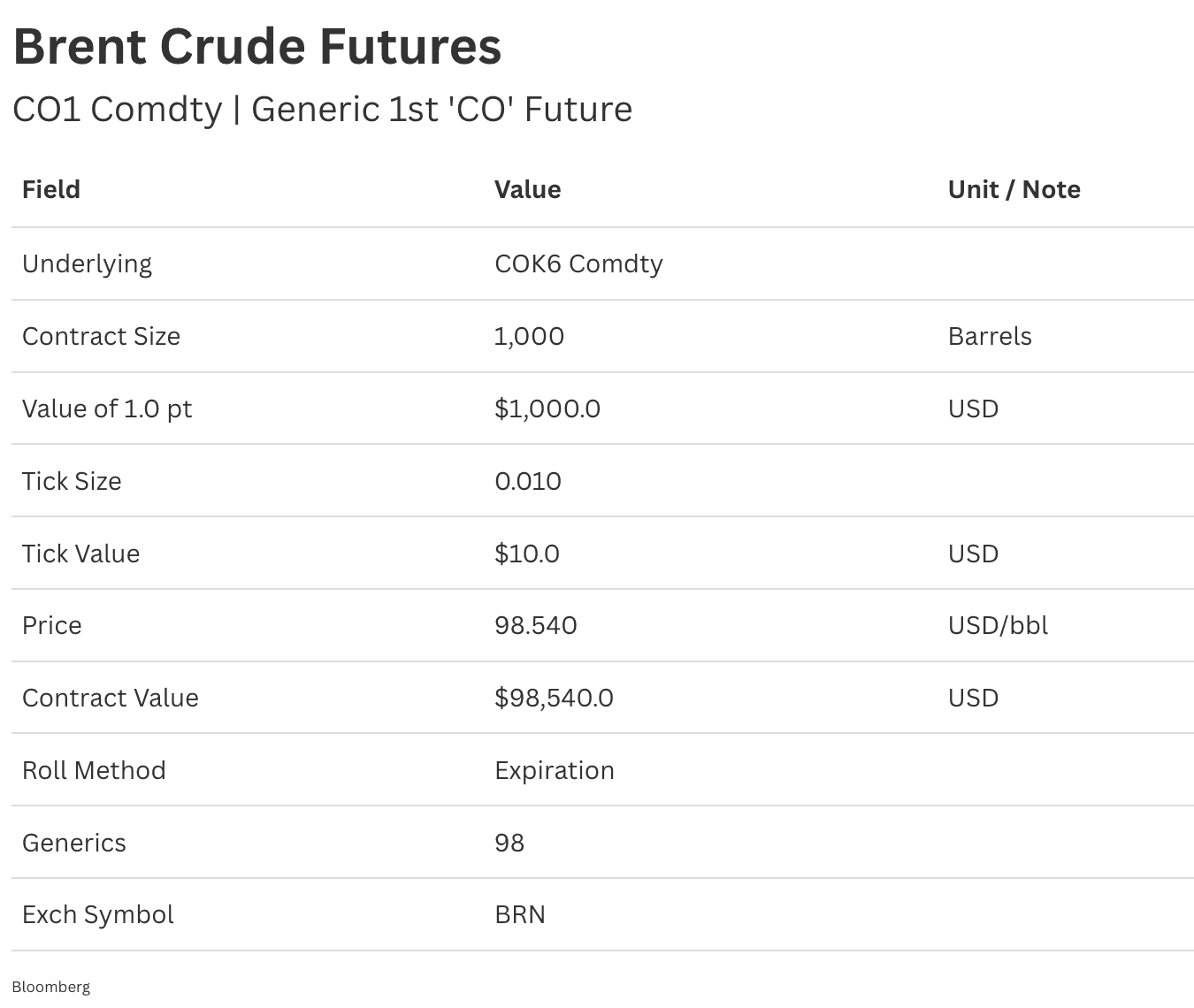

Brent crude is the most widely used international oil benchmark and serves as the reference price for much of the world’s traded oil.

It is based on production from the North Sea and is used to price crude exports across Europe, Africa, and large parts of Asia. Unlike WTI, Brent is more exposed to global supply chains and maritime routes, making it highly sensitive to geopolitical developments and disruptions in shipping. In simple terms, while WTI reflects the U.S. market, Brent captures the broader dynamics of global oil trade.

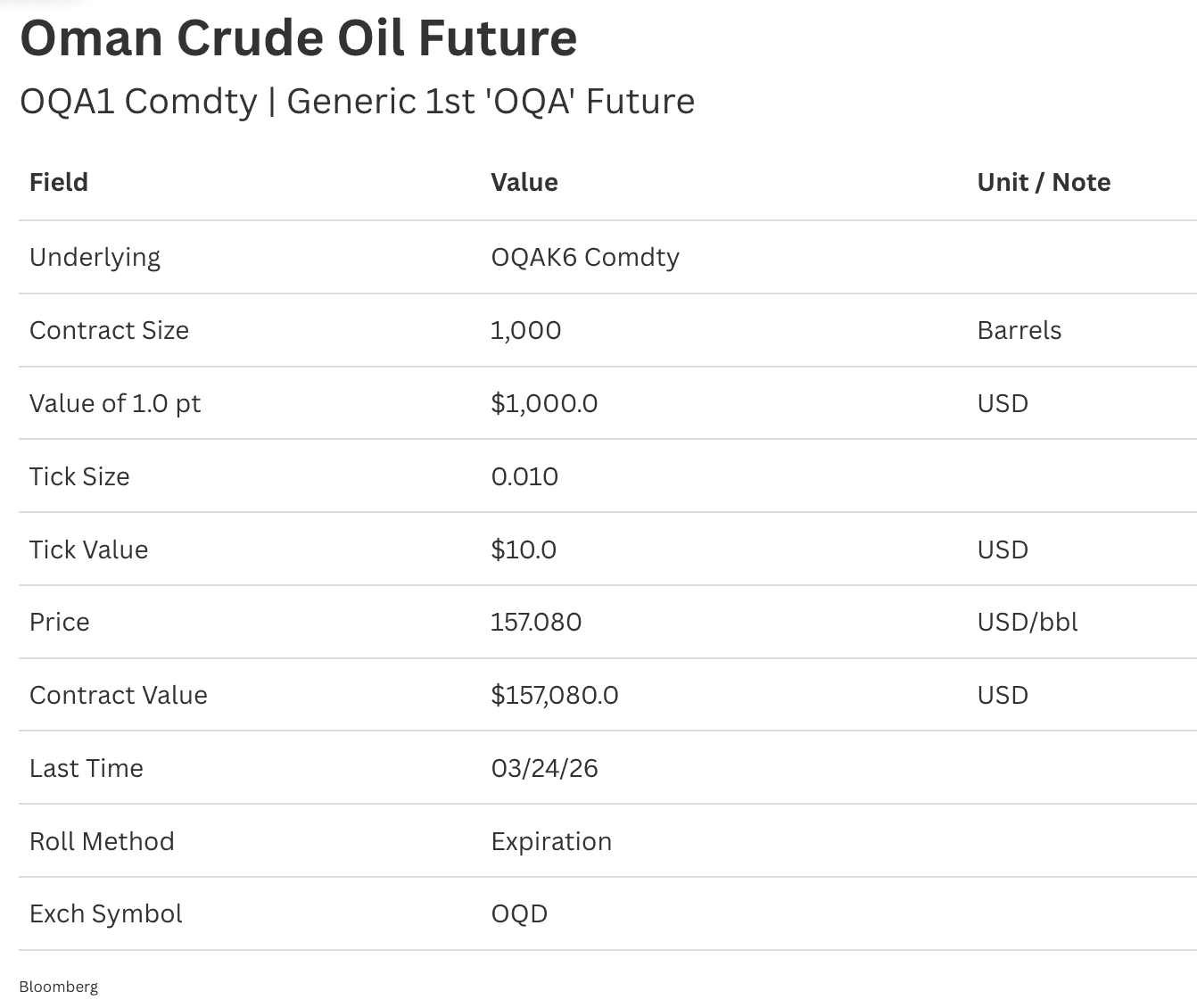

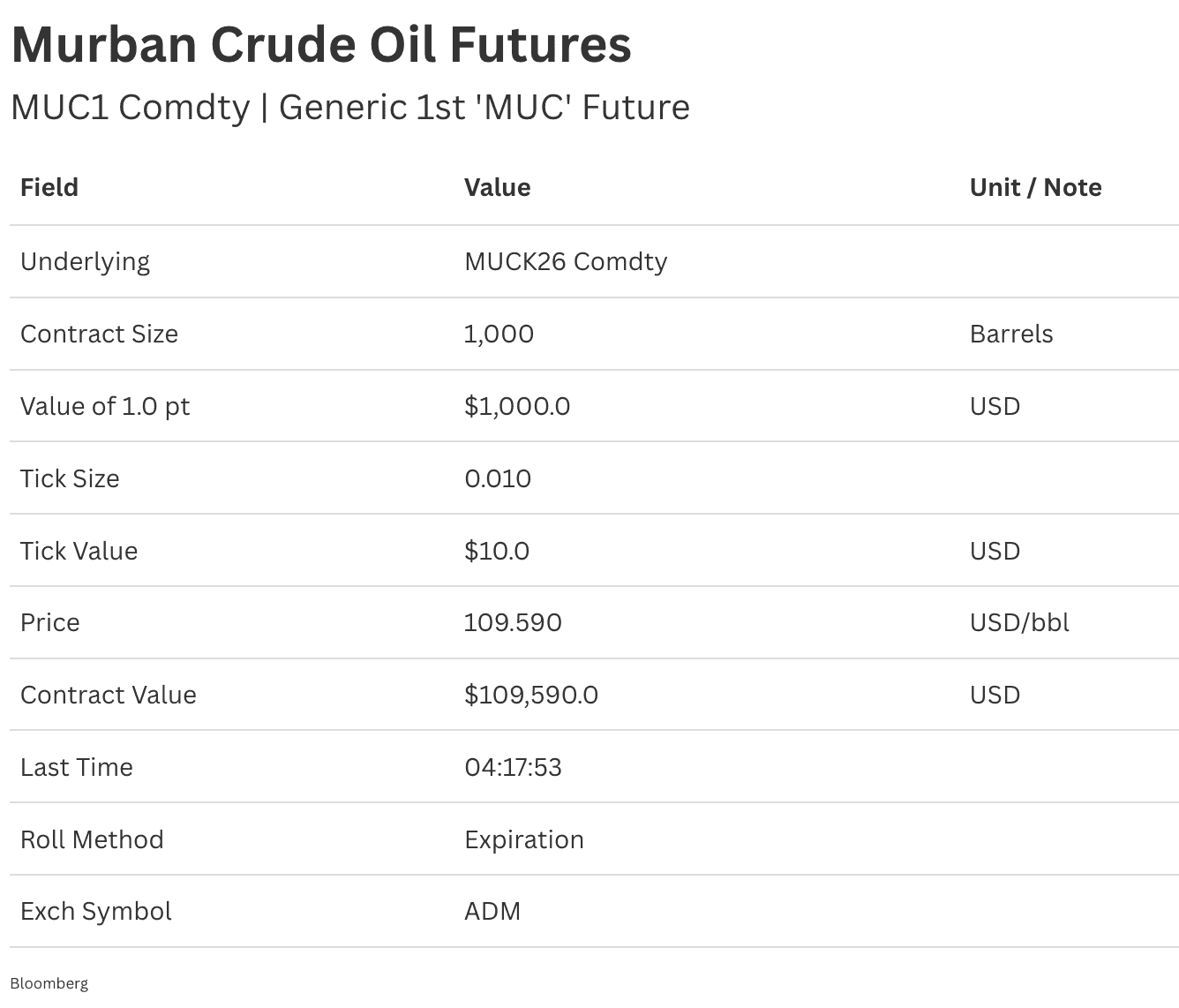

Oman, Dubai, Murban and Saudi Crude: The GCC Benchmarks

For GCC investors, oil pricing is not defined by a single benchmark but by a group of regional grades that reflect how crude is actually produced and exported across the Gulf. The most important are Oman, Dubai, Murban, and Saudi crude, all of which play distinct roles in pricing flows to Asia, the region’s largest customer base.

Oman crude is actively traded through futures contracts, making it one of the most transparent benchmarks in the region and widely used for hedging and pricing. Dubai crude, by contrast, is primarily based on physical cargo pricing and remains a key reference for Gulf exports, closely tied to real-time supply and demand conditions.

In the UAE, Murban crude has emerged as a major benchmark, supported by futures trading on Abu Dhabi’s exchange infrastructure. It represents a light, export-ready grade and is increasingly used as a pricing reference for Asian buyers, adding a more liquid and market-driven layer to regional pricing.

Saudi Arabia, the region’s largest producer, does not rely on a single traded benchmark in the same way. Instead, it sets official selling prices (OSPs) for its crude, typically priced relative to Oman and Dubai benchmarks. This pricing power means Saudi oil plays a central role in shaping regional spreads and market direction.

Together, these benchmarks provide a comprehensive picture of oil flows from the GCC to global markets, particularly Asia, and reflect both physical trade realities and evolving financial markets in the region.

Why These Benchmarks Diverge

Even though all these benchmarks track crude oil, they reflect different parts of the global market and therefore do not move in the same way. WTI crude oil is primarily driven by U.S. supply, storage, and infrastructure, making it more sensitive to domestic dynamics. Brent crude oil reflects seaborne global trade and reacts more directly to geopolitical events and shipping disruptions.

In contrast, GCC-linked benchmarks including Oman, Dubai, and Murban are tied to Middle East exports to Asia, the largest demand center for the region’s crude. These benchmarks are closely linked to physical cargo flows and strategic routes such as the Strait of Hormuz. During periods of disruption, they can move more sharply as traders price in immediate risks to supply. Saudi crude adds another layer, as it is priced through official selling prices (OSPs) set relative to Oman and Dubai, influencing regional pricing rather than following a single traded benchmark.

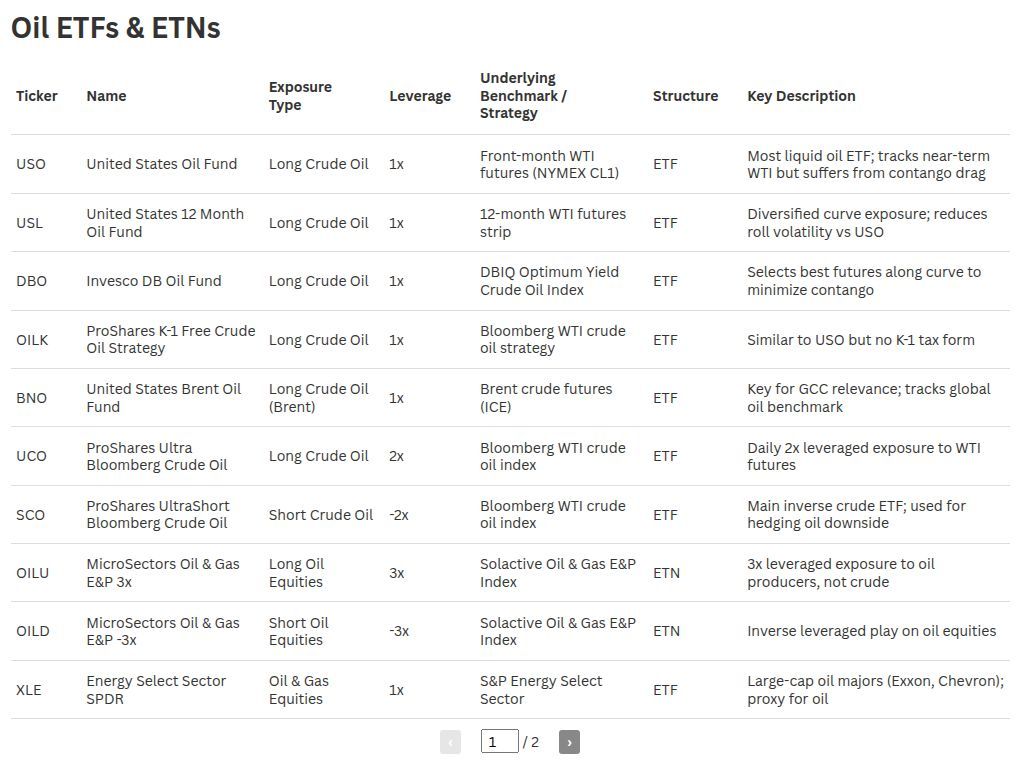

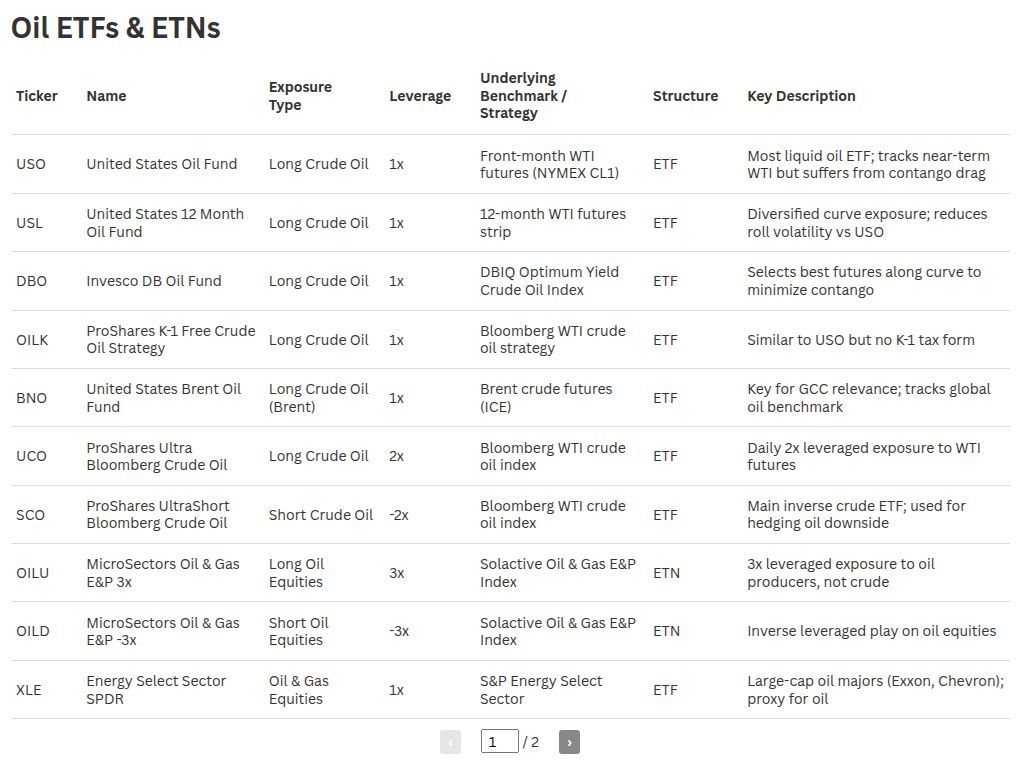

How Investors Access Oil Through ETFs

Investors typically access oil through exchange-traded products that track futures contracts rather than physical barrels. These products differ based on the benchmark they follow and how they manage futures exposure.

For U.S.-focused exposure, funds such as the United States Oil Fund (USO) track near-term WTI futures, closely reflecting short-term price movements. United States 12 Month Oil Fund (USL) spreads exposure across multiple futures contracts, helping reduce volatility linked to contract rollovers. Invesco DB Oil Fund (DBO) uses a strategy to select futures contracts based on market conditions, while ProShares K-1 Free Crude Oil ETF (OILK) offers similar exposure with a different tax structure.

For global pricing, United States Brent Oil Fund (BNO) tracks Brent crude futures, providing exposure to international oil markets rather than U.S.-specific dynamics.

More advanced products include leveraged and inverse ETFs such as ProShares Ultra Bloomberg Crude Oil (UCO) and ProShares UltraShort Bloomberg Crude Oil (SCO), which aim to deliver double or inverse daily returns. These are designed for short-term trading and can diverge significantly from oil prices over longer periods due to daily compounding.

For GCC-based investors, UCITS products such as WisdomTree WTI Crude Oil ETC and WisdomTree Brent Crude Oil ETC provide accessible exposure through European markets, often preferred for their structure and availability on international platforms.

Within the region, direct ETF exposure to oil is still limited, but investors can gain indirect exposure through energy-heavy equity ETFs such as Chimera S&P UAE UCITS ETF and Albilad MSCI Saudi Arabia ETF, where companies like Saudi Aramco play a significant role in performance.

For more direct regional pricing, Oman crude futures, linked to the Gulf Mercantile Exchange and available through platforms such as Dubai Mercantile Exchange offer one of the closest representations of GCC oil benchmarks, even though they are not structured as ETFs.

What Investors Should Always Check

Before investing in any oil ETF, it is important to look beyond the headline and understand what the product actually tracks. The first question is which benchmark it follows whether it is WTI, Brent, or another reference as this alone can lead to very different performance outcomes. Investors should also consider how the ETF manages its futures exposure, as some products focus on the nearest contract while others spread exposure across multiple months, which can affect volatility and returns over time.

Another key factor is whether the product is leveraged or inverse. These structures are designed for short-term trading and can behave very differently from the underlying oil price over longer periods. Finally, it is important to understand that most oil ETFs do not track spot prices directly. Instead, they follow futures markets, which means performance can diverge from the price investors see in headlines. As a result, two oil ETFs can behave very differently even if both are described as providing “oil exposure.”

Conclusion

There is no single oil market, only a set of interconnected benchmarks that reflect different parts of the global system. WTI captures U.S. market dynamics, Brent reflects global seaborne trade, and regional benchmarks such as Oman, Dubai, and Murban provide insight into GCC exports and flows to Asia. Saudi crude, through its official pricing system, adds another layer by influencing regional price structures rather than following a single traded benchmark.

Understanding these differences is essential. Following oil headlines without knowing which benchmark they refer to can lead to a distorted view of the market. For investors, this matters even more. Choosing the right ETF or product is not just about gaining exposure to oil, but about gaining exposure to the right part of the oil market.