Invesco QQQ built one of the most unconventional marketing playbooks in the ETF industry by treating an investment product like a cultural brand rather than a ticker symbol. Over the years, the fund sponsored everything from NCAA athletics to the New York City Food & Wine Festival, embedding itself in popular culture in a way few ETFs ever have. That era, however, is now drawing to a close.

One of the world’s largest and most heavily traded exchange-traded funds has quietly undergone a structural shift that matters more in the margins than the headlines suggest. In December 2025, the Invesco QQQ Trust (QQQ) converted from a unit investment trust (UIT) into an open-end ETF, accompanied by a modest fee cut that lowered its expense ratio to 0.18% from 0.20%. At the same time, Invesco amended a long-standing marketing provision in the fund’s prospectus, a change that is expected to unlock a significant revenue windfall for the asset manager going forward.

For a fund with roughly $400 billion in assets under management, even small adjustments carry large dollar consequences. At the new fee level, QQQ’s annual expense revenue declines by approximately $80 million, though the fund remains meaningfully more expensive than several large-cap growth competitors. Offsetting that, the revised marketing structure allows Invesco to retain far more of the economic value generated by one of the most profitable ETFs in the world.

What changed and what didn’t

The most important point for investors is what stayed the same. QQQ continues to track the Nasdaq-100 Index, uses full replication, and maintains identical holdings and weightings. There was no rebalance, no change to the index methodology, and no taxable event associated with the conversion. From a portfolio-construction perspective, the fund investors own today is structurally the same one they held before December 2025.

What did change is the fund’s legal and economic framework. By converting from a unit investment trust (UIT) to an open-end ETF, QQQ can now engage in securities lending and reinvest idle cash, practices that were restricted under its prior structure. In large, highly liquid portfolios, these tools can marginally improve tracking efficiency and total returns, though the benefit is typically measured in single-digit basis points per year rather than headline performance gains.

Less visible, but potentially more consequential, was a change embedded in the fund’s prospectus. Under its UIT structure, QQQ was required to allocate a significant portion of its estimated $150 million in annual revenue toward marketing and promotional activities.

That constraint helped turn QQQ into one of the most aggressively marketed ETFs in the industry and one of the most sought after by marketing agencies and sponsorship partners. With the conversion to an open-end ETF, that obligation has been removed, allowing Invesco to retain a much larger share of the fund’s economics and materially increase the profitability of one of its flagship products.

Ironically, the marketing strategy that grew out of that constraint helped define QQQ’s brand. Rather than leading with fees or historical performance, QQQ positioned itself as a proxy for innovation, pushing into spaces rarely associated with financial products. The ETF sponsored major sporting events, partnered with world-class chefs, experimented with gamified financial-education experiences for Gen Z, and ran city-scale outdoor campaigns more typical of consumer brands than investment vehicles. By focusing on ideas, creativity, and long-term thinking, QQQ normalized ETFs for a broader audience, built early brand affinity with future investors, and transformed a simple Nasdaq-100 tracker into one of the most recognizable and trusted investment brands in global markets.

Morningstar did not alter its overall view of the strategy following the change, maintaining a Neutral Medalist Rating, with a Below Average Process, Above Average People, and Average Parent assessment.

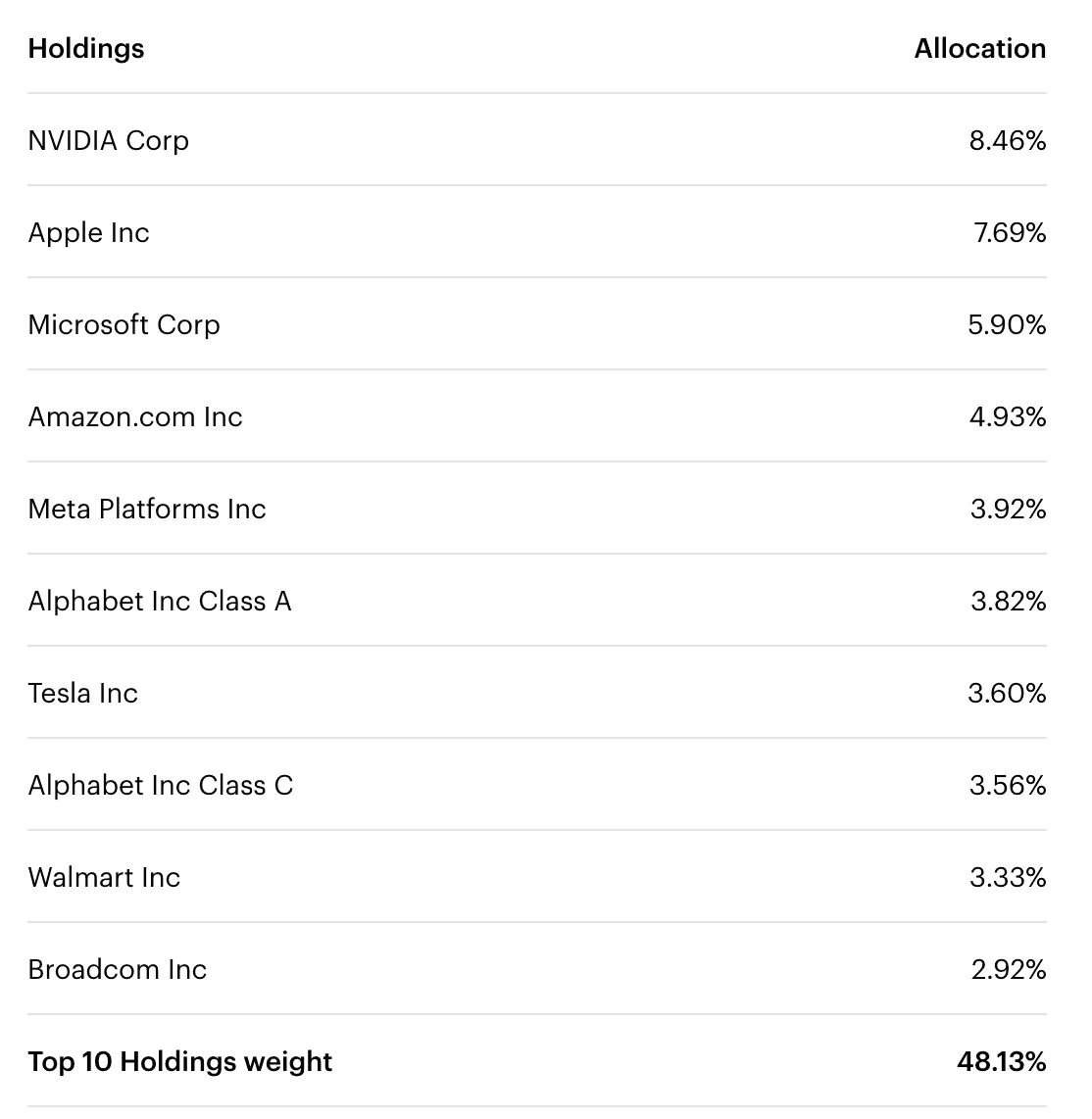

At the portfolio level, QQQ remains one of the most concentrated and liquid ways to access the Magnificent Seven Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla.

Which together continue to account for a dominant share of the fund’s weight and performance.

Top 10 holdings

source: https://www.invesco.com/qqq-etf/en/about.html

Index construction still drives the risk profile

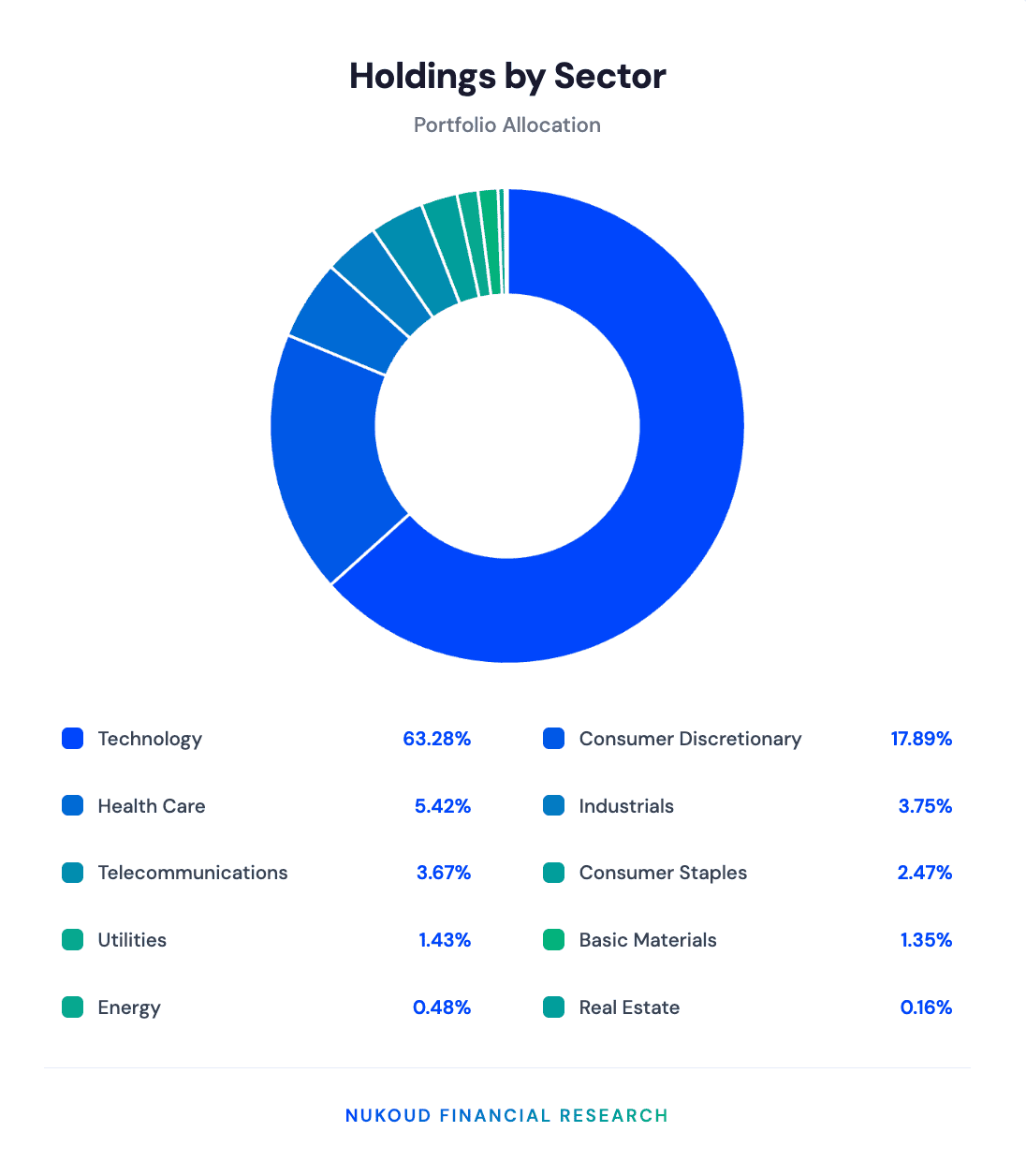

Structurally, QQQ remains bound by the Nasdaq-100’s design, which selects the 100 largest non-financial companies listed on Nasdaq, weighted by market capitalization, with concentration caps.

That design has consequences:

- Technology accounted for more than 50% of the portfolio as of December 2025

- Communication services and consumer cyclical stocks added roughly another 30%

- Stocks listed on the NYSE, such as Oracle or Salesforce, are excluded regardless of size or fundamentals

The result is a portfolio that behaves like a concentrated growth and tech proxy, even though it is not explicitly labelled as such. During drawdowns, that concentration shows up clearly. In 2022, the Nasdaq-100 fell more sharply than broader growth benchmarks, and in July 2023, the index was forced to execute a special rebalance, cutting the combined weight of its seven largest stocks to 43% from 55%.

Performance remains the anchor

Despite its structural quirks, performance explains QQQ’s enduring appeal. Since inception in 1999, the fund has delivered approximately 10.5% annualized returns through November 2025, surviving multiple boom-bust cycles, including the dot-com crash, the global financial crisis, and the 2022 rate shock.

That long-term record is the reason many investors accept higher fees and index constraints in exchange for exposure to the dominant growth franchises of each cycle.

The bottom line for ETF investors

The conversion of QQQ into an open-end ETF is a clean-up trade rather than a reinvention. The fee cut helps at the margin, securities lending may add incremental return, and Invesco gains more flexibility over one of the most profitable ETFs in the world.

For investors, the decision remains unchanged. QQQ is still a liquid, concentrated growth vehicle, not the cheapest way to access large-cap growth, but one of the most efficient ways to trade and hold the Nasdaq-100. The numbers have shifted slightly, the strategy has not.