The numbers coming out of January 2026 were hard to ignore. Global ETF inflows hit record levels, but the headline figure wasn’t the real story. What mattered was where the money went.

Capital didn’t simply expand. It rotated. Non-US equities absorbed an unprecedented share of demand. Emerging markets recorded outsized allocations. And regional dispersion in flows widened in ways that rarely happen without a reason.

Flows like these don’t lie. While prices capture outcomes, flows capture decisions, the actual allocation choices of investors managing real capital across regions, asset classes, and risk exposures. When flow patterns shift at this scale, they typically signal something more than short-term repositioning. They reflect a fundamental reassessment of where opportunity lies.

January’s data demands closer attention, particularly for markets like the GCC, that are increasingly embedded within global allocation frameworks. It is usually a month during which major strategic allocation changes occur from major institutions. Is January trying to signal the start of a major shift out of US assets as many has predicted for many years?

What Did January’s ETF Flows Actually Reveal?

Every month, analysts track where money is actually flowing, not where pundits say it should go, but where real investors are putting real money. January’s numbers were striking. A record $165 billion poured into ETFs globally. But the more interesting story was where, within that total, the money went.

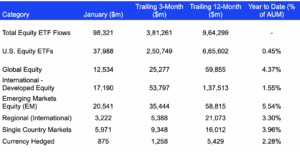

For the first time, international stocks outside the US pulled in more investor money than US stocks. Non-US equity ETFs captured $60 billion in a single month (versus $38 billion for US equities), their biggest intake on record.

This represented more than routine diversification. Investors were actively reallocating exposures, reflecting a shift in perceived opportunity sets rather than an incremental shift in risk management. Emerging markets were central to this rotation. ETFs tracking developing economies gathered approximately $20.5 billion, with the rolling three-month pace of inflows now running 238% above historical norms, a signal consistent with sustained capital reorientation rather than episodic positioning.

The underlying drivers remain familiar. Inflation pressures across several emerging economies have moderated, the US dollar has weakened, historically supportive for non-US assets, and valuation dispersion has widened as developed market multiples remain elevated relative to long-term growth expectations. In aggregate, investors appear increasingly motivated by relative value and diversification efficiency.

Equity ETF Flows Breakdown – January 2026:

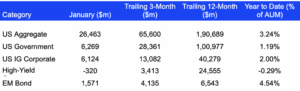

Fixed Income ETF Flows Breakdown – January 2026:

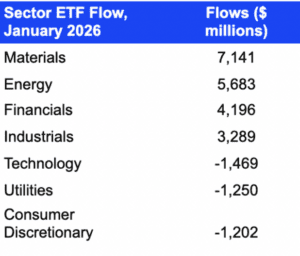

Sector Rotation Emerges as the Dominant Allocation Signal

Beyond regional shifts, sector flows reveal an equally important transition: capital rotation away from Technology and toward cyclicals or sectors that have low overlap with AI and technology such as Banking or Energy.

Cyclical sectors dominated inflows, while Technology and Utilities experienced outflows.

Several forces may be driving this rotation:

- Valuation sensitivity in growth-heavy segments

- Repricing of duration-sensitive equities

- Broadening earnings expectations

- AI exposure reduction

- Strengthening commodity-linked sectors

Why GCC Markets Are Benefiting From the Global Rotation

Global sector rotations often produce regional effects, particularly in markets whose index structures align with changing allocation preferences. The recent shift toward cyclicals carries clear implications for GCC equities.

Regional benchmarks maintain structural tilts toward energy, financials, and materials-linked industries, sectors currently attracting strong global flows. Unlike many emerging markets concentrated in technology or export manufacturing, GCC indices are naturally positioned within cyclical leadership regimes. This alignment allows the region to participate in global rotations without reliance on narrow catalysts.

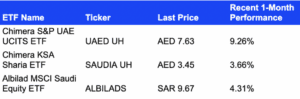

January flows suggest this dynamic is already influencing allocations. Foreign investors directed approximately $2.6 billion into GCC equity markets, a twelvefold increase from December. Saudi Arabia attracted roughly $1.5 billion, while the UAE drew approximately $846 million. Such magnitude and acceleration typically reflect deliberate portfolio rebalancing rather than opportunistic trading.

Market performance reinforced this trend. Saudi Arabia’s MSCI KSA Index advanced 10.5% during the month, broadly consistent with emerging market strength globally.

For investors seeking exposure, ETFs provide an efficient implementation mechanism, offering diversified regional access with liquidity flexibility.

The structural appeal of ETFs lies in diversification efficiency. Rather than relying on single-company outcomes, investors gain exposure to broader market dynamics, an increasingly valuable feature in flow-driven markets.

Bottom line

Markets defined by persistent rotation challenge static portfolio structures. Rather than attempting to predict short-term leadership shifts, investors often benefit from maintaining diversified exposure across regions exhibiting differentiated growth drivers.

GCC markets, supported by sovereign balance sheet strength and reform momentum, offer a distinct return profile within global allocations. ETFs provide a structurally efficient mechanism through which such exposure can be implemented while preserving liquidity flexibility.

In environments where capital flows increasingly dictate market leadership, positioning, and adaptability may prove more valuable than precision timing.