Exchange-Traded Funds (ETFs) (etfs exchange traded funds) have evolved from a niche financial product into a core component of modern investment portfolios. In developed markets such as the United States and Europe, ETFs have already reshaped how capital is allocated, how portfolios are constructed, and how investors gain exposure to entire markets with precision and efficiency.

In the Gulf Cooperation Council (GCC), this transition began later, but it is unfolding at a faster pace.

As capital markets mature across the UAE, Saudi Arabia, and Qatar, ETFs are increasingly viewed as the preferred vehicle for diversified, transparent, and cost-efficient exposure to both local and global markets. Regulators are supportive, exchanges are expanding ETF listings, and investor sophistication is rising across both retail and institutional segments.

What was once perceived as a passive, secondary tool is now being actively used for portfolio construction, tactical positioning, income generation, and risk management.

This article serves as the guide to ETF investing in the GCC. Every ETF-related explainer, market update, thematic analysis, and data-driven report links back to this page. If you are looking for a structured, practical understanding of how ETFs fit into the GCC investment landscape in 2025, this is the starting point.

1. Why ETFs Matter in the GCC Today

The GCC investment environment is undergoing a structural re-allocation cycle. Historically, portfolios across the region were heavily concentrated in a small set of asset classes including:

- Direct equity holdings (often domestic and concentrated)

- Real estate

- Private or semi-private investments

- Cash or bank deposits.

Today, most stocks, along with ETFs and mutual funds, are now accessible and tradable for GCC investors, reflecting the evolving and increasingly diverse investment landscape.

These allocations were shaped by market structure, limited product availability, and a preference for tangible or relationship-driven investments.

While these asset classes remain important, they are no longer sufficient on their own.

ETFs sit at the intersection of all these trends, which explains why their adoption has accelerated so sharply in recent years.

1.1 Cost and Transparency Advantages

One of the most immediate reasons ETFs matter in the GCC is cost. ETFs offer institutional-grade market exposure at a fraction of the cost of traditional active funds. ETFs tend to have lower fees compared to mutual funds and stocks, and are generally passively managed. Lower expense ratios mean that investors retain more of their returns over time which is an increasingly critical advantage as markets normalize after years of ultra-loose monetary conditions.

Cost efficiency alone, however, does not fully explain the appeal. The expense ratio is a key metric for evaluating ETF costs, and investors should also consider the total expense ratio when comparing different funds.

Transparency is equally important. Most ETFs disclose their holdings daily, allowing investors to see exactly what they own at any given time. This level of visibility contrasts sharply with opaque pooled investment structures that are still common in parts of the region, where underlying exposures, turnover, and risk concentrations are not always clear. Investors should also consider the ongoing costs associated with ETF investments, as these can impact overall returns.

For investors operating in a market environment that is becoming more data-driven and performance-sensitive, transparency is no longer optional, and ETFs perfectly align naturally with this shift.

1.2 Diversification in Concentrated Markets

GCC equity markets are structurally concentrated. Financial institutions often dominate index weightings, energy exposure is significant, and a small number of mega-cap stocks can drive a disproportionate share of overall market performance. While this concentration can work in favorable cycles, it also increases portfolio risk when conditions change.

ETFs provide a systematic way to diversify across sectors, countries, asset classes, and investment styles without abandoning regional exposure altogether. Instead of relying on a handful of domestic names, investors can use ETFs to broaden their opportunity set while maintaining liquidity and flexibility.

They can achieve broad exposure through a single fund, which bundles together a collection of investments, such as stocks, bonds and commodities that collectively track a specific market or index, simplifying portfolio construction.

This diversification benefit is particularly relevant in the GCC, where many investors already face implicit concentration risk. Income streams, business interests, and real estate holdings are often tied to the same regional economic drivers. ETFs allow investors to offset that exposure rather than amplify it.

1.3 Alignment with Islamic Finance

Another reason ETFs are gaining traction in the GCC is their compatibility with Islamic finance principles. Unlike many traditional investment vehicles, ETFs can be systematically structured to comply with Shariah requirements through clear, rules-based screening and ongoing oversight.

For Islamic investors, this addresses a long-standing challenge: access to scalable, transparent, and diversified investment products that remain compliant without constant manual screening. Shariah-compliant ETFs provide a repeatable framework that aligns religious principles with modern portfolio construction.

Importantly, the appeal of these structures extends beyond strictly Islamic investors. Shariah-screened ETFs often exhibit characteristics, such as lower leverage and sector discipline that can be attractive from a conventional risk-management perspective as well.

1.4 Institutional Adoption Is Driving Liquidity

Perhaps the most important shift underpinning ETF growth in the GCC is institutional adoption. ETFs are no longer viewed solely as passive buy-and-hold products. Institutional investors are increasingly using them for tactical allocation, short-term positioning, liquidity management, and portfolio rebalancing.

As institutions enter the market, liquidity improves, bid-ask spreads tighten, and price discovery becomes more efficient. This creates a positive feedback loop: better liquidity attracts more participants, which in turn benefits retail investors through lower trading friction and improved execution.

In other words, ETF growth in the GCC is not being driven from the bottom up, it is being reinforced from the top down.

2. Understanding Exchange Traded Funds: A Focused Refresher

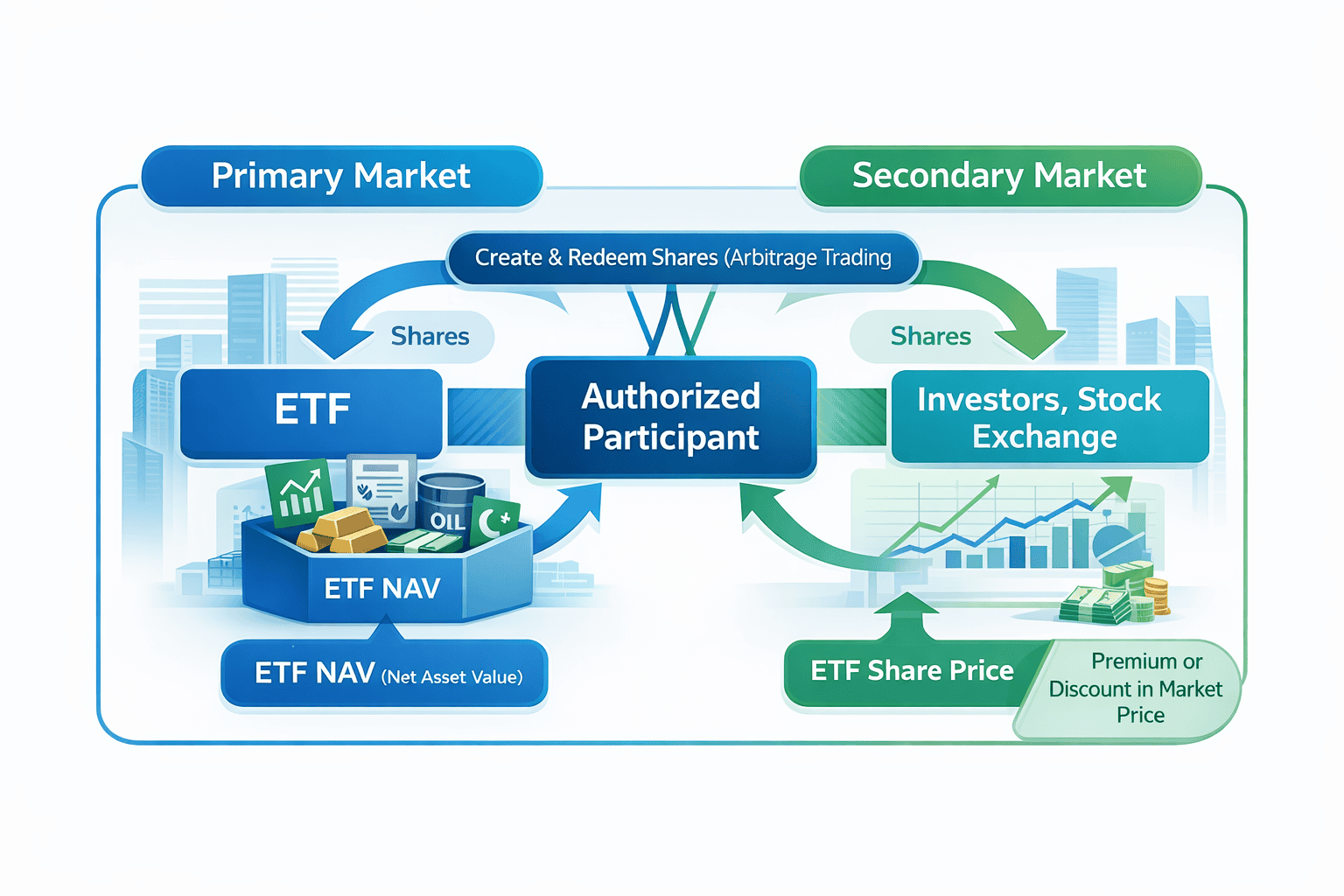

At their core, Exchange-Traded Funds are publicly traded investment vehicles designed to track an underlying index, particular index, asset class, or defined investment strategy. ETFs aim to replicate the performance of a specific benchmark, such as the S&P 500 or FTSE, by holding a portfolio of assets that mirrors the composition of that index. ETFs trade on stock exchanges throughout the day, allowing investors to buy and sell units in real time, just like shares of a company.

This structure distinguishes ETFs from traditional mutual funds, which are typically priced once per day and do not offer intraday liquidity. ETFs can be bought and sold throughout the trading day, providing investors with the flexibility to react to market changes as they happen. Trading ETFs during market hours allows investors to respond to market movements in real time, which is not possible with mutual funds.

ETFs are generally open-ended vehicles. New units can be created or redeemed through an in-kind mechanism involving authorized participants, which helps keep the ETF’s market price aligned with the value of its underlying assets. The net asset value (NAV) is an important financial metric that reflects the overall value of the fund’s holdings, calculated as the net asset of the ETF divided by the number of outstanding shares. This structural feature is central to why ETFs are able to maintain tight tracking and efficient pricing.

2.1 ETF Categories Relevant to GCC Investors

The ETF universe has expanded significantly and now spans multiple asset classes and strategies.

Equity ETFs provide exposure to local, regional, or global stock markets and are often used as core portfolio holdings. Fixed income ETFs offer access to bonds and sukuk, allowing investors to gain diversified income exposure without directly managing individual securities. Commodity ETFs which are particularly those linked to gold or energy serve as inflation hedges or tactical allocations.

A variety of fund companies, both local and international, offer these ETF products. The reputation, size, and management style of the fund companies can influence the risk and performance of an ETF, making them important factors to consider when selecting an investment.

Shariah-compliant ETFs occupy a growing segment of the market, offering Islamic equity and sukuk strategies that adhere to religious screening standards. Thematic ETFs focus on specific trends such as technology, healthcare, ESG, or energy transition, allowing investors to express targeted views within a diversified structure. Crypto-linked ETFs and exchange-traded products provide regulated exposure to digital assets, primarily for sophisticated investors seeking price exposure without direct custody.

This guide assumes a baseline familiarity with ETF mechanics. Investors seeking a deeper explanation of definitions, structures, and operational details can explore the dedicated ETF Education Center, which expands on these fundamentals in detail.

3. The ETF Market Landscape in the GCC

3.1 Local Exchanges and ETF Listings

ETF activity in the GCC is anchored by three core exchanges: the Abu Dhabi Securities Exchange, Saudi Tadawul, and the Qatar Stock Exchange. Each plays a distinct role in shaping the regional ETF ecosystem.

While these exchanges are at different stages of development, they share a common trajectory. Product breadth is expanding, market-making infrastructure is improving, and institutional participation is increasing. ETFs are no longer treated as peripheral listings but as strategic instruments within broader capital-market development plans.

Saudi Arabia currently leads the region in both the number of listed ETFs and trading volumes. ETF growth on Tadawul has been supported by rising domestic participation, increased foreign investor access, and the integration of Saudi equities into global indices. ETFs have become a central channel through which both local and international investors gain exposure to the Saudi market.

The UAE, and Abu Dhabi in particular, is positioning itself as a regional hub for innovation. The focus has been on cross-listings, partnerships with international issuers, and the introduction of differentiated products that complement global ETF offerings. This strategy aligns with Abu Dhabi’s broader ambition to serve as a bridge between regional capital and global markets.

Qatar’s ETF market is smaller in absolute terms, but it is strategically aligned with wider capital-market reforms. As liquidity deepens and institutional participation grows, ETFs are expected to play a larger role in providing diversified access to Qatari equities and income instruments.

3.2 Cross-Border Access and Global ETFs

One of the defining features of ETF investing in the GCC is the coexistence of local and international access. Most investors do not choose between domestic and global exposure; they combine both.

Local ETFs provide direct exposure to GCC markets with familiar trading hours, currency alignment, and regulatory frameworks. At the same time, most GCC brokers offer seamless access to US- and Europe-listed ETFs, allowing investors to allocate capital across global equity markets, fixed income, commodities, and thematic strategies.

This hybrid access model enables GCC investors to construct globally diversified portfolios without abandoning regional opportunities. It also allows investors to manage concentration risk more effectively, particularly in portfolios where income, business activity, or real estate exposure is already regionally concentrated.

As brokerage platforms improve and settlement infrastructure becomes more standardized, the friction between local and global ETF access continues to decline, further accelerating adoption.

3.3 Fund Providers Active in the Region

ETF issuers operating in the GCC broadly fall into three categories. Regional asset managers bring local market expertise and familiarity with regulatory nuances. Sovereign or quasi-sovereign entities play a developmental role, supporting liquidity, market depth, and product diversity. Global firms are expanding selectively, often through partnerships or targeted listings rather than blanket market entry.

Among global players, BlackRock and Vanguard have engaged with the region through strategic listings and collaborations, reflecting a broader trend of international issuers testing GCC demand with carefully structured products rather than wholesale launches.

As competition among issuers increases, investors benefit directly. Fees trend lower, tracking quality improves, and product specialization becomes more refined. Over time, this competitive dynamic strengthens the overall ETF ecosystem and reinforces ETFs as a credible alternative to traditional investment vehicles.

4. Shariah-Compliant ETFs: A Core Pillar, Not a Niche

Any serious discussion of ETF adoption in the region must treat Shariah-compliant ETFs as a core pillar rather than a niche offering.

ETFs are particularly well-suited to Islamic investing because compliance can be structured in a rules-based, auditable, and scalable manner. This contrasts with discretionary or opaque investment vehicles where compliance assessment may be inconsistent or difficult to verify.

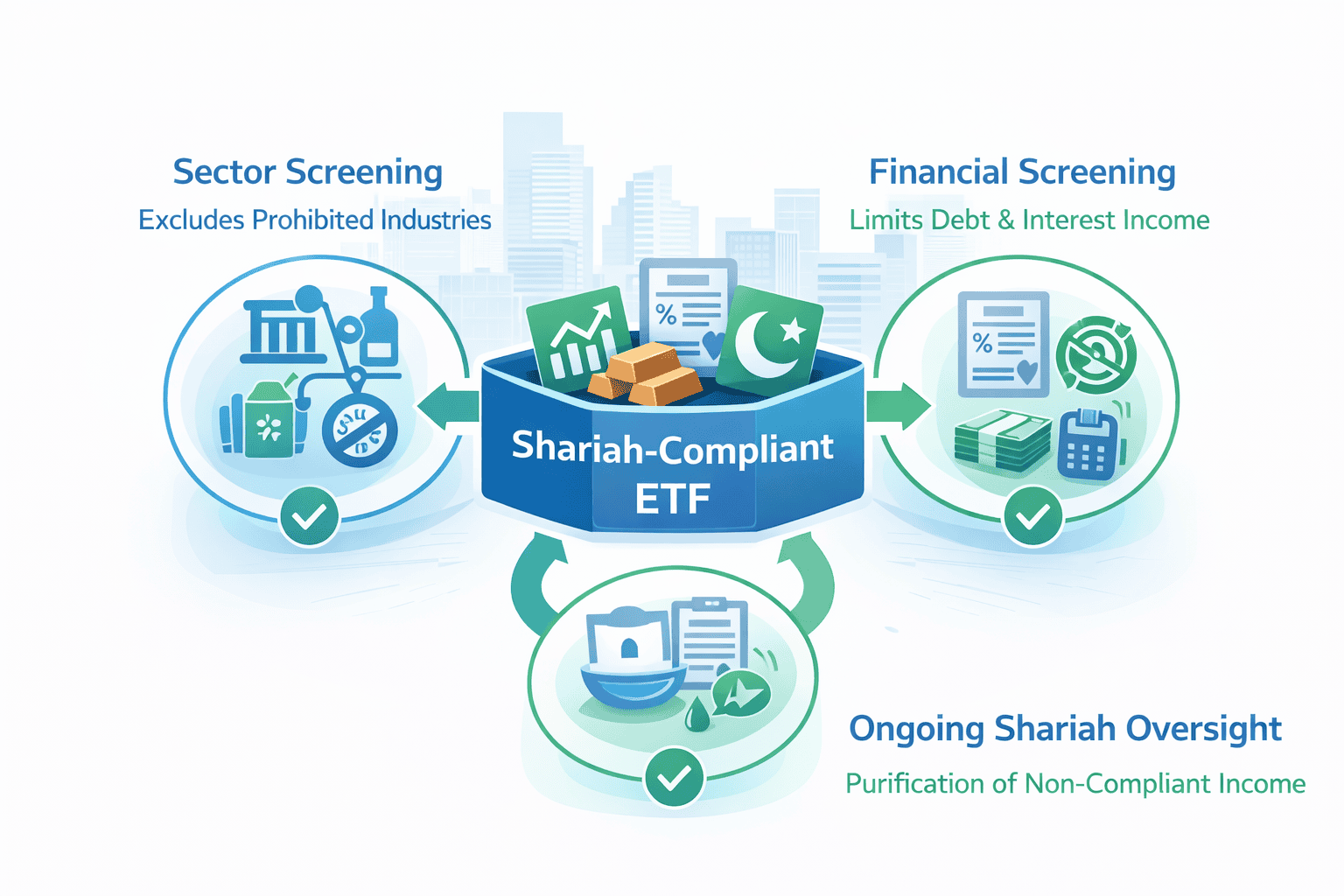

4.1 How Shariah-Compliant ETFs Work

Shariah-compliant ETFs apply a combination of sector screening, financial ratio screening, and governance oversight to ensure alignment with Islamic principles. Prohibited sectors are excluded entirely, while financial ratios limit excessive leverage or interest-based income. Any residual non-compliant income is addressed through formal purification processes.

Oversight is typically provided by independent Shariah boards, and compliance is reviewed on an ongoing basis rather than as a one-time certification. This structure provides consistency and credibility, particularly for institutional and family-office investors who require formal governance frameworks.

4.2 Types of Islamic ETFs

Islamic ETFs span multiple strategies. Shariah equity ETFs track Islamic indices composed of screened equities. Sukuk ETFs provide diversified exposure to Islamic fixed income instruments and are often used for income generation or capital preservation. Hybrid strategies combine equity and income components within Shariah constraints, offering balanced exposure for longer-term portfolios.

Rather than limiting investment choice, Shariah ETFs often introduce disciplined financial characteristics. Lower leverage, cleaner balance sheets, and sector tilts can enhance resilience during periods of market stress. As a result, Islamic ETFs increasingly attract interest from non-Islamic investors seeking structurally conservative exposure.

For detailed screening methodologies, governance frameworks, and fund comparisons, readers can explore the Halal ETF Hub, which expands on Islamic ETF structures in depth.

5. Crypto ETFs and Tokenization: Early, but Strategic

Digital assets represent one of the most closely watched frontiers in capital markets. While adoption remains measured, the strategic interest is undeniable.

5.1 Crypto ETFs in a GCC Context

Direct ownership of cryptocurrencies introduces regulatory uncertainty, custody complexity, and operational risk, particularly for institutional investors. Crypto-linked ETFs and exchange-traded products offer a regulated wrapper that aligns more closely with institutional compliance requirements and risk frameworks.

In the region, adoption has so far been selective, concentrated among family offices, hedge funds, and sophisticated retail investors. Rather than speculative mass participation, the focus has been on structured exposure, regulated venues, and institutional-grade custody solutions.

This measured approach reflects the broader GCC regulatory philosophy: innovation without sacrificing systemic stability.

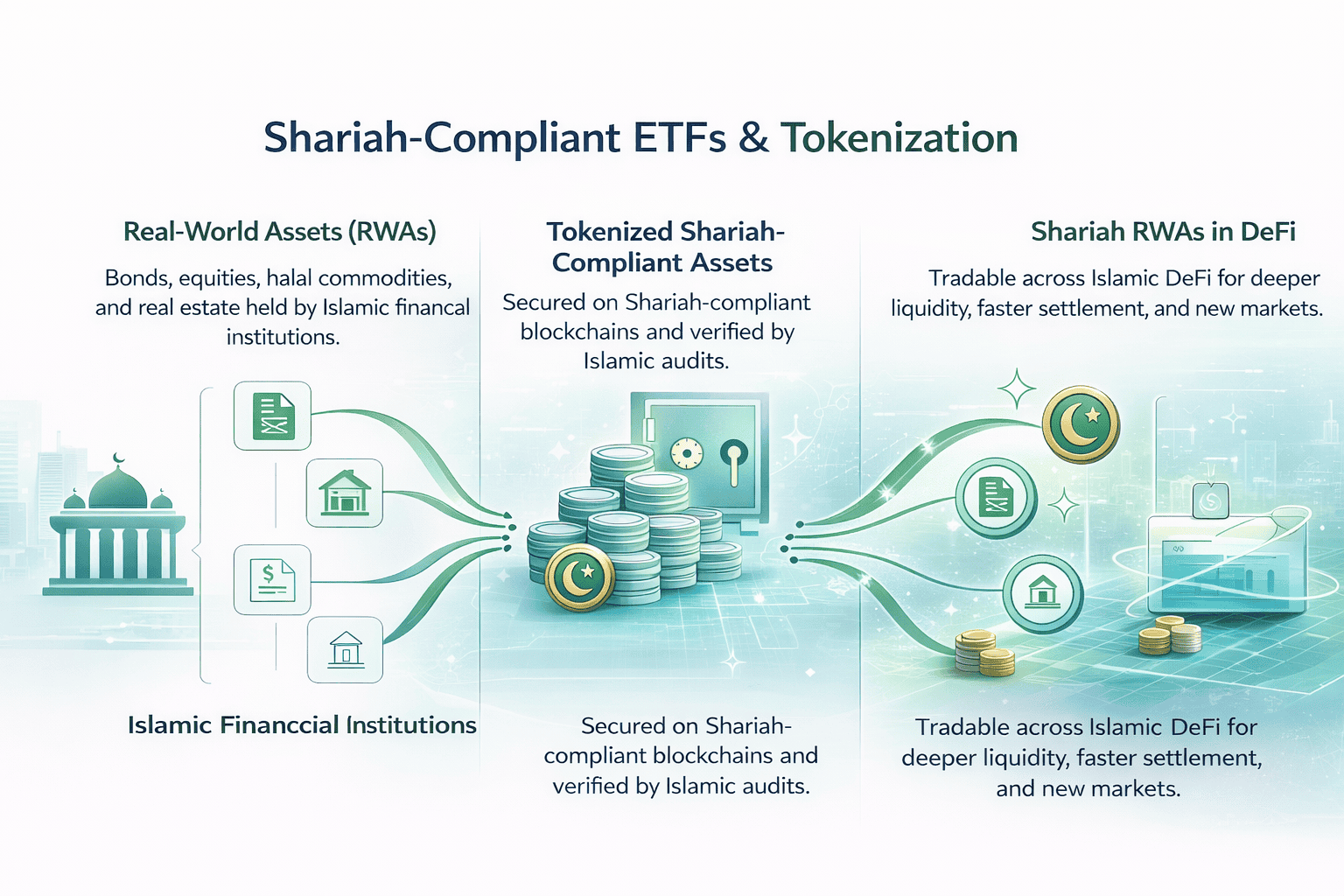

5.2 Tokenization and the Future of ETFs

Tokenization extends beyond price exposure to digital assets. It encompasses tokenized fund units, blockchain-based settlement, and fractional ownership structures that could fundamentally reshape how ETFs are issued, traded, and administered.

The GCC’s regulatory sandboxes, proactive regulators, and appetite for financial innovation make the region a natural testing ground for these models. While still in early stages, tokenization has long-term implications for market efficiency, accessibility, and settlement risk.

This theme remains emerging rather than mainstream, but its strategic importance is growing. Investors interested in the intersection of ETFs, blockchain, and digital infrastructure can explore this topic further in the Tokenization & Crypto ETFs pillar.

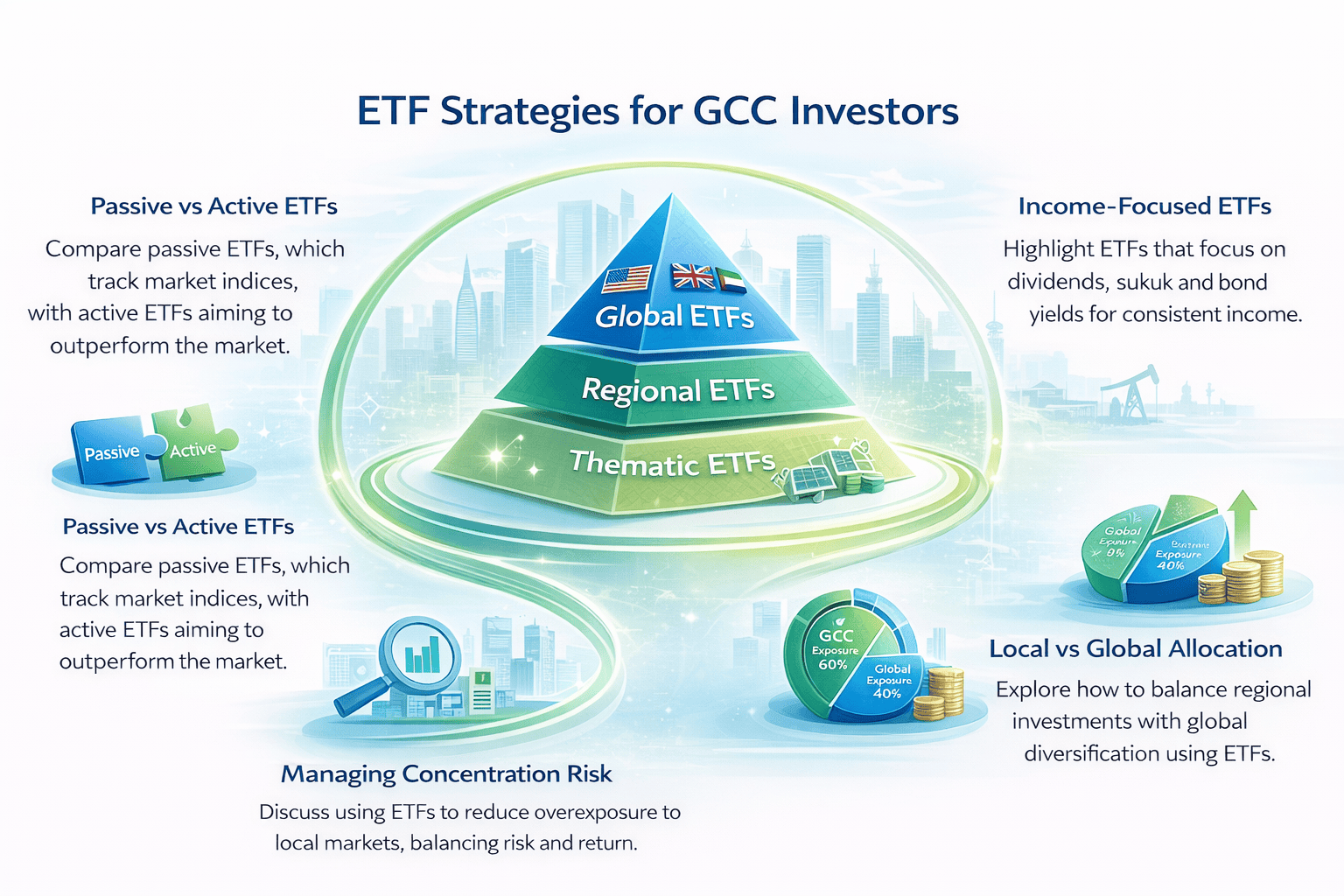

6. ETF Strategies for GCC Investors

ETF investing is not a one-size-fits-all exercise. Strategy should reflect an investor’s objectives, time horizon, risk tolerance, and existing exposure; especially in a region where many portfolios are already implicitly concentrated through business ownership, real estate, or domestic equity holdings.

ETFs are subject to market risk, meaning the value of investments can fluctuate due to changes in the overall market. Market fluctuations are a normal part of investing and should be considered when building a portfolio. As a result of market risk and these fluctuations, there is a possibility that investors may not recover the amount they originally invested. Understanding how to deploy ETFs strategically is therefore more important than simply understanding what they are.

6.1 Passive vs Active ETFs

Passive ETFs currently dominate ETF usage in the GCC, reflecting their simplicity, low cost, and predictability. These funds track well-defined indices and aim to replicate market performance rather than outperform it. For many investors, particularly those building long-term exposure to equities or fixed income, passive ETFs form the backbone of portfolio construction.

However, as markets mature and liquidity improves, active ETFs are gaining traction. Actively managed ETFs typically have higher fees compared to passive ETFs, so investors should carefully weigh the trade-offs between active management and cost efficiency. Active ETFs combine professional portfolio management with the structural advantages of ETFs, including intraday trading and transparency. Rather than tracking an index, active managers seek to generate alpha while retaining the operational efficiency of the ETF wrapper.

6.2 Income-Focused ETF Strategies

Income remains a central objective for all investors in the region. Historically, this income was generated through real estate, private lending, or dividend-paying equities held directly. ETFs now offer an alternative that preserves income generation while improving liquidity and diversification.

Dividend-focused equity ETFs allow investors to access income streams across a diversified set of companies rather than relying on a narrow group of high-yield names. When considering these ETFs, investors should pay close attention to the dividend yield, as it is a key measure of the income they can expect to receive from their investment. Sukuk and bond ETFs provide exposure to fixed income instruments that were previously difficult to access efficiently, particularly for smaller portfolios. Low-volatility or income-oriented strategies further aim to smooth returns while maintaining yield.

For many investors, these income-focused ETFs do not replace traditional income assets but complement them. They provide liquidity, reduce idiosyncratic risk, and allow for rebalancing without exiting long-term positions in real estate or private investments.

6.3 Local vs Global Allocation Frameworks

A recurring challenge for GCC investors is balancing regional familiarity with global diversification. ETFs are particularly effective in addressing this tension.

A common portfolio framework involves using global ETFs as a core allocation, providing diversified exposure across developed and emerging markets. Around this core, investors add regional or GCC-focused ETFs as satellite positions to capture local growth, policy-driven opportunities, or sector-specific themes. Thematic ETFs are then used selectively to express targeted views, such as technology adoption, energy transition, or ESG trends.

This layered structure helps manage concentration risk without eliminating regional upside. It also allows investors to adjust exposure dynamically as macroeconomic conditions, valuations, or policy environments change.

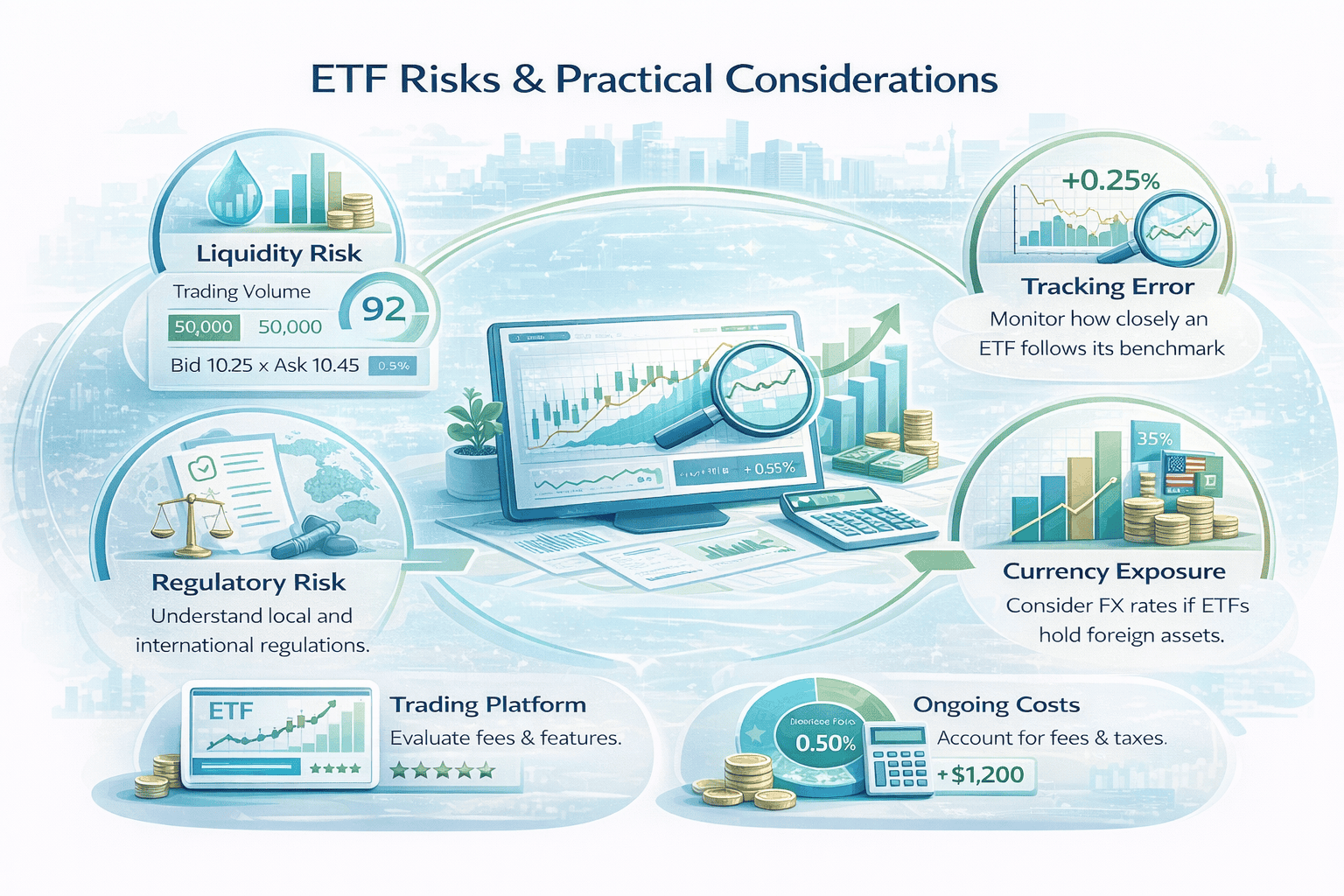

7. Risks and Practical Considerations

While ETFs are efficient and transparent, they are not risk-free. Understanding the specific risks associated with ETF investing is essential, particularly in markets where liquidity and market structure are still evolving.

Additionally, selecting a suitable trading platform for buying and selling ETFs is crucial, as platform features and fees can significantly impact your investment outcomes.

7.1 Liquidity Risk

Not all ETFs trade with the same depth. Some locally listed ETFs in the GCC may exhibit lower average daily trading volumes or wider bid-ask spreads, particularly during periods of market stress. This does not necessarily reflect the quality of the underlying assets, but it does affect execution costs.

Investors should assess liquidity holistically, considering both on-screen trading volume and the presence of market makers. For larger allocations or tactical trades, liquidity considerations can materially influence outcomes.

7.2 Tracking Error

Tracking error measures how closely an ETF follows its benchmark. Deviations can arise from management fees, sampling techniques, transaction costs, or market frictions. In more complex or less liquid markets, tracking error may be higher, particularly for niche or thematic ETFs.

For investors using ETFs as precision tools whether for hedging or asset allocation they should understand that tracking behavior is critical and persistent deviations can undermine the role an ETF is intended to play within a portfolio.

7.3 Regulatory and Structural Risk

ETF regulation varies by jurisdiction. Cross-listed or foreign ETFs may be subject to different disclosure standards, tax treatments, or trading rules than locally domiciled funds. These differences can affect after-tax returns, reporting requirements, and investor protections.

Additionally, central bank interest rate policies can influence the returns and safety of alternative investments like fixed-term deposits and government bonds, which are often compared to ETFs.

GCC investors using international ETFs should be aware of these structural distinctions and ensure that products align with their regulatory and compliance expectations.

7.4 Currency Exposure

While many GCC currencies are pegged to the US dollar, not all ETF exposures are currency-neutral. Global equity and bond ETFs introduce foreign exchange risk, which can either amplify or detract from returns depending on currency movements.

In some cases, currency exposure is a feature rather than a bug, providing diversification benefits. In others, hedging may be appropriate. Understanding how currency interacts with ETF returns is particularly important for long-term investors.

8. Performance, Flows, and Market Trends

ETF growth in the GCC is not occurring in isolation. It reflects broader structural changes across regional capital markets that are reshaping how both domestic and international capital is deployed. Increased foreign participation, inclusion of GCC equities in major global indices, privatization programs, and expanding IPO pipelines have all contributed to rising ETF usage across the region.

These developments have fundamentally changed the investor base. Global asset managers, pension funds, and sovereign allocators increasingly access GCC markets through ETFs as a first point of entry. ETFs offer a scalable, liquid, and transparent way to gain exposure while market familiarity and conviction are still developing. Over time, this ETF-led access often precedes deeper engagement through direct equity or private-market investments.

Saudi equity ETFs, in particular, have experienced sustained inflows. These flows are closely linked to the Kingdom’s economic diversification agenda, rising institutional participation, and continued improvements in market infrastructure. Enhanced settlement systems, better disclosure standards, and growing market depth have made Saudi ETFs increasingly attractive to global investors seeking emerging-market exposure with improving risk-adjusted characteristics.

Importantly, these inflows are not purely speculative or momentum-driven. They reflect a longer-term shift in how global capital accesses GCC markets, moving from episodic allocations to more permanent, benchmark-aware positioning. ETFs have become the preferred vehicle for expressing these structural allocations.

At the same time, investor interest is expanding beyond pure market beta. Thematic ETFs focused on technology, ESG, healthcare, and the energy transition are gaining traction as investors seek differentiated sources of return aligned with long-term structural trends. This shift signals increasing sophistication in ETF usage, with investors using ETFs not only for exposure, but for portfolio shaping and narrative alignment.

As data availability improves and product design becomes more refined, ETF strategies in the GCC are increasingly converging with global best practices. The region is moving from ETF adoption to ETF optimization.

For detailed performance metrics, fund flows, relative valuations, and comparative analysis across markets and strategies, readers should refer to the Market Reports & Data section, which provides ongoing coverage of these developments.

9.Taxation and ETFs

One of the structural advantages of exchange-traded funds is their tax efficiency at the fund level. Unlike many mutual funds, ETFs are generally structured to minimize internal capital gains distributions, meaning investors are less likely to face taxable events when securities are bought or sold within the fund.

For investors based in the GCC, taxation is usually not driven by local capital gains or income tax, as most GCC countries do not levy personal income or capital gains tax on individuals investing in listed securities. As a result, selling ETF shares locally typically does not trigger domestic capital gains tax for individual investors.

However, this does not mean ETF investing is entirely tax-free. The main tax consideration for GCC investors is withholding tax applied at the source, particularly on dividends. When an ETF holds foreign assets such as US or European equities dividends may be taxed before they reach the investor, depending on the domicile of the ETF and the countries where the underlying securities are listed.

In practice, the tax outcome depends more on ETF domicile and underlying markets than on the investor’s GCC residency. While most GCC investors face little to no local taxation, cross-border withholding can still affect after-tax returns, especially for income-focused ETFs.

Because tax rules vary by structure and jurisdiction, investors should consider professional advice when selecting ETFs to ensure their strategy is optimized on an after-tax basis.

10. How to Use This Guide Going Forward

This article is designed to function as a navigation hub rather than a one-off explainer. It provides the structural overview that connects all ETF-related content across the site, allowing readers to move from high-level understanding to focused, in-depth analysis.

From this central guide, readers can deepen their knowledge through dedicated content hubs covering ETF fundamentals, Islamic investing frameworks, digital asset exposure, and market-level data. Each of these pillars explores its topic in greater detail while linking back to this guide, reinforcing its role as the primary reference point for ETF investing in the GCC.

As markets evolve, new ETF products are launched, and regulatory frameworks adapt, this guide will be updated to reflect those changes. Investors should treat it as a living resource, one that evolves alongside the regional ETF ecosystem rather than remaining static.

Whether you are building your first ETF allocation or refining an existing strategy, this guide is designed to remain relevant as both markets and investor needs mature.

Final Takeaway

ETF investing in the GCC has reached a clear inflection point. What was once viewed as a peripheral or supplementary product is rapidly becoming core portfolio infrastructure.

For retail investors, ETFs offer simplicity, transparency, and efficient diversification without sacrificing liquidity.

For institutional investors, they provide scalability, precision, and a flexible tool for both strategic and tactical allocation.

For Islamic investors, ETFs deliver compliance through structured, repeatable, and auditable frameworks that align faith-based principles with modern portfolio construction.

As listings expand, liquidity deepens, and financial innovation accelerates, understanding ETFs is no longer optional for GCC investors, it is essential. Use this guide as your anchor point, and build outward from here as the regional ETF landscape continues to evolve.