Investor sentiment toward emerging markets (EM) has improved significantly, with confidence rising on expectations of stronger growth and easing inflation. Year to date, iShares MSCI Emerging Markets ETF (the MSCI Emerging Markets Index) gained around 30.5%, outperforming the S&P 500’s roughly 15.5% increase. Over the past year, the index rose about 20.5% vs. the S&P 500 delivered stronger gains of 17.7%.

As per HSBC’s 21st EM Sentiment Survey (September 2025), 62% of investors are optimistic about EM performance over the next three months, up from 44% in June 2025, marking one of the most positive readings on record. Also, bearish views declined to 7%, halving from 14% in June.

The survey gathered responses from 100 institutional investors managing a combined $423 billion in EM assets. The results indicate that resilient global economic activity, moderating inflation, and the likelihood of policy easing in advanced economies have bolstered investor conviction.

Regional and Asset Class Preferences

Within asset classes, Latin America continues to attract investors in fixed income, particularly in local currency debt, thanks to its attractive yields and scope for further monetary easing. In the equity space, Asia remains the main driver, aided by optimism around China and India.

Investors favour local currency debt (LCD), where net positioning surged to 61%, even as external debt (EXD) sentiment slipped to -11%. Within equities, Asia leads with a net sentiment of 16%, supported by positive views on China, India, and Indonesia.

However, sentiment toward Asian LCD weakened as 45% of investors expect limited room for rate cuts. Meanwhile, sentiment toward EM currencies remains positive, especially for those in the Middle East and Africa. The Chinese yuan (CNY), Brazilian real (BRL), and Mexican peso (MXN) were named among the most favoured currencies for near-term appreciation.

Renewed Optimism in Equities

Confidence in EM equities is near multi-year highs. Two-thirds of investors (66%) expect EM equities to rise in the coming quarter, and none foresee a decline. A majority (61%) also believe EM stocks will outperform developed markets.

Building on this renewed optimism in EM equities, GCC equity ETFs have also attracted increasing investor interest, supported by resilient corporate earnings, elevated oil prices, and ongoing economic reforms across the region.

Funds tracking Saudi Arabia, the UAE, and Qatar have seen steady inflows as investors seek diversified exposure to sectors benefiting from fiscal expansion, infrastructure investment, and Vision 2030-driven growth initiatives.

The strength of regional indices, particularly Saudi Arabia’s Tadawul and the ADX in Abu Dhabi, has reinforced confidence in GCC equities as part of the broader EM recovery story, positioning these markets as attractive destinations for both yield and growth-focused investors.

As of September 23, there are 26 equity equities listed across UAE (14), Saudi Arabia (9), Qatar (2) and Egypt (1). With regard to AUM, Albilad CSOP MSCI Hong Kong China Equity ETF is the leading equity ETF and has delivered a year-to-date return of 39.15%. This is followed by SAB INVEST HANG SENG HONG KONG ETF which witnessed a year-to-date growth of 36.99%. Also, Chimera S&P China HK Shariah ETF witnessed an increase of 41.4% and Chimera S&P India Shariah ETF fell 4.6% year-to-date.

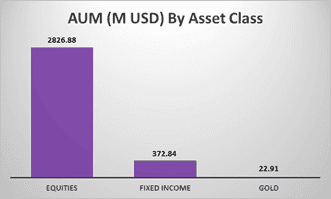

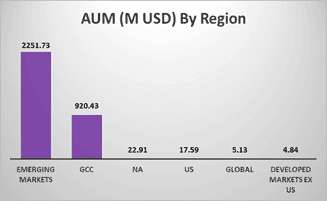

The breakdown of GCC ETFs’ assets under management (AUM) by asset class and region is as follows:

Market Still Cautious

Despite rising optimism, investor risk appetite showed only a modest uptick to 6.2 from 6.1 in June, indicating lingering caution amid trade uncertainties and recession fears in advanced economies. Cash holdings dipped to 5.5% of assets, yet 44% of investors maintain over 5% in cash, reflecting continued caution.

Trade tensions and global recession fears continue to weigh on sentiment, though both concerns have eased. About 28% of investors see tariffs and trade disputes as the main downside risk (down from 32%), while 22% cite recession worries in major economies (down from 27%). A growing 9% are wary of a stronger U.S. dollar’s potential drag on EM assets.

However, the recent weakening of the U.S. dollar has provided a notable boost to EM currencies, easing financial conditions and improving capital inflows. A softer dollar makes EM assets more attractive by lowering debt-servicing costs and supporting local purchasing power.

As U.S. rate cuts and moderating inflation take hold, this trend could serve as a structural tailwind for EM currencies, enhancing returns and fuelling growth across equity and fixed-income markets for years to come.

Summary

The final quarter of 2025 finds EMs on firmer footing. Investors are leaning into opportunities in equities and local debt while keeping an eye on trade and policy developments. With expectations of stronger growth and moderating inflation, EMs are once again emerging as a preferred destination for global capital seeking both yield and diversification.

The expectations for economic acceleration have strengthened, with 36% of respondents anticipating faster EM growth over the next 12 months, up from 33%. The share expecting a slowdown declined to 23% from 39%.

Inflation expectations have improved as well, with 39% forecasting lower inflation versus 26% who expect it to rise, reflecting growing confidence in disinflation trends across Asia and Latin America.