Saudi Exchange (Tadawul) has published a new ETF Market Making Framework designed to strengthen the secondary-market trading experience for exchange-traded funds, specifically by tightening bid-ask spreads, improving liquidity, and supporting more efficient price formation.

For ETF investors, this is not cosmetic. When spreads are wide or quotes disappear, ETF ownership becomes more expensive in practice, even if the fund’s ongoing fees look low on paper. Tadawul’s framework directly targets that friction by defining clear quoting obligations for market makers and pairing them with fee incentives for compliance.

What Tadawul is introducing

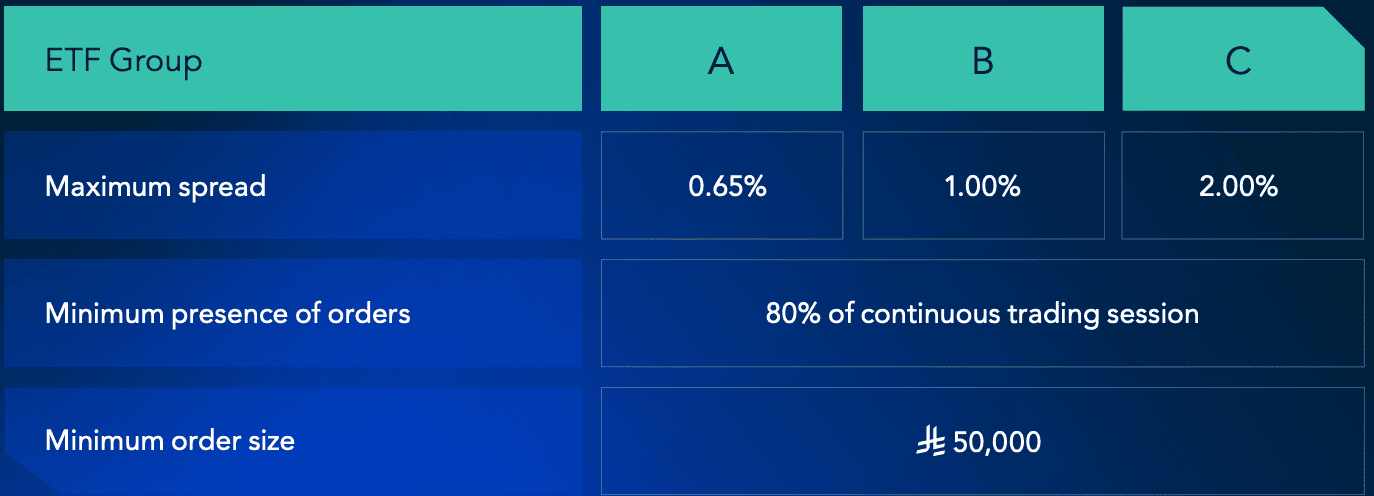

At the center of the framework is a set of predefined market-maker obligations grouped into three tiers (A, B, C). The ETF’s tier is chosen by mutual agreement between the fund manager and the market maker, and can be changed later if both request it, subject to Tadawul approval.

The obligations focus on three levers that matter most to day-to-day ETF tradability:

- Maximum bid-ask spread (how wide the quote can be)

- Minimum presence time (how often quotes must be present during the continuous session)

- Minimum order size (minimum quoted size)

The three obligation tiers (A / B / C)

From the factsheet, the tiers include the following parameters:

The incentive: 100% trading-fee rebate (if obligations are met)

To make these obligations commercially viable for liquidity providers, Tadawul offers daily 100% fee incentives—covering commissions charged by Saudi Exchange, Edaa, Muqassa, and the CMA provided the market maker adheres to the obligations in the Market Making Agreement.

That’s an unusually explicit incentive package, and it reinforces the framework’s purpose: building an ETF market that behaves more like mature global venues where market making is structured, measurable, and rewarded.

Who can be an ETF market maker, and which ETFs qualify?

Tadawul’s factsheet lays out clear eligibility:

Applicants must be either:

-

- an Exchange member of Saudi Exchange, or

- a client of an Exchange member.

Exchange members can act as a market maker as principal or as agent on behalf of their clients, and Tadawul retains the right to accept or reject applications and determine whether the activity is conducted as principal or agent.

On scope, the framework is broad:

All listed ETFs on the Saudi Exchange are eligible for market making.

This is important because it clarifies accountability: the exchange is not simply encouraging liquidity. It is creating a monitored, contractual set of behaviors tied to incentives.

Why Tadawul is doing this

The Saudi Exchange frames the initiative as part of developing a more dynamic and accessible ETF ecosystem, contributing to the advancement of the Saudi capital market under the Financial Sector Development Program and Vision 2030.

In practical market terms, the framework is aimed at the three pain points that limit ETF adoption in newer ETF ecosystems:

- Wide spreads that increase trading costs

- Patchy quote presence that makes execution uncertain

- Weaker price formation that undermines confidence in the ETF’s fair value

How does this benefit issuers and investors

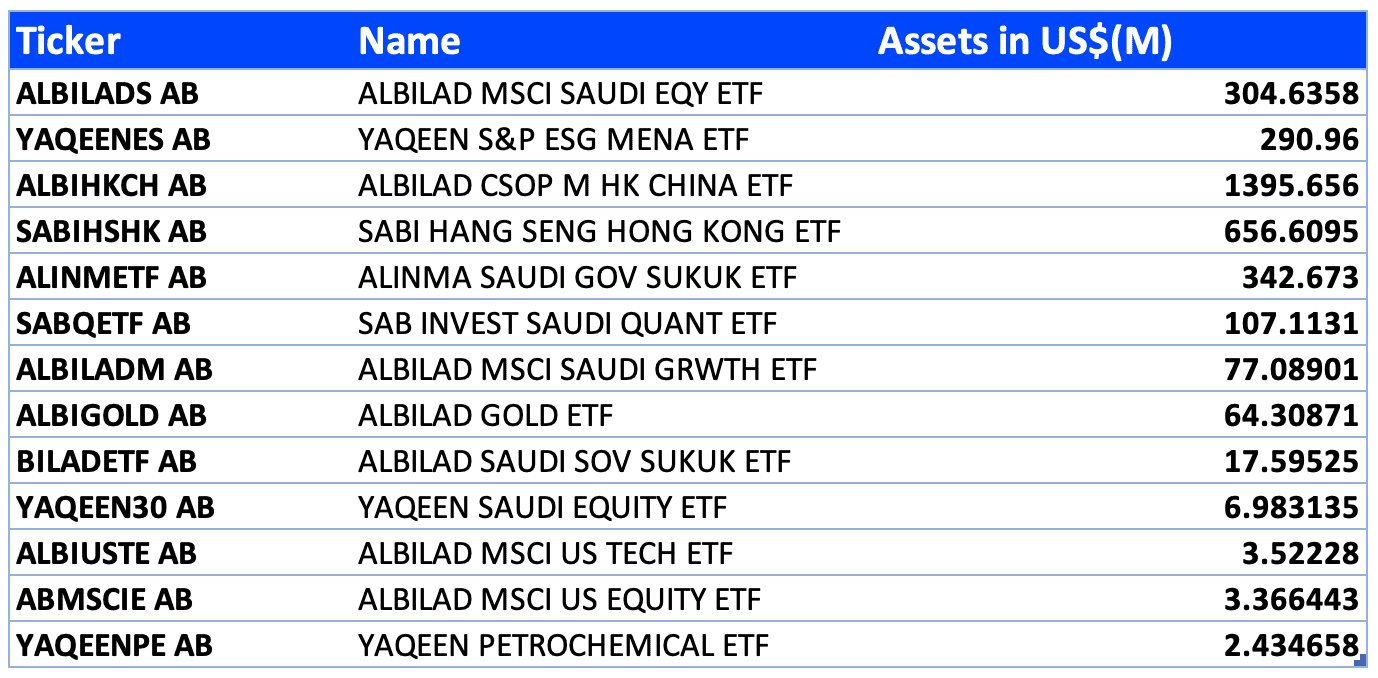

For GCC investors, particularly those weighing Saudi-listed ETFs against cross-listed or offshore alternatives, Tadawul’s new market-making framework matters because liquidity and bid-ask spreads are often the difference between an ETF merely existing and being genuinely investable at scale. Today, the Saudi ETF market comprises 13 listed ETFs with a combined assets under management base that is still relatively modest, making secondary-market quality especially important as the segment grows.

At the same time, the framework gives issuers a practical tool to shape trading quality from day one, with tier selection agreed jointly between fund managers and market makers and embedded directly into ETF go-to-market planning. By allowing these obligations to be adjusted over time with Tadawul’s approval, the exchange creates a clear pathway for ETFs to graduate their liquidity commitments as trading activity deepens.

Taken together, the framework represents a meaningful upgrade to the mechanics that make ETFs work in practice one that may not grab headlines, but can materially lower execution costs, improve price discovery, and strengthen investor confidence in Saudi-listed ETFs over time. To learn more about the broader evolution of ETFs across the region, see our guide to GCC ETFs in 2025.