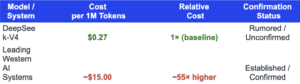

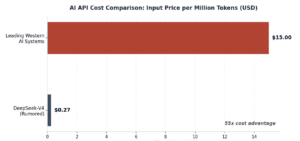

The global artificial intelligence race is approaching a new inflection point, and this time, the disruption is not primarily about model capability. It is about economics. Markets and the technology community are closely watching the anticipated release of DeepSeek-V4, the next-generation model from Hangzhou-based AI startup DeepSeek. While official specifications remain limited, early industry leaks point to a potentially transformative pricing structure: API input costs rumored at just $0.27 per million tokens, compared with approximately $15 per million tokens for leading Western AI systems. If confirmed, that represents a cost differential of more than 55 times.

For GCC investors with exposure to China technology ETFs, this development carries meaningful sentiment and thematic implications most directly for funds such as the KraneShares CSI China Internet ETF (KWEB), which sits at the intersection of China platform leadership, AI narrative momentum, and cross-border capital flows.

The Cost Disruption: Why $0.27 Per Million Tokens Matters

To appreciate the significance of DeepSeek-V4’s rumored pricing, consider where AI inference costs currently stand:

Across technology cycles, it has consistently been cost compression, not incremental performance improvements, that catalyzes structural shifts in adoption. When inference prices fall dramatically, four consequential dynamics tend to emerge simultaneously:

- New user segments emerge, including price-sensitive developers, startups, and SMEs previously priced out of AI-native workflows.

- Experimentation accelerates as the cost of failure falls, compressing innovation timelines across industries.

- Adoption barriers weaken across geographies and use cases, including in GCC markets where digital transformation agendas are accelerating.

- Integration becomes economically viable at scale, unlocking enterprise deployment that was previously marginal on a unit-economics basis.

DeepSeek-V4, if its cost structure is validated, represents less of a model release than a pricing shock to AI infrastructure economics, one with implications well beyond China’s domestic technology sector.

Why This Matters for GCC Investors?

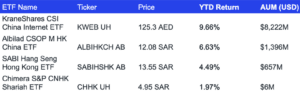

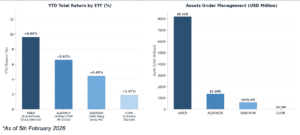

GCC investors seeking exposure to China’s digital economy have access to several ETF vehicles, each with distinct characteristics in terms of technology concentration, AI sensitivity, and assets under management. The tables and charts below provide a structured comparison.

KWEB’s defining characteristic is exposure to China technology stocks. With $8.2 billion in assets and a near 9.66% YTD gain, it is both the largest and best-performing vehicle in this dataset. Its concentrated positioning in Chinese internet and platform leaders, the firms most sensitive to AI optimism cycles, makes it the most direct proxy for DeepSeek-V4 narrative momentum among GCC-accessible instruments. Hang Seng tracking funds offer broader Hong Kong equity exposure, diluting technology concentration but providing more stable, diversified return profiles. Shariah-screened vehicles offer the highest level of diversification but the least direct participation in AI-driven sentiment cycles.

ETF Performance and Scale Comparison

*As of 5th February 2026

What Happened Last Year: DeepSeek-Driven ETF Flows

Last year’s launch of DeepSeek’s early AI models, particularly the DeepSeek chatbot based on the R1 architecture, disrupted markets when it became the most-downloaded AI app in January 2025

During that period, ETF flows into China-related technology funds spiked. For example, the KraneShares CSI China Internet ETF (KWEB) recorded approximately $105 million of inflows in late January 2025, marking its strongest weekly inflow in nearly four months amid renewed enthusiasm for Chinese AI and internet stocks. Reports also highlighted sustained capital allocation to China tech ETFs, with KWEB recording inflows exceeding $637 million in a subsequent week linked to DeepSeek-driven optimism, signalling a notable shift in global investor sentiment.

This rebound aligned with a broader recovery in foreign investment, as offshore inflows into Chinese equities surpassed $50 billion in 2025 through October, a multiyear high partly supported by AI-related narratives. The episode demonstrated how powerful technology themes, even before full monetization, can drive significant capital flows into China’s technology assets and influence ETF positioning among global and GCC investors.

Could the Timing of the Chinese New Year Amplify Market Impact?

Speculation that DeepSeek-V4’s release may coincide with the Chinese New Year period adds a strategically significant dimension to the narrative. In recent years, the Chinese New Year has increasingly served as a platform for major technology announcements and forward-looking signals, a moment that blends cultural weight with deliberate strategic positioning.

Launching a frontier domestic AI model during this period reinforces narratives of technological renewal, national innovation momentum, and competitive advancement against Western incumbents. For sentiment-driven sectors such as technology, symbolic timing frequently amplifies market reactions beyond what underlying fundamentals alone would justify. Investors should be alert to the possibility of announcement-driven volatility in the near term.

Bottom line

DeepSeek-V4 represents more than another iteration in the AI model arms race. It symbolises a potential structural shift in AI economics, one that, if validated, could ripple through adoption curves, infrastructure pricing, competitive dynamics, and technology equity sentiment globally.

For GCC investors, the relevance is direct and proximate. Vehicles such as KWEB sit precisely at the intersection of China technology exposure, AI innovation narratives, and sentiment-driven capital flows. The fund’s scale, concentration, and demonstrated responsiveness to China technology developments make it the clearest available lens through which to evaluate this theme.

Whether DeepSeek-V4 ultimately delivers on its rumoured cost advantage and whether that advantage proves durable at scale remains to be determined. But in markets where narratives routinely travel faster than data, the story itself may generate meaningful near-term positioning activity regardless of the eventual empirical outcome.