Three weeks ago, software stocks were repricing.

The catalyst was Anthropic’s expansion of Claude’s agentic capabilities, particularly Claude Code Security and Claude Cowork. What could have been viewed as incremental product development instead triggered a broader structural concern: that autonomous AI agents may directly compete with parts of the SaaS and cybersecurity ecosystem.

While stock price correction was swift and broad, these sectors have recently attracted significant flows. The real question is the market pointing to an overreaction and buying the dip type of situation?

From Productivity Tool to Competitive Threat

Software companies have integrated AI for years. The market reaction this time was different.

Claude demonstrated increasingly autonomous workflows with AI capable of scanning codebases, identifying vulnerabilities, suggesting fixes, and potentially replacing segments of human-led security, compliance, and coding services.

That shift reframed AI from productivity enhancer to workflow competitor. If AI agents can perform security audits, compliance reviews, and legal analysis at scale, what happens to subscription-based SaaS models built around human workflows? Markets moved quickly to price that risk.

The repricing extended beyond high-growth SaaS names. It touched cybersecurity, legal analytics, compliance platforms, and data infrastructure firms globally.

This was not earnings-driven volatility. It was a structural concern.

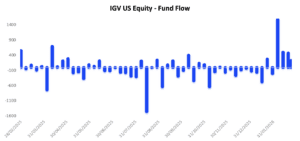

IGV, the iShares Expanded Tech-Software ETF, became the central pricing vehicle. It fell more than 20% from its 2025 highs and dropped sharply during the Claude-driven panic phase.

Global X Cybersecurity UCITS and First Trust NASDAQ Cybersecurity ETF reflected the cybersecurity repricing, while WCLD amplified the high-beta SaaS reaction.

But then something unexpected happened.

Despite the price decline, IGV (iShares Expanded Tech-Software ETF) attracted roughly $2.5 billion in inflows, which is well above average.

Price Panic, Capital Conviction

Prices reflected fear; flows reflected selective conviction. Investors appear to be distinguishing between immediate competitive headlines and genuine long-term business model erosion.

Many allocators seem to view the repricing as a multiple reset rather than a collapse in underlying revenue durability especially given that valuations entering 2026 were already elevated and vulnerable to compression. The “Claude shock” may therefore have accelerated a correction that was structurally primed to occur.

Some analysts argue the selloff was excessive, noting that enterprise software firms still command deep data ecosystems, entrenched distribution networks, regulatory and compliance frameworks, and mission-critical integrations that cannot be displaced overnight.

Others counter that AI agents could gradually erode per-seat subscription pricing and redirect economic value toward AI infrastructure providers. The reality likely sits between these extremes: not existential disruption, but margin and pricing pressure that forces a recalibration of expectations rather than a wholesale abandonment of the sector.

The Bigger Picture

The “Claude Shock” marked the first large-scale equity market stress test of autonomous AI agents as competitive economic actors. Software stocks sold off sharply, cybersecurity names repriced, and legal and compliance platforms experienced historic declines.

Yet capital did not leave the space, it rotated. ETFs such as IGV, BUG, and WCLD became transmission channels for both panic and tactical re-entry, highlighting how passive vehicles now amplify volatility while simultaneously facilitating repositioning. The episode underscores a broader shift: AI is no longer priced as a one-way growth narrative.

Markets are beginning to differentiate between AI as a productivity catalyst and AI as a redistributor of industry economics. Software and cybersecurity are not being abandoned; they are being stress-tested. The selloff appears less a collapse in demand than a reassessment of durability, pricing power, and competitive moats in an agent-driven landscape, a view reinforced by record inflows into IGV, suggesting capital is recalibrating exposure rather than exiting the theme altogether.