China internet stocks have been on a hot streak so far this year and through much of 2025. The key drivers have been easing political tensions with the US, the emergence of China’s AI potential beginning to show up in earnings, and a gradually recovering domestic economy. That last pillar has been slow-moving, but it was increasingly seen as the final piece needed for China internet stocks to begin closing the wide valuation gap with US technology and AI peers.

On valuation alone, Chinese AI leaders such as Alibaba, Tencent, and Baidu remain among the cheapest globally when screened against international AI and platform companies. The lingering impact of COVID, regulatory tightening, and years of US–China tensions still leaves a bad taste for global investors, despite improving fundamentals.

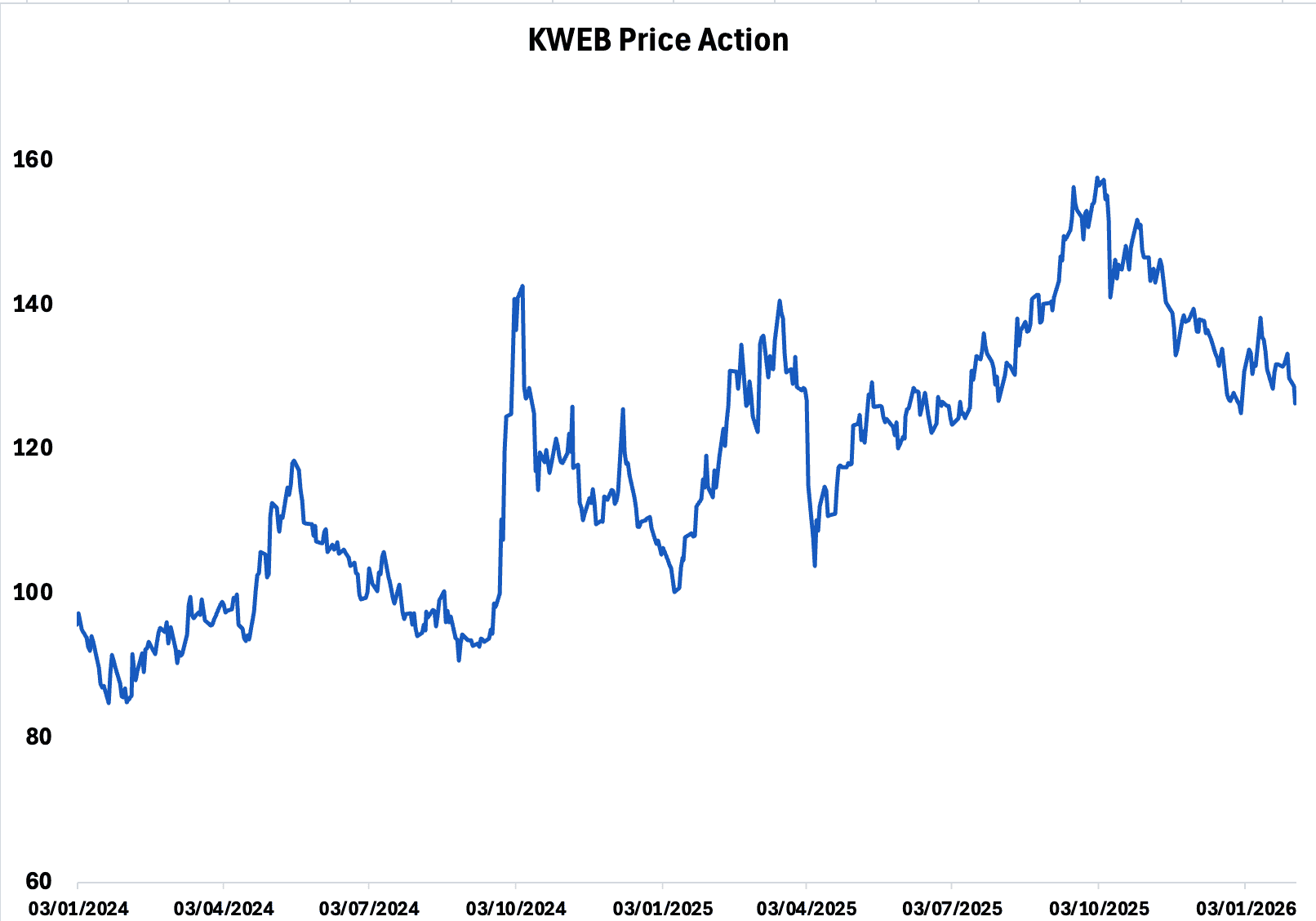

This week, however, a new concern emerged. China announced a value-added tax (VAT) increase on telecom companies, raising the rate from 6% to 9%, which some investors feared could eventually extend to internet and gaming companies. The reaction was swift: Tencent shares closed more than 3% lower, while the KraneShares China Internet ETF (KWEB) slid toward $34, or approximately AED 122, based on prices quoted by ADX market maker Oceane Invest.

Sell-side analysts were quick to downplay the broader implications. J.P. Morgan said the move reflected a clarification in VAT classification specific to telecom services, rather than a framework that would be applied across the digital economy. The bank noted that most China internet business models are unlikely to be affected.

As the analysts explained:

“Applying the telecom logic literally, ‘connectivity-like services were clarified as basic telecom (9%).’ The read-through to most China internet business models is limited. Advertising, platform commissions, online content and services, software and IT services, and most digital services do not become ‘basic telecom’ simply because they operate over the internet. These activities remain classified as modern or IT services, where the prevailing VAT rate is 6%.”

More broadly, China appears to have learned from the regulatory tightening of 2021, which weighed heavily on major internet platforms and employment. Market participants increasingly believe that policymakers are more likely to support growth and innovation — particularly in AI — than to impose new burdens on the sector.

In conclusion, most previous pullbacks in China internet stocks and KWEB have ultimately proven to be buying opportunities rather than structural breaks in the story. This episode may be no different, particularly for investors looking to gain exposure at discounted valuations.

For GCC investors, access to China internet and technology exposure now extends beyond KWEB. Regional options include the Lunate China ETF and the Saudi-listed Albilad CSOP China ETF, offering additional regulated routes to participate in China’s internet and AI recovery.