Covered call strategies have long been used by institutional investors to generate income from equity positions, particularly when price appreciation is uncertain or markets move sideways. Historically, implementing these strategies required active options trading and specialized derivatives expertise. The growth of ETFs transformed this landscape by embedding covered call mechanics into transparent, rules-based structures accessible to a much broader range of investors.

Over the past decade, persistent market volatility, low interest rates, and elevated valuations have strengthened the search for reliable income. For GCC investors traditionally reliant on dividends, fixed income, and real assets, the emphasis on stable cash flows has become increasingly central to portfolio construction.

Covered call ETFs operate at this intersection of income demand and structural innovation. By monetizing volatility and option premiums rather than relying solely on dividends or coupons, they offer an alternative source of yield even when equity markets remain range-bound.

What Is a Covered Call?

A covered call is an options strategy in which an investor owns a stock (or equity index exposure) and simultaneously sells a call option on that position. Selling the option generates an upfront premium, providing income, while granting the buyer the right to purchase the shares at a fixed strike price before expiration.

This strategy is typically used when modest price movement is expected. It seeks to enhance income through premiums and offers limited downside cushioning, but the trade-off is capped upside if the asset rises above the strike price.

In ETFs, covered calls are implemented systematically across diversified portfolios, enabling consistent premium capture and regular income distributions.

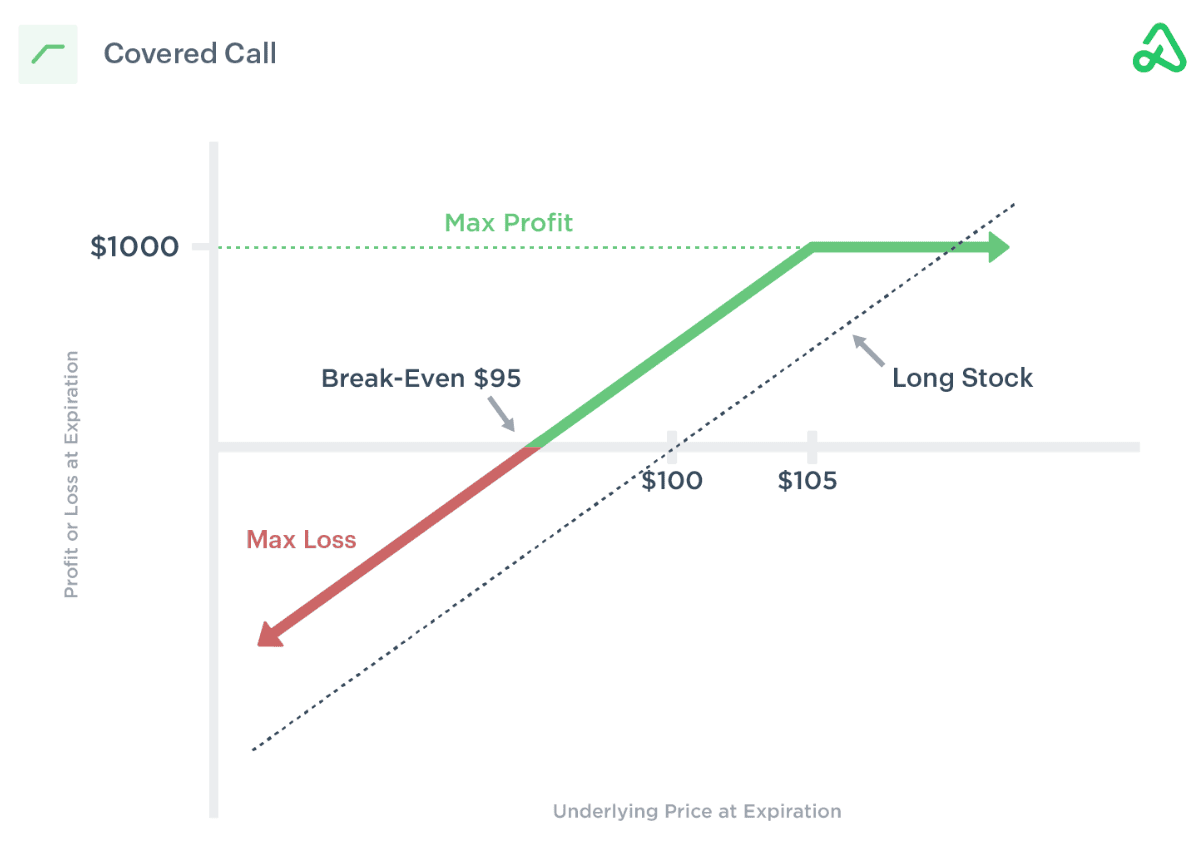

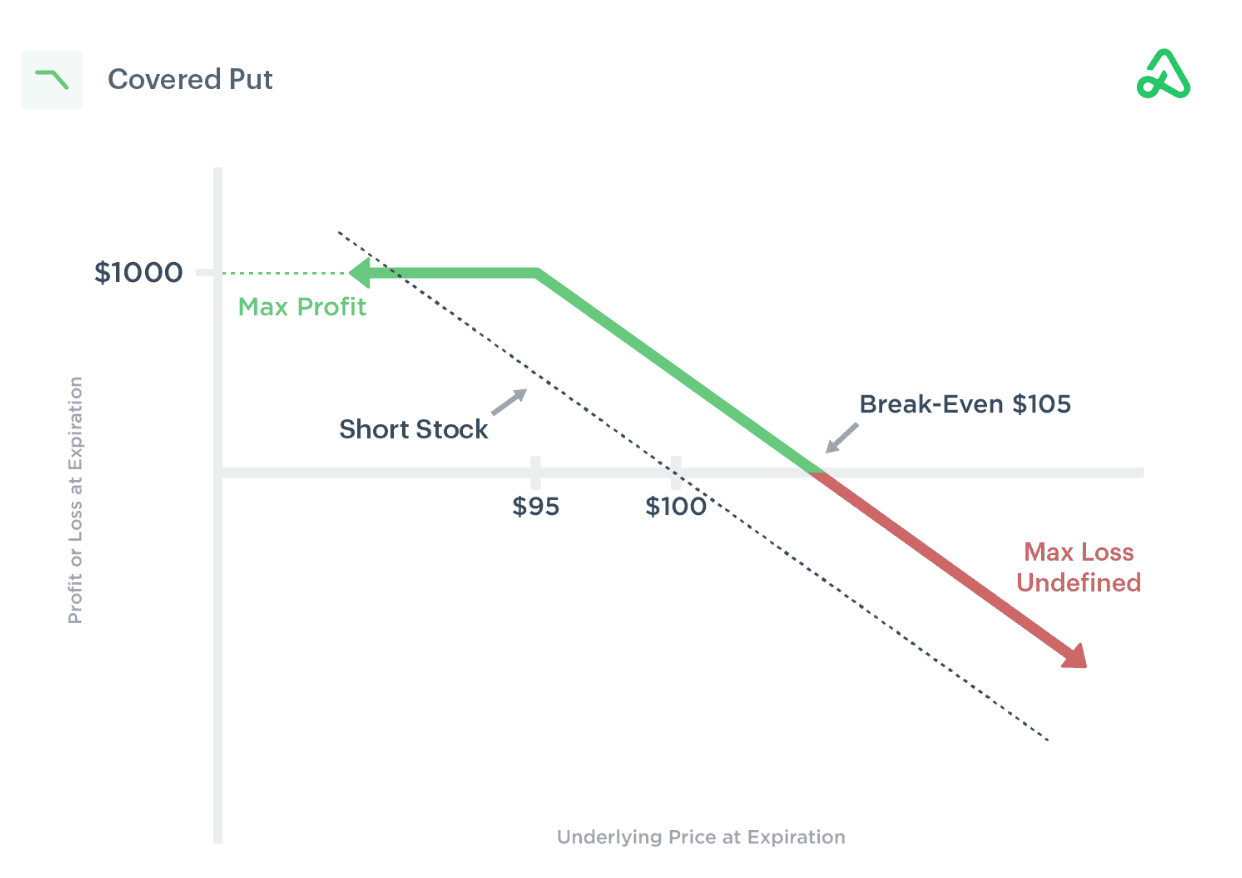

Covered Call vs Covered Put, Payoff Illustrated

A payoff chart makes it easier to understand how covered option strategies behave as stock prices change at expiration. In the covered call example shown above, the investor owns the stock at $100 and sells a call option with a $105 strike price. The chart highlights a breakeven level near $95, which reflects the premium received from selling the option. If the stock remains below $105, the option expires worthless, and the investor keeps the premium as income. If the stock rises above $105, gains are capped because the shares may be sold at the strike price, limiting further upside. If the stock declines, losses occur, although the premium collected slightly cushions the downside. In simple terms, the covered call generates income but limits profits in a strong rally.

The covered put chart represents the opposite positioning. Here, the investor is effectively shorting the stock around $100 and sells a put option with a $95 strike price, producing a breakeven level near $105. If the stock stays above $95, the put expires worthless, and the premium becomes profit. If the stock falls below the strike price, the investor may need to buy the shares at $95, with profits depending on how much the stock declines. However, if the stock price rises significantly above $105, losses increase because the short stock position moves against the investor. In essence, the covered put also generates premium income, but rising prices create substantial risk.

Together, these examples demonstrate the symmetry between the two strategies. Both seek income through option premiums, yet a covered call sacrifices upside beyond the strike price, while a covered put exposes the investor to potentially large losses if prices rise sharply.

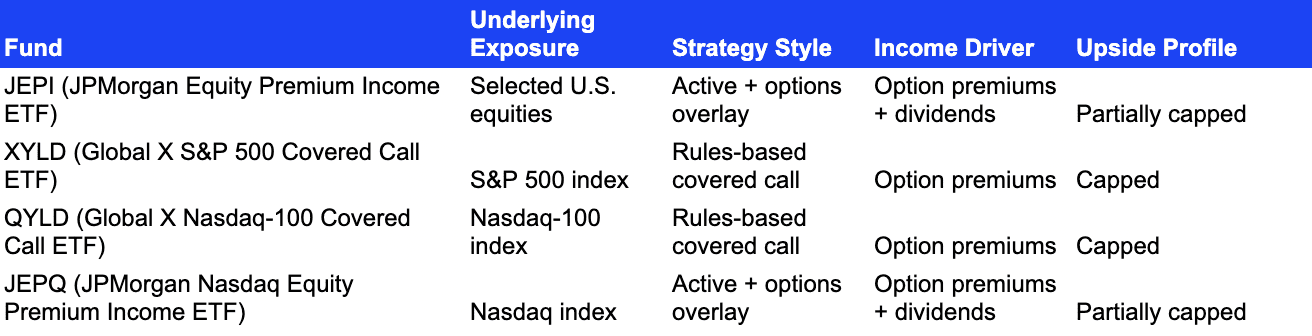

Leading Equity Covered Call Funds Globally

Covered call ETFs have surged in popularity, particularly in developed markets, as investors seek income solutions beyond traditional dividends and bonds. Key vehicles include both active and rules-based implementations that combine equity exposure with systematic option writing:

These funds demonstrate how covered call strategies can be applied at scale, blending income mechanics with broad market exposure.

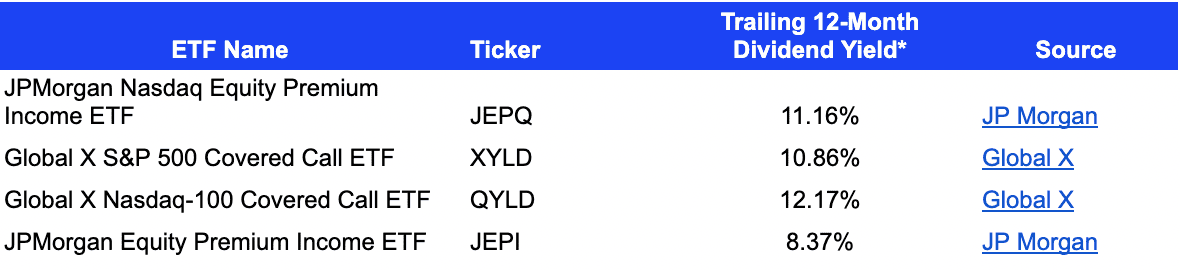

Average Distribution Yields: What Investors Are Receiving?

A key reason investors consider covered call ETFs is their relatively high distribution yields compared with broad market dividend rates. Below are approximate annual dividend yields for leading covered call ETFs (early 2026):

*As of 13th February 2026

These yields reflect current distributions, driven by option premiums amid recent volatility. In comparison, typical broad equity dividend yields remain significantly lower, often in the 1–2% range for major indices.

Covered call strategies on highly volatile stocks such as technology companies like NVIDIA, or assets such as cryptocurrencies may generate higher option premiums because option prices tend to increase with volatility. In certain market environments, this has resulted in income levels that were significantly higher than those seen in broader equity indices. However, these outcomes can vary and are not guaranteed.

Common Covered Call Strategy Variations

While the basic principle is unchanged, ETFs can implement covered call strategies in different ways depending on their goals:

- Buy-Write Strategy

A widely used approach where the fund buys equities and immediately sells call options on them. This generates instant premium income while maintaining equity exposure. The trade-off is limited upside in strong market rallies. - Rolling Covered Call Strategy

As options expire, the fund closes existing positions and sells new calls with later expirations or different strikes. This enables continuous premium capture but repeatedly resets the upside cap. - Systematic Covered Call Strategy

Options are written according to fixed rules, such as selling calls monthly or at preset strike distances. This ensures consistency, though flexibility may be reduced during sharp market moves. - Laddered Covered Call Strategy

Call options are spread across multiple strikes or maturities. Some positions prioritise higher income, while others preserve greater upside potential, creating a balance between yield and growth. - Covered Call Overlay Strategy

Calls are sold on an existing portfolio without changing its core holdings. Common in institutional mandates, this approach adds incremental income while still capping upside at strike levels.

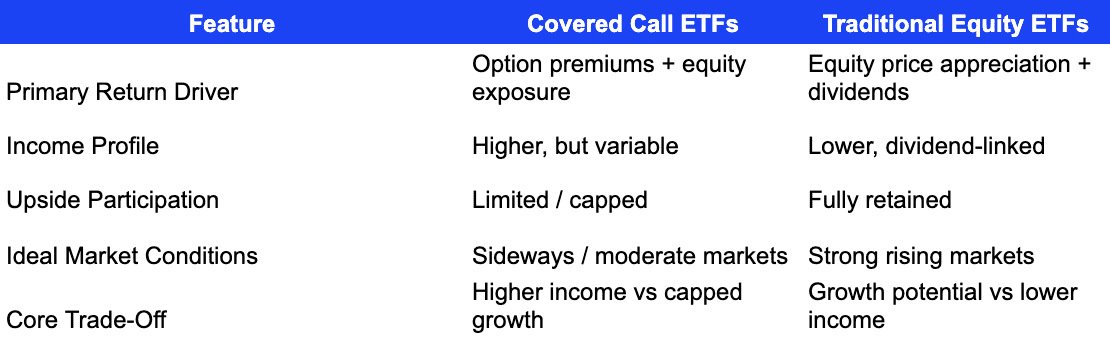

Advantages and Limitations of Covered Call ETFs

- Elevated income potential: Option premiums can boost distributions well above underlying dividend yields.

- Regular cash flow: Most covered call ETFs distribute monthly income, appealing to yield-focused investors.

- Partial downside cushion: Premium income can offset modest equity declines in range-bound markets.

Limitations

- Capped upside: Gains above the strike price are foregone, reducing long-term growth potential in strong bull markets.

- Variable income: Premium levels fluctuate with volatility, leading to distribution variability.

- Equity risk remains: Covered calls do not protect against steep market declines; losses in the underlying holdings can outweigh premiums.

This trade-off underscores why covered call ETFs are often considered income tools, not outright growth engines.

Where Covered Call Strategies Fit Within GCC Portfolios

For GCC investors, covered call ETFs typically act as complementary income tools rather than substitutes for core regional holdings. They can help boost portfolio cash flows while traditional GCC equity ETFs maintain exposure to domestic growth themes and sector dynamics.

Their income potential is closely tied to market conditions, particularly volatility. Higher volatility often leads to richer option premiums, which can support higher distributions. This makes covered call strategies attractive in volatile or range-bound markets where capital gains may be limited.

However, higher income comes with trade-offs. Covered call ETFs do not eliminate downside risk, and losses in the underlying equities remain possible during sharp market declines. Investors effectively exchange part of their upside potential for current income while retaining full equity risk.

Additionally, covered call strategies rely on deep and liquid derivatives markets, which are still limited across GCC exchanges. Consequently, these exposures are generally accessed through international ETF listings rather than local markets.

How Does NAV Erosion Impact Long-Term Investors?

NAV (Net Asset Value) erosion occurs when high distributions exceed the fund’s total return, gradually reducing the ETF’s share price over time. Some investors avoid covered call ETFs due to this “yield trap,” where attractive payouts mask principal decay, especially in rising markets where capped upside compounds the issue.

To address this, some asset managers are evolving: they now distribute only half of the generated income (e.g., option premiums) while retaining the other half in the fund to support NAV stability and reinvestment. This hybrid approach limits erosion while preserving strong yields, appealing to long-term holders prioritizing capital preservation alongside income.

Risk Awareness Remains Essential

Covered call ETFs cap upside potential and remain exposed to equity market risk. Their outcomes are sensitive to overall market direction, volatility, option pricing, and timing of distributions. As with any strategy that seeks income enhancement, investors should assess allocations within the context of total portfolio objectives, risk tolerance, and investment horizon.

Bottom line

The rise of covered call ETFs reflects a broader evolution in income investing. Traditional income sources such as dividends and coupons are being complemented by volatility-driven distribution strategies that seek to monetise market mechanics. For GCC investors, this development expands the toolkit available for income-focused portfolio design without diminishing the continuing importance of regional equity exposure.

By blending elevated cash flows with risk awareness and strategic allocation layers, covered call ETFs can play a meaningful role within diversified income strategies, particularly for investors seeking stability, predictability, and enhanced visibility into portfolio cash flows.