Pakistan’s KSE-100 is among the world’s standout equity markets in 2025, up roughly 37% year-to-date even as India’s benchmarks churn through bouts of foreign selling and tariff anxiety. As Abu Dhabi’s ETF shelf deepens, GCC investors can now access each market directly on ADX via Chimera S&P India Shariah ETF (INDI) and Chimera S&P Pakistan UCITS ETF (PKSTN) two vehicles with very different macro backdrops, risk profiles, and tax nuances, according to Bloomberg

This piece compares India and Pakistan through a GCC lens of growth, policy, flows, currency, and valuations, then maps those realities to ADX-listed ETFs that track Shariah-screened India and UCITS-compliant Pakistan equities.

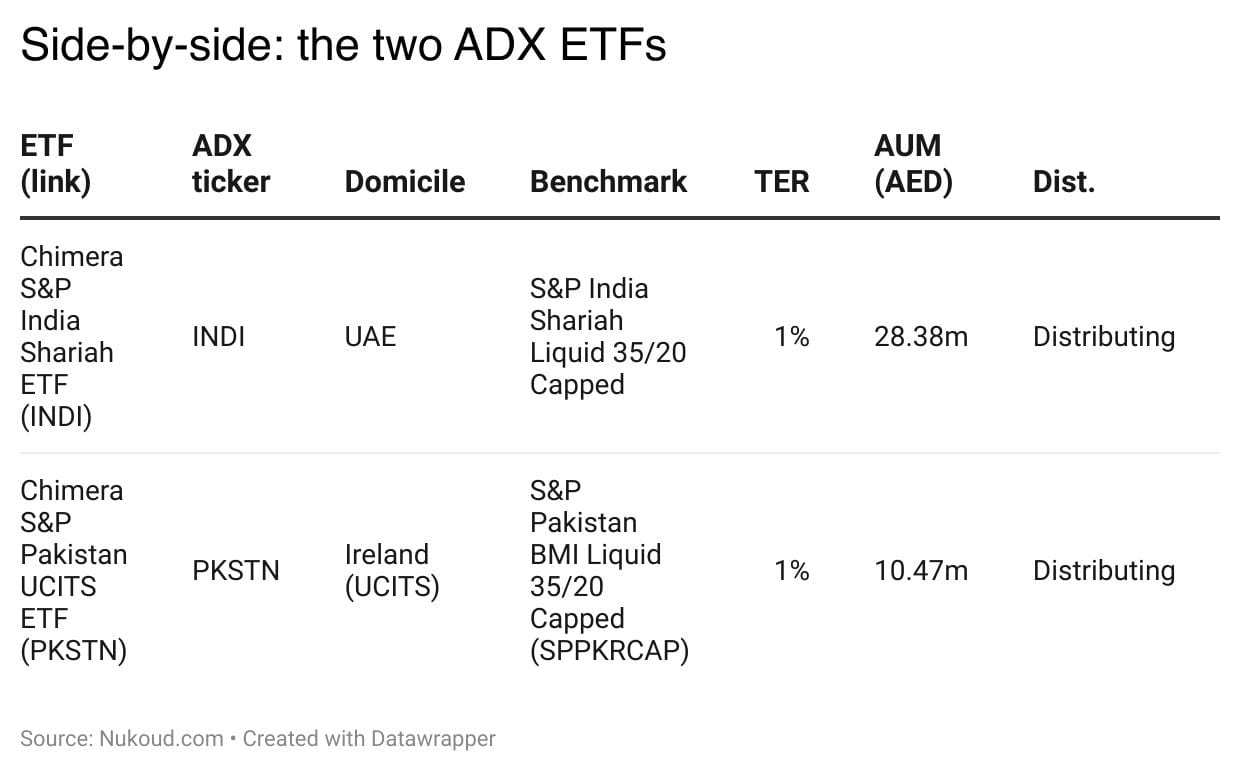

We close with a practical table (TERs, domiciles, benchmarks, AUM) and caveats specific to UAE investors (withholding, UCITS vs UAE domicile, liquidity).

India Navigating Growth and Market Flows

Indian equities remain tightly linked to the global cycle, with HSBC’s multi-asset research highlighting that growth momentum abroad is the key driver, while domestic liquidity and long-term potential growth expectations provide secondary support. Local investors continue to put a floor under prices, yet it is foreign inflows that typically fuel sharp rallies.

Valuations face pressure from an issuance surge over USD 7 billion per month in recent offerings, outpacing mutual-fund demand; foreigners have been net sellers in the secondary market while buying roughly USD 9 billion year-to-date in primaries, leaving a near-term supply overhang.

Sentiment is also clouded by policy risks, with HSBC flagging a “50% tariff shock” scenario as a major headwind to growth and the rupee, leaving equities undervalued on its models but in need of tariff relief or reform momentum to re-rate.

Near-term flows remain uneven, with September still showing net foreign outflows though at a slower pace than August’s heavy selling. On the ground, the Nifty and Sensex entered the week softer as IT stocks lagged on U.S. policy headlines, while the rupee is trading around 88 per dollar with bearish positioning elevated.

How that maps to ADX access.

Chimera S&P India Shariah ETF (INDI) tracks the S&P India Shariah Liquid 35/20 Capped Index, is UAE-domiciled, distributing, and carries a 1.00% TER. AUM: AED 28.38m; NAV: AED 3.339

Price context: INDI 1-yr return ≈ –12.8%; ex-dividend: 2025-06-30.

Pakistan Stabilizing with IMF Support

Pakistan’s economy is currently anchored by a 37-month IMF Extended Fund Facility (EFF), which completed its first review in May 2025 and remains the key policy framework for fiscal repair and foreign-exchange stability.

Inflation has begun to ease, with headline CPI falling 0.65% month-on-month in August, allowing the State Bank of Pakistan to hold its policy rate at 11% on September 15 as it balances moderating prices against still-fragile activity.

Against this backdrop of macro stabilization and reform expectations, equity markets have surged, with the KSE-100 sitting near record territory and delivering a year-to-date gain of roughly 37% as of September 22, 2025.

How that maps to ADX access

Chimera S&P Pakistan UCITS ETF (PKSTN) tracks the S&P Pakistan BMI Liquid 35/20 Capped Index (SPPKRCAP), is UCITS-compliant (Ireland-domiciled), distributing, and lists on ADX (listing date 2023-08-18). TER: 1.00%. Factsheet August 2025 shows AUM AED 10.47m; NAV AED 10.465.

Price context: indicative ~+82% 1-yr move on PKSTN (price series; check prevailing quote).

Definitions: TER (Total Expense Ratio) is the annual cost of running the fund, expressed as a % of assets. AUM (Assets Under Management) is the total value of assets in the ETF. Distributing means dividends received are paid out to investors.

Through GCC Eyes Structure, Domicile and Liquidity

From a GCC perspective, structure and domicile play a crucial role. The Chimera S&P India Shariah ETF (INDI) is UAE-domiciled and tracks a Shariah-compliant index of Indian equities, while the Chimera S&P Pakistan UCITS ETF (PKSTN) is Ireland-domiciled under UCITS rules.

A setup that can be advantageous for certain cross-border withholding-tax pathways depending on the source of dividends and treaty networks. Both funds apply S&P’s Shariah methodology, which screens sectors and financial ratios to ensure compliance, though investors should always consult the relevant index factsheet for precise criteria.

On the trading side, each ETF is listed on ADX in AED and trades during UAE hours, where investors should pay attention to bid–ask spreads and the depth of on-screen liquidity. With multiple new listings in 2024-25, including the launch of the India Shariah product in January 2024, ADX has steadily positioned itself as the region’s most active venue for ETF access.

Key Risks and Considerations

The risk picture differs sharply between the two markets. In India, elevated valuations and a surge of equity supply from IPOs and promoter block sales threatens to cap upside until foreign demand re-engages.

HSBC’s models indicate that global growth remains the dominant driver of short-term returns, while the tariff trajectory is the critical wild card. Pakistan’s rally, by contrast, is heavily policy-dependent; continued IMF program reviews, disciplined foreign-exchange management, and disinflation are essential to sustain momentum.

The State Bank of Pakistan has kept rates at 11% as of mid-September 2025, but any setbacks in reforms or funding could quickly reprice risk. At the ETF level, investors also need to consider currency exposures. INDI is denominated in AED but tracks an index based in INR, while PKSTN is an AED share class tied to underlying PKR securities.

That currency layer can introduce additional volatility relative to local benchmarks, underscoring the importance of reading each fund’s factsheet carefully for base and share-class currency details as well as distribution policies.

How to use these two funds together

One way to think about combining these two funds is through a barbell approach, INDI provides exposure to India’s large-cap, Shariah-compliant names tilted toward technology, telecom, and consumption, while PKSTN offers a more concentrated “liquid 15” basket dominated by financials, materials, and energy. Together they deliver a diversified factor of exposure across South Asia. Positioning, however, should be flow-aware.

India is contending with foreign portfolio outflows and a near-term supply glut from heavy issuance, suggesting patience on entry sizing, while Pakistan’s IMF-anchored rebound makes a disciplined rebalancing strategy prudent in the event of volatility spikes.

What It All Means for UAE Investors

India remains structurally resilient, yet near-term valuations and heavy equity supply mean the next phase of gains will likely depend on clearer global growth signals and tariff relief. Pakistan’s rally is interesting but rests squarely on the continuation of IMF support and disciplined policy execution, leaving it more fragile to setbacks.

Together, the two ADX-listed ETFs INDI, a UAE-domiciled Shariah-compliant gateway to Indian equities, and PKSTN, an Ireland-domiciled UCITS vehicle tracking Pakistan offer targeted and transparent access to markets that are otherwise difficult to tap directly. With total expense ratios of 1.00% each and Shariah screening in place, they provide GCC investors with a practical bridge into South Asia’s fiercest rivals.

As always, monitoring monthly factsheets for AUM, holdings, and distribution details is essential, but the bigger takeaway is clear: through ADX, the India–Pakistan rivalry has shifted from geopolitics to portfolios.