As of August 2025, investors are assigning a high probability to Federal Reserve rate cuts beginning as early as September. At the same timeU.S.-listed fixed income ETFs recorded nearly $19 billion in inflows during the week of August 4. .

This article unpacks how Fed easing, both expected and actual, shapes ETF performance across bond and equity sectors.

We further examine the relationship between growth and value stocks and offer a Gulf‑centric lens: how U.S. monetary policy affects GCC investors via tax implications, Sharia compliance, portfolio construction, and cross‑listing choices.

Fed Rate Cuts – Market Expectations and Timeline

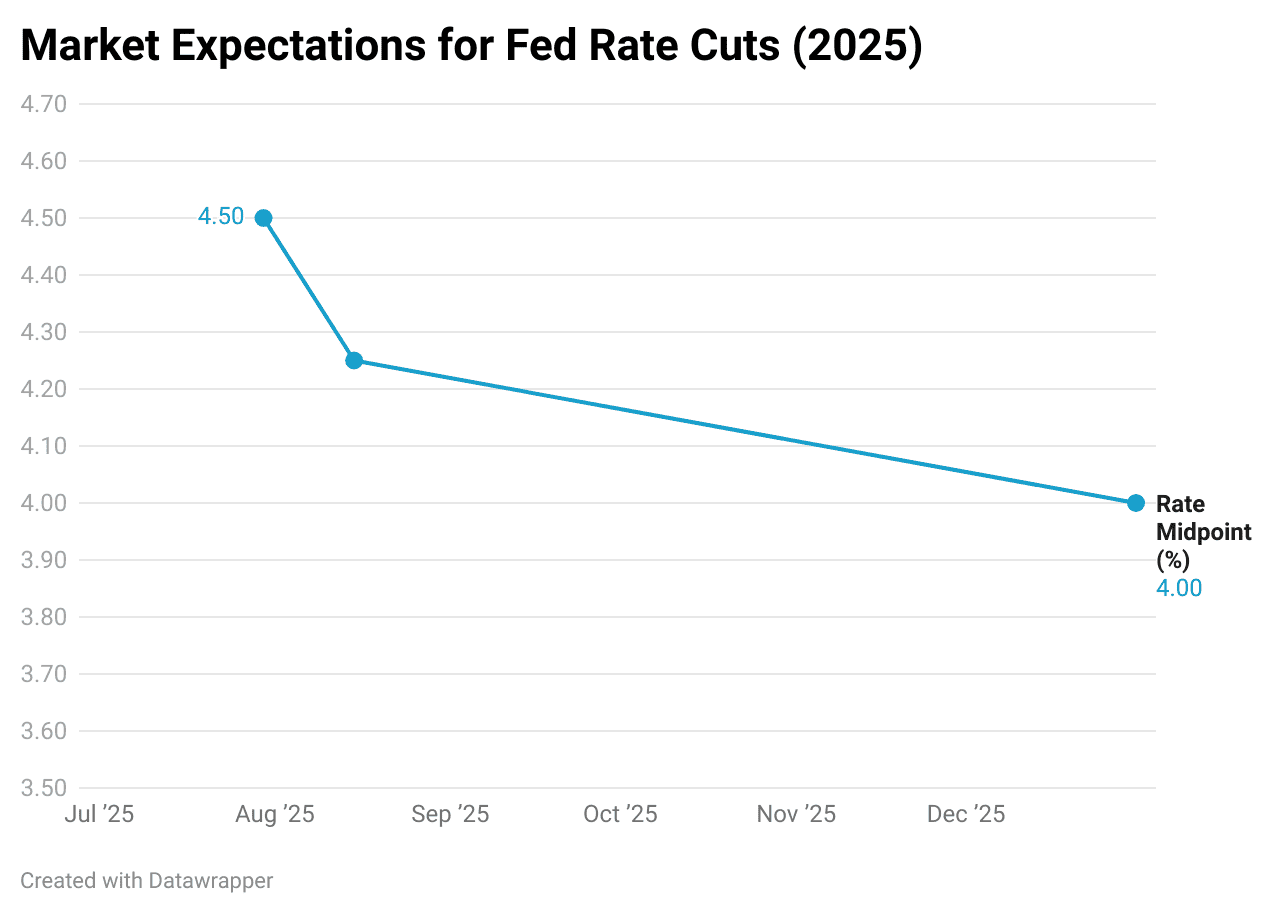

As of July 30, 2025, the Fed held rates steady at their 4.50% upper bound Fed Fund rate, with two dissenters favoring a cut.

Upcoming catalysts: Jackson Hole symposium, labor data, and consumer spending. As of August 15, equity futures rallied, pricing at least 25 bps in rate easing.

Market futures now reflect expectations of one or two cuts by year‑end, pushing terminal rate projections toward the 3.0% to3.5% Fed Funds range.

The Conventional Response of Bond ETFs to Rate Cuts

Bond prices move inversely to yields, which means that when the Federal Reserve cuts interest rates, the market value of existing bonds typically rises.

This mechanical relationship makes bond ETFs one of the most immediate beneficiaries of easing monetary policy.

Yet, the impact is not uniform across maturities.

Short-term bond ETFs, such as the Vanguard Short-Term Bond ETF (BSV US), tend to exhibit lower sensitivity to rate changes because their underlying holdings mature quickly and reset to prevailing yields.

By contrast, long-duration strategies like the iShares 20+ Year Treasury ETF (TLT US) are far more volatile in response to policy moves, with performance hinging heavily on shifts in long-term yield expectations.

In practice, investors often see the steepest gains in long-bond ETFs during the early stages of an easing cycle, though these returns can reverse quickly if inflation risks resurface.

Historical data reinforces this nuance. JPMorgan Asset Management notes that in previous easing cycles, U.S. investment-grade bonds delivered an average return of 6% over six months, compared with just 2.9% for cash equivalents.

Equity ETFs: Growth vs. Value in an Easing Environment

Equities typically benefit from Fed rate cuts, with growth stocks whose valuations rely heavily on discounted future cash flows enjoying the strongest initial boost.

Lower rates reduce the discount rate applied to projected earnings, making technology and innovation-focused ETFs such as the Invesco QQQ Trust (QQQ US) particularly sensitive to easing.

At the same time, more cyclical and rate-sensitive areas of the market can experience outsized gains.

For instance, small-cap companies and homebuilders, which often rely on credit availability, have historically rallied on easing signals.

A recent reminder came when the SPDR S&P Homebuilders ETF (XHB US) slipped 1.8% following a hotter-than-expected Producer Price Index (PPI) reading underlining that inflation surprises can quickly offset the tailwinds of lower rates.

Yet, the equity market’s relationship with Fed policy is not always straightforward. JPMorgan strategists warn that valuations for major U.S. indices are already elevated, potentially limiting the upside from cuts.

Macro hedge funds appear to share this caution: according to MarketWatch, positioning remains defensive, with managers running low beta exposures and even building up short interest in the SPDR S&P 500 ETF (SPY) despite market consensus for cuts.

The takeaway for investors, including those in the GCC, is that rate cuts may provide a lift to equities, but the scale of the rally could be muted by stretched valuations, persistent inflation risks, and cautious institutional positioning.

GCC Investor Lens

For GCC investors, Fed cuts don’t translate one-to-one with the U.S. ETF flows because of tax and domicile considerations.

Some GCC investors prefer Ireland-domiciled UCITS ETFs, which avoid the 30% U.S. dividend withholding tax. This means that while U.S.-listed ETFs may see billions in inflows after Fed easing, Gulf investors are often better served by UCITS equivalents unless cross-listed locally on ADX, DFM, or Tadawul.

Currency dynamics also matter. With most GCC currencies pegged to the dollar, rate cuts affect local liquidity directly. Dollar strength can make U.S. assets more attractive, but FX volatility in euro- or sterling-denominated UCITS ETFs adds another layer of risk.

Sharia compliance further narrows choices. Conventional bond ETFs, the most direct beneficiaries of cuts are generally off-limits for Islamic portfolios, leaving sukuk ETFs as alternatives, though they remain less liquid.

Similarly, growth equity ETFs need screening to ensure compliance with Islamic principles.

Finally, local listings remain thinly traded, raising questions around liquidity and tracking error. For now, many investors rely on international platforms for depth.

Allocation strategies may lean toward short- to intermediate-duration UCITS bond ETFs for income stability, while growth exposure can be balanced with value or defensive equity sectors to smooth volatility in a shifting rate environment.

Quantitative Lens & Historical Comparisons

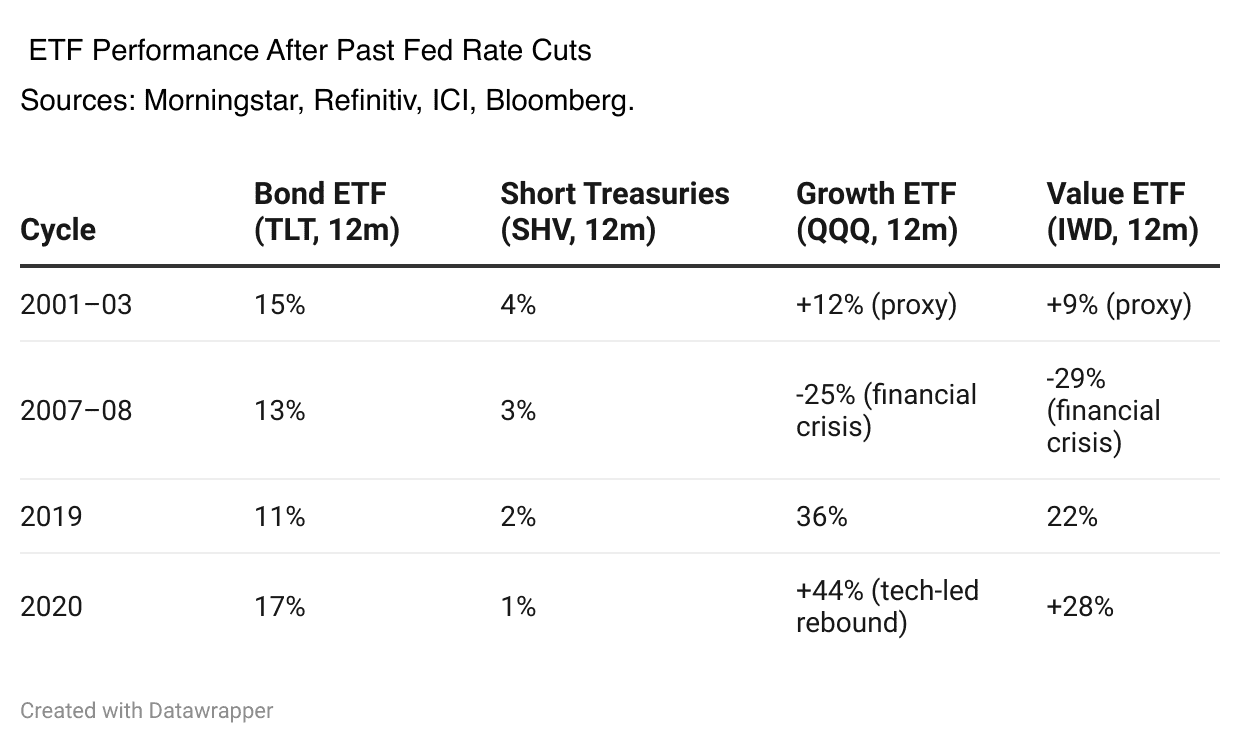

After the 2001–2003 rate cuts, long-term Treasuries proxied by back-tested indexes delivered gains of roughly 15% over 12 months, while short-term Treasury funds rose just 4%.

The 2007–2008 cuts saw iShares’ flagship long-bond ETF, TLT, advance 13% in six months before surrendering returns as inflation re-emerged.

Equities responded differently: in the 2019 “mid-cycle adjustment,” the Invesco QQQ Trust surged 36% over the following year, far outpacing the 22% rise in the iShares Russell 1000 Value ETF. Typically, growth outperforms in the early months of easing, but value and cyclical stocks often catch up if cuts extend beyond a year.

Flows add another layer of evidence: during the 2020 emergency cuts, U.S.-listed bond ETFs absorbed $45 billion in just two months, even as equity ETFs experienced outflows despite a subsequent rebound.

Risk and Caveats

While Fed easing has historically buoyed both bonds and equities, several risks complicate the current cycle.

First, much of the rally may already be priced in. If the Fed’s messaging in September is more cautious than markets expect, investors could see a “sell the rumor” effect, with muted or even negative reactions despite a rate cut.

Inflation also remains a wild card. A surprise uptick in price pressures would not only undermine the case for easing but could also pressure bond ETF valuations, particularly in the long-duration segment.

Even if the Fed cuts, structural factors such as term premium dynamics where investors demand higher compensation for holding long-dated bonds could keep long yields elevated, limiting upside for ETFs like TLT. Finally, strong employment data or resilient consumer spending could push the Fed to delay or temper cuts, unraveling expectations that have already driven flows into fixed income.

Key Takeaways for GCC Investors

For GCC investors, the implications are nuanced rather than binary. Short- to intermediate-maturity bond ETFs, particularly those available in UCITS form, may offer more stability in a volatile cycle by reducing sensitivity to shifts in long-term yields.

On the equity side, rate cuts often favor growth stocks, but valuations are already stretched, making a diversified mix that includes value and defensive sectors prudent.

Using UCITS ETFs where possible remains key to minimizing withholding tax drag while staying aligned with local regulatory frameworks.

Investors must also weigh currency exposure: while most GCC currencies are pegged to the U.S. dollar, hedging or allocation decisions can still shift outcomes depending on fund denomination.

Perhaps most importantly, Fed communications themselves may prove just as market-moving as the cuts, making it essential for Gulf investors to monitor not only the policy moves but also the tone and guidance surrounding them.