Markets are being pulled in opposite directions and the GCC is no exception. After three weeks of conflict, regional performance has diverged: UAE equities, including ADX and DFM, have declined, while Saudi Arabia has remained relatively resilient.

Oil has been the dominant driver, swinging sharply day to day as markets react to shifting supply and demand dynamics, with ripple effects across key sectors such as real estate and transportation. Gold, however, has remained surprisingly steady, failing to fully reflect a traditional flight to safety, while Bitcoin has delivered uneven performance.

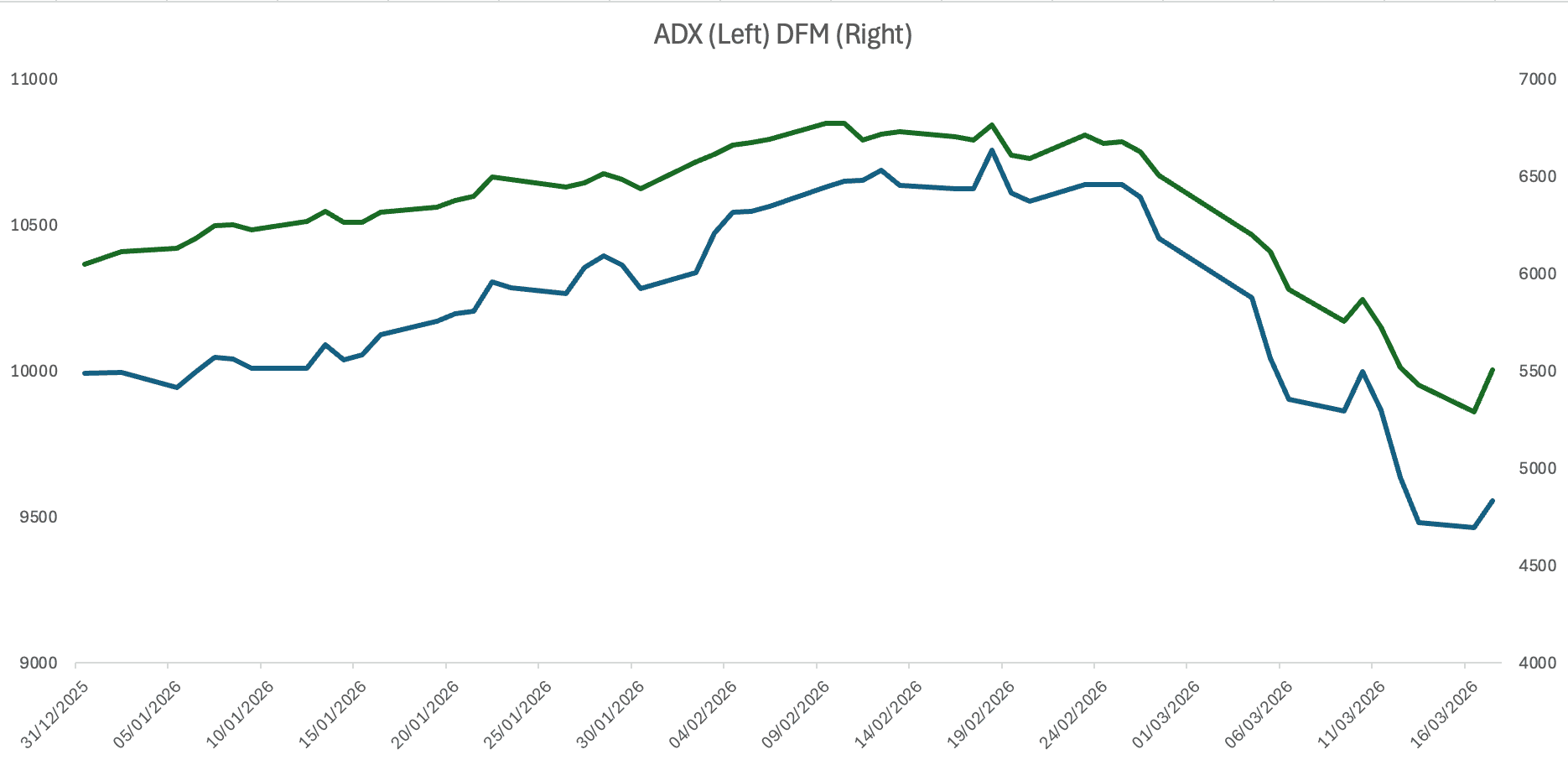

GCC Equities: Divergence Beneath the Surface

The UAE has been the clear pressure point. Both the Dubai Financial Market and Abu Dhabi Securities Exchange have reversed part of their strong pre-war rally, with Dubai down more than 18% since late February (as of 2026-03-16), marked by repeated daily declines of 2-3% across multiple sessions.

In Dubai, weakness has been concentrated in real estate, banks, and transport-linked names, with stocks such as Emaar Properties, Emirates NBD, Salik Company, and Air Arabia seeing sustained selling pressure as investors price in disruptions to mobility, tourism, and transaction activity.

Abu Dhabi has also weakened, though less sharply, with declines across banks and property names, partially offset by institutional flows and sovereign-linked support. Trading activity has remained elevated, pointing to active repositioning rather than illiquidity.

In response, the Central Bank of the UAE has launched a AED 1 trillion liquidity support package for the banking sector, aimed at stabilizing financial conditions and ensuring continued credit flow, a move that underscores the scale of policy backing behind the system.

ETF activity reflects this shift. The Chimera S&P UAE UCITS ETF and Chimera ADX Index ETF have tracked the drawdown, with price action and liquidity pointing to selective de-risking rather than broad capitulation.

Saudi Arabia has been comparatively resilient.

The Saudi Exchange (Tadawul) has seen volatility, but moves have been more contained, with declines generally limited to low single digits on risk-off days.

Support has come from Saudi Aramco, which has benefited from higher crude prices, while banks and domestic sectors have remained relatively stable, reflecting deeper local liquidity and less direct exposure to logistical disruptions.

This is visible in ETFs. The Albilad MSCI Saudi Arabia ETF has shown more stable performance, with shallower drawdowns and steadier trading patterns, reinforcing Saudi Arabia’s role as a relative anchor within the region.

Elsewhere, markets have been volatile but functional. Qatar has seen sharper swings, including multi-day moves of 2-4% in both directions, with banks and energy-linked names driving performance. The Al Rayan Qatar ETF has mirrored this volatility without indicating sustained outflows.

Oman has been relatively steady, recording modest gains on several sessions, while Kuwait and Bahrain have posted milder declines, reflecting risk sensitivity without systemic stress. Across these markets, ETFs suggest investors are adjusting exposure rather than exiting entirely.

Oil: The War’s Primary Transmission Channel

Oil has been the clearest barometer of the conflict, reacting almost daily to developments on the ground.

The closure of the Strait of Hormuz initially sent prices sharply higher, briefly pushing crude futures toward $120 per barrel, as markets priced in severe supply disruption. At the same time, physical crude benchmarks surged even more aggressively, highlighting immediate constraints on export flows rather than just futures-driven sentiment.

Prices have since eased back toward the high-$90s as pressure mounted to reopen shipping lanes, strategic reserves were tapped, and some flows toward key Asian buyers resumed.

Even so, oil remains elevated because the underlying disruption persists. The market is now balancing tight supply, fragile logistics, and uncertainty around the duration of the conflict.

For GCC economies, this reinforces oil’s dual role: it strengthens fiscal positions while simultaneously disrupting trade, transport, and downstream sectors — pressures that are now visible in equity and ETF performance.

Gold and Bitcoin: Two Very Different Hedges

Gold has moved higher in a more measured way, supported by geopolitical risk and inflation expectations.

Its role remains traditional, a steady store of value during uncertainty, increasingly accessible in the region through products such as the Albilad Gold ETF.

Bitcoin, by contrast, has behaved differently. Holding near $73,700 (as of 2026-03-17), it has remained firm even as regional equities sold off. Rather than acting as a risk asset, it is trading more like a global liquidity proxy, reflecting broader macro positioning rather than regional developments.

USD: A Quiet Driver in the Background

The U.S. dollar has remained firm, adding another layer of pressure on regional markets as tighter global financial conditions feed through to GCC liquidity. For dollar-pegged economies, this limits monetary flexibility, even as domestic conditions soften. The result is an additional divergence: oil supports revenues, but a strong dollar tightens financial conditions, pulling markets in opposite directions.

The U.S. dollar has remained firm, adding another layer of pressure on regional markets as tighter global financial conditions feed through to GCC liquidity. For dollar-pegged economies, this limits monetary flexibility, even as domestic conditions soften. The result is an additional divergence: oil supports revenues, but a strong dollar tightens financial conditions, pulling markets in opposite directions.

A Fragmenting Market, Seen Through ETFs

Three weeks into the conflict, the key shift is structural. The GCC is no longer moving as a single oil-linked trade. Notably, markets have shown signs of stabilisation in the latest session, with several GCC indices trading higher as of today.

The UAE remains the most exposed market, with sector-level weakness in real estate, banking, and transport feeding directly into ETF performance. Saudi Arabia is acting as a relative stabiliser, supported by oil revenues and domestic liquidity. Smaller markets continue to trade with volatility but remain intact, while Bitcoin and gold highlight diverging forms of defensive positioning.

What ties this together is the ETF layer. Across the region, ETFs show that investors are not exiting, they are reallocating, trimming exposure to the most affected sectors and markets while maintaining positions where resilience is strongest.

In this environment, ETFs are not just tracking performance. They are mapping the fragmentation of GCC markets in real time.