As Washington and Tehran head into another round of nuclear talks, GCC investors are focused less on rhetoric and more on market reaction.

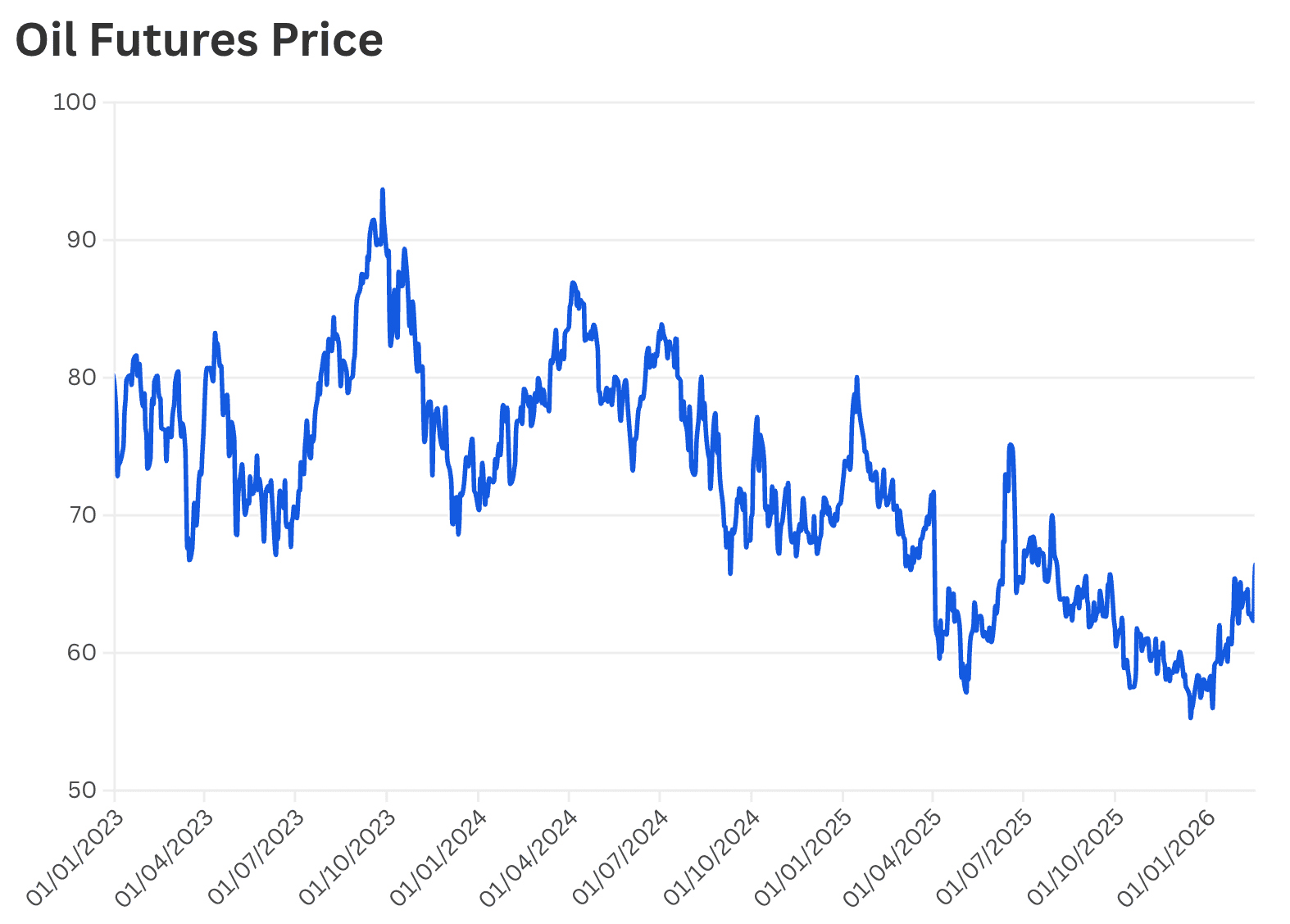

Regional equities have edged cautiously lower but remain orderly, with banks and large-cap names showing resilience. There is no sign of broad risk liquidation. Oil has firmed on geopolitical premium, but it remains a secondary driver to how equity markets interpret the probability of escalation versus containment.

For now, markets appear to be pricing tension, not conflict. The base case reflected in asset prices is continued diplomacy with elevated headline risk.

For investors, the question is not about oil alone, but whether regional equities are facing temporary volatility or a shift in risk regime. So far, positioning suggests caution rather than capitulation.

GCC Equities Feeling the Strain

Gulf equity markets have recently oscillated in response to shifts in geopolitical sentiment. On Feb. 20, 2026, UAE markets fell, with Dubai and Abu Dhabi indices down roughly 0.3% each, as traders reacted to escalatory rhetoric from Washington and Tehran. Key names such as Aldar Properties and major banking stocks posted modest declines amid cautious positioning.

Conversely, signs of progress in nuclear negotiations earlier this month triggered rallies across GCC bourses, with Saudi Arabia’s benchmark advancing and gains broadening to Dubai and Qatar.

Financial heavyweights including Saudi National Bank and Qatar National Bank benefited from softer geopolitical pricing and steady oil support.

The recent volatility has also coincided with MSCI rebalancing flows, which tend to amplify short-term moves in large-cap constituents as passive funds adjust holdings, adding a technical layer to an already sentiment-driven market.

This ebb and flow underscores the dual influence of geopolitics and market psychology: positive diplomatic signals tend to lift equities, while escalatory rhetoric or naval activity near the Strait of Hormuz weighs on risk assets.

-

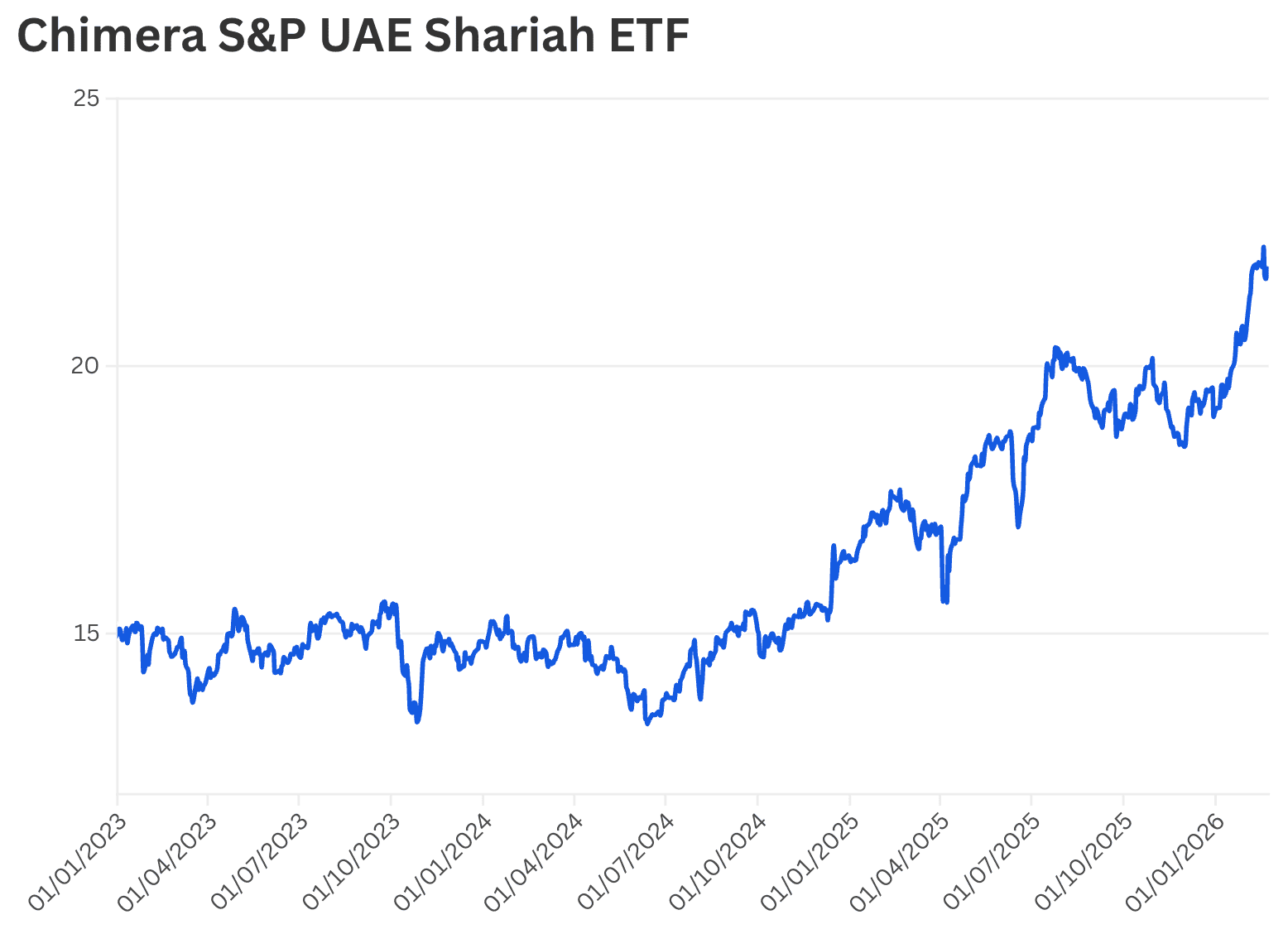

Chimera S&P UAE Shariah ETF tracks a Shariah-compliant UAE equity benchmark, providing single-ticket exposure to major UAE stocks and often acting as a barometer of local retail and institutional sentiment.

-

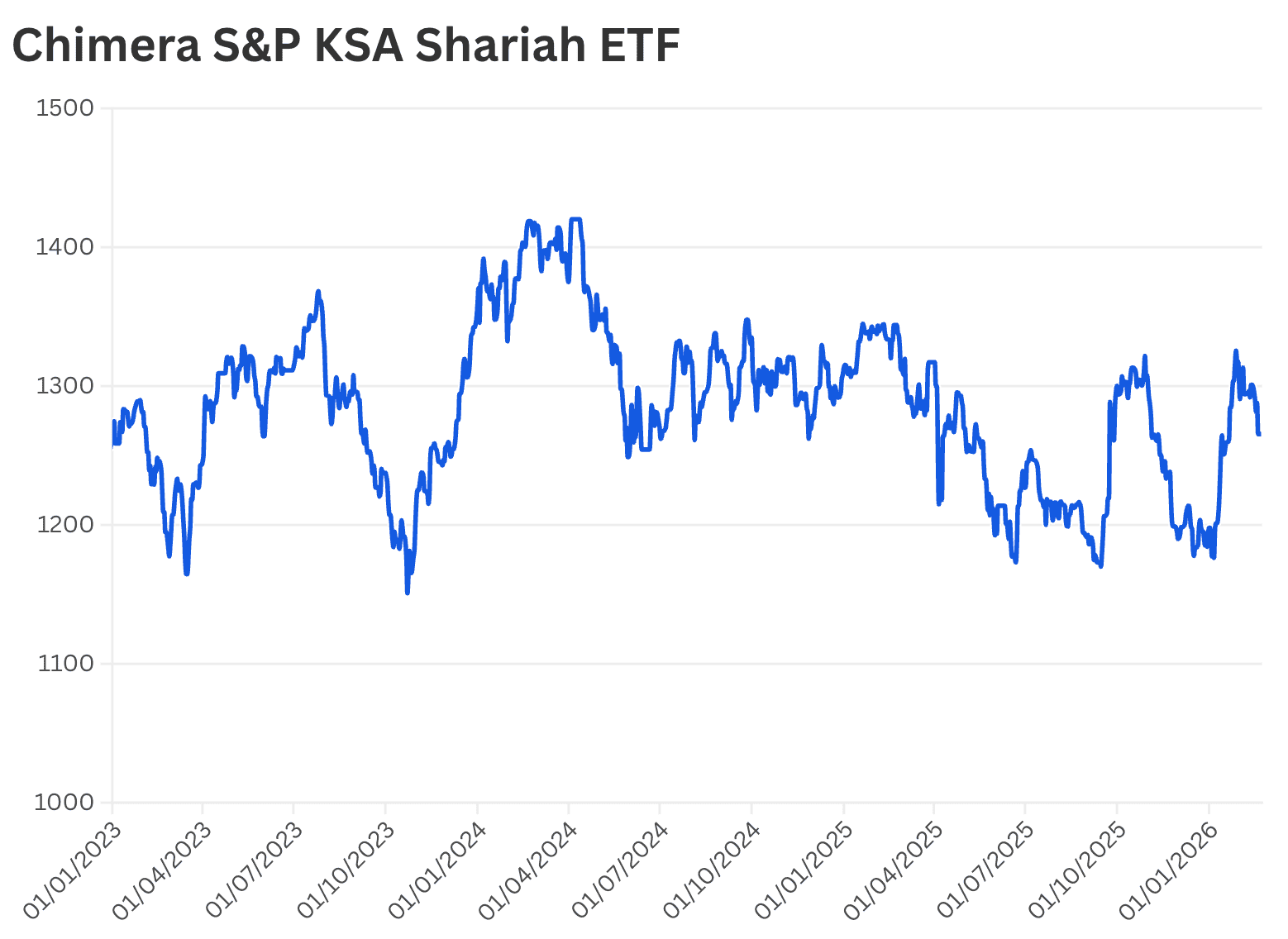

Chimera S&P KSA Shariah ETF similarly delivers Saudi equity exposure with a Shariah tilt, reflecting investor appetite in the Kingdom’s largest market

During recent tension-driven selloffs, these ETFs have tended to reflect the same patterns seen in underlying markets, wider drawdowns during fear spikes and partial recoveries as diplomatic optimism builds. Region-focused ETF flows, while smaller in absolute scale than global thematic funds, can nonetheless amplify local sentiment, with flows accelerating on both dips and rallies.

Sector & Flow Impacts Beyond Energy

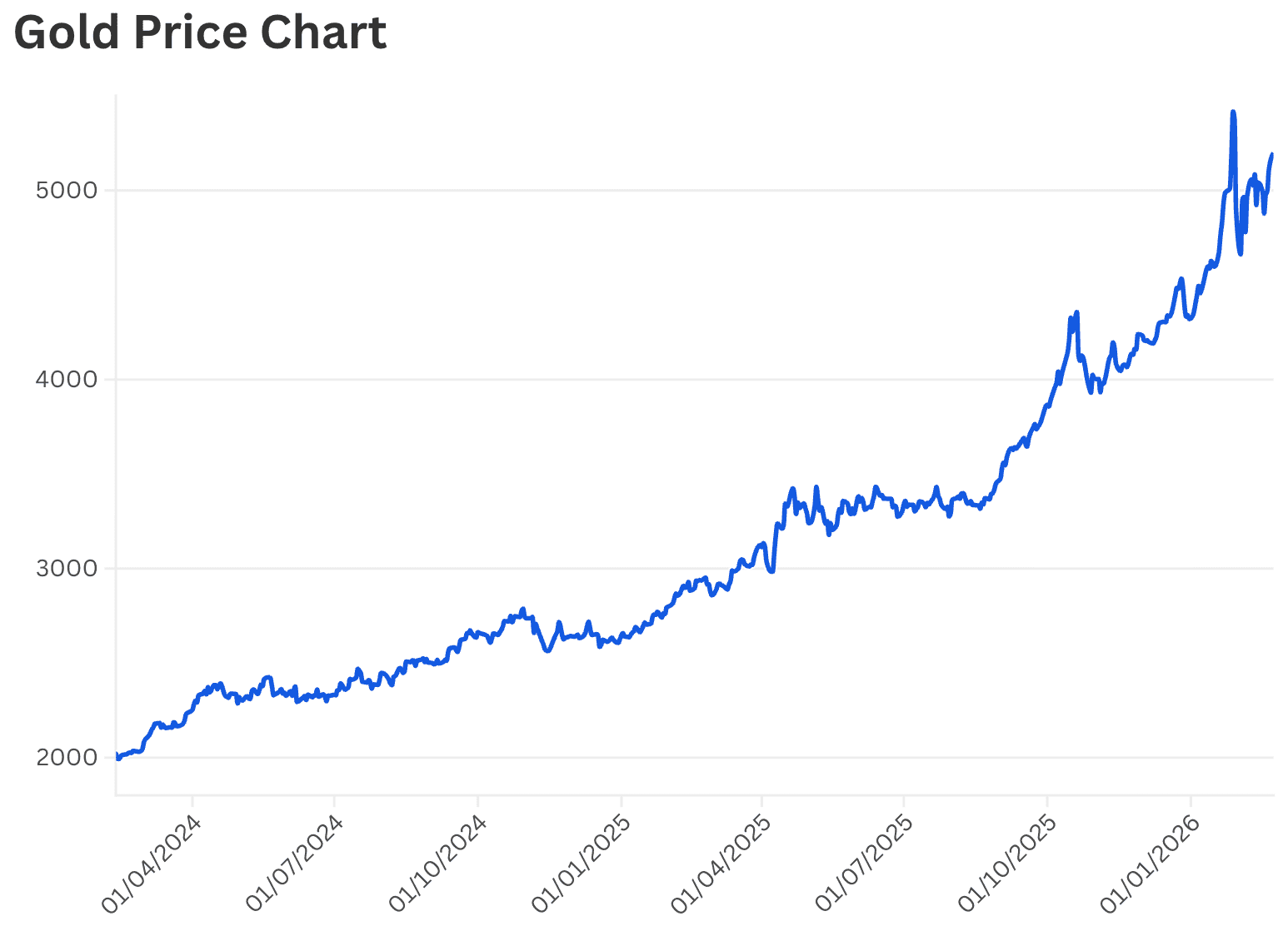

The current environment has also boosted traditional haven assets such as gold, which has climbed toward recent peaks alongside crude. Rising safe-haven demand reflects investor caution and broader risk repricing, as geopolitical instability feeds uncertainties over inflation and global growth.

Importantly, banking and financial sectors in the GCC show differentiated reactions: names with strong domestic credit growth and resilient fundamentals have outperformed during risk rallies, while those more sensitive to external flows have lagged during geopolitical selloffs, highlighting intra-market dispersion.

Predictions

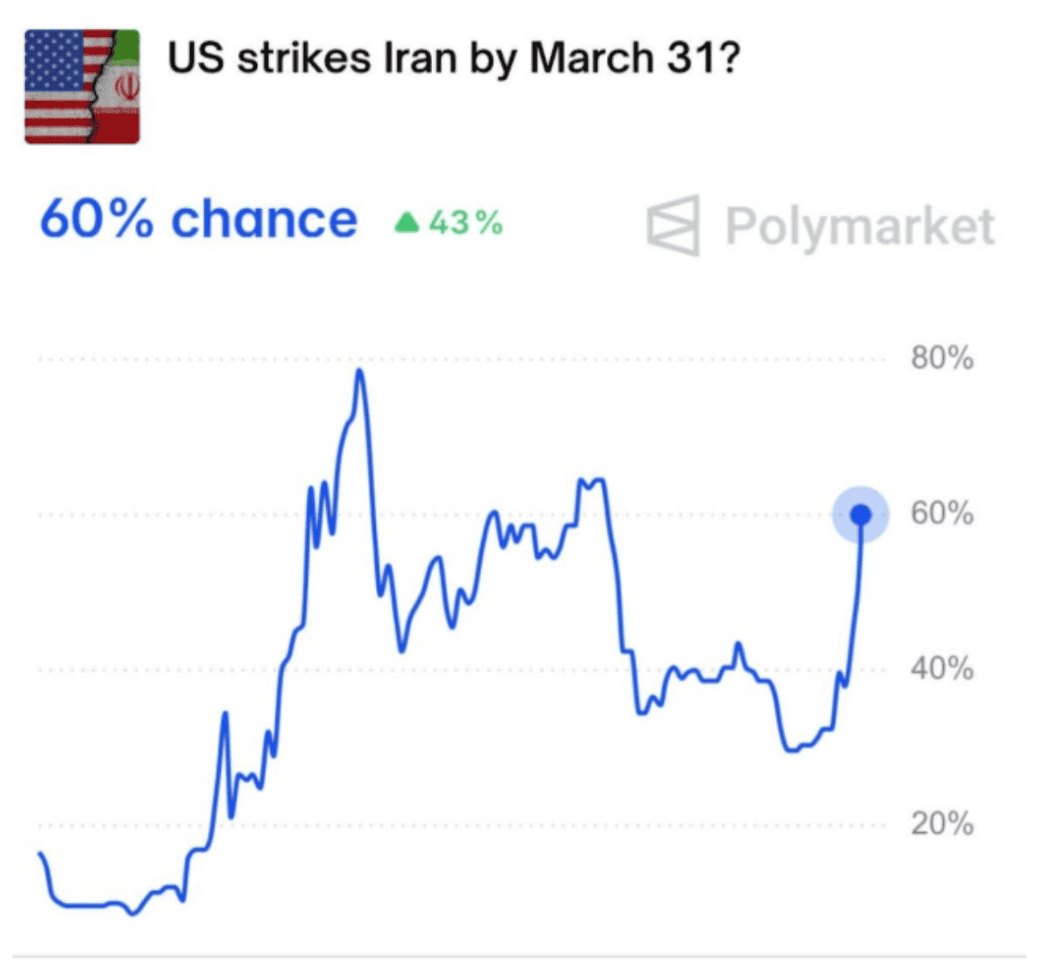

Will Trump do it this time? Reports in the media mentioned that some of Trump’s advisors are advising against an Iran strike. The fear is that the US enters a prolonged war that could put US troops and the region in danger. But recent mobilization and other leaks show that Trump is adamant on dealing with what he believes are threats to the US and the region. Odds of a US strike by the end of March have increased over the past week but remain at 60%. While headlines make it look imminent, the situation could be more complicated.

Why This Matters to Investors

For GCC investors and allocators, the U.S.–Iran dynamic complicates the risk/reward calculus:

- Oil prices are trading with a geopolitical overlay that can trigger sharp swings independent of fundamentals.

- Equity markets are responding not just to energy revenue expectations, but to risk sentiment tied to diplomatic headlines.

- Safe-haven flows into gold and select defensive assets suggest a multi-asset repricing around macro uncertainty.

- Policy and military developments, especially actions affecting the Strait of Hormuz remain key short-term drivers.

Previously, regional tensions meant buying the dip for the region. Volatility increased and equities dropped as events unfolded, but rebounded swiftly sometimes before the end of the conflict. To learn more about recent performance read our previous article on the topic.

In short, Gulf markets are watching geopolitical momentum, and positioning accordingly. Even as diplomacy remains alive, the risk premium embedded in pricing across energy, equities, and credit reflects an environment where conflict risk, however remote, still commands investor attention.