Trading activity in U.S.-listed GCC ETFs accelerated sharply into the U.S. close on February 19, 2026, reinforcing the sense that global investors are leaning more decisively into the region. However, the timing of the surge was not coincidental. The session coincided with the quarterly MSCI index rebalance, a scheduled event that often generates significant turnover as passive and benchmark-aware managers adjust positions to reflect updated index weights.

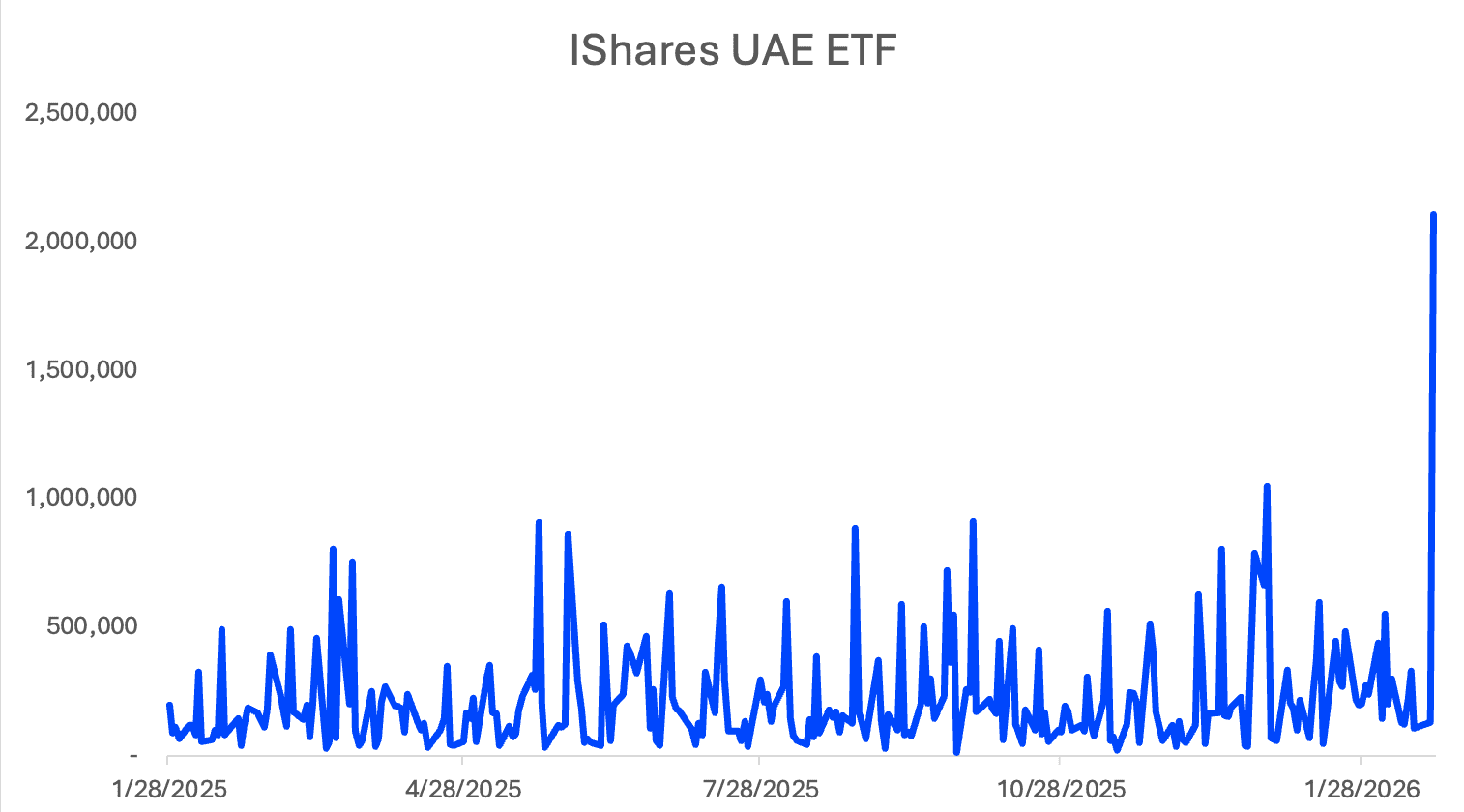

The iShares MSCI UAE ETF finished the session at an all-time high of $22.23 earlier this week, and by the market close volumes had swelled to approximately 2.1 million shares. That compares with a 20-day average of roughly 250,000 shares, underscoring how unusual the day’s activity was. While the early spike initially suggested opportunistic buying, the sustained flow into the closing auction aligns more closely with index-driven adjustments tied to MSCI’s quarterly rebalance process.

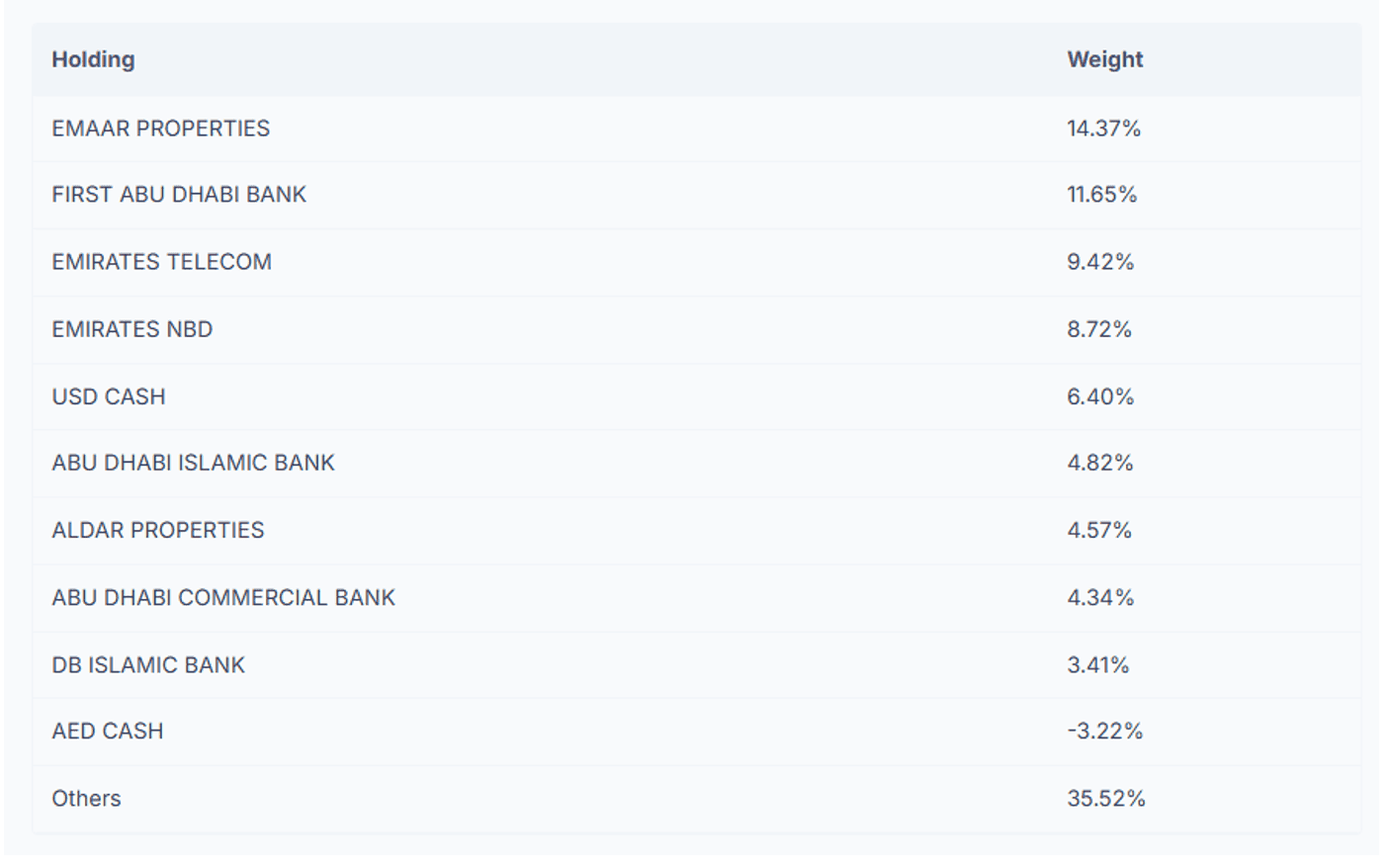

Top Holdings in the UAE ETF

Volume Trends in the UAE US-Listed ETF

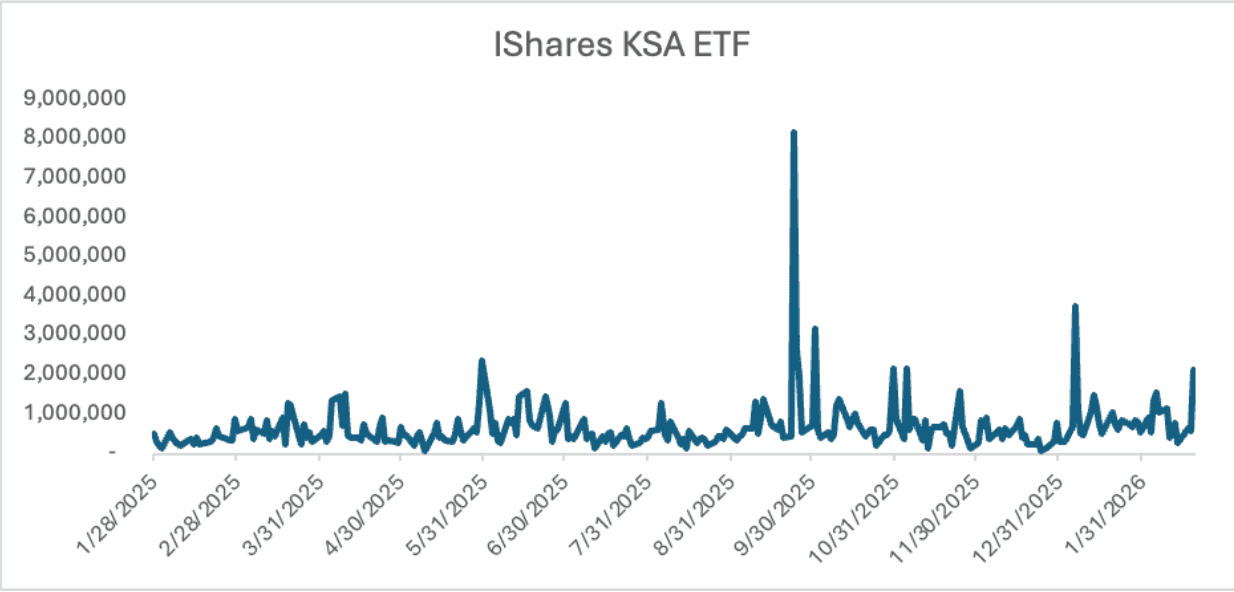

Saudi Arabia exposure saw a similar dynamic. The iShares MSCI Saudi Arabia ETF closed with roughly 2.021 million shares traded, well above its recent 20-day average near 780,000 shares. Although the fund did not mark a new 52-week high, the magnitude and concentration of trading into the close point to systematic repositioning rather than discretionary momentum alone. Rebalance events often trigger simultaneous inflows and outflows as managers recalibrate exposures, amplifying volume across both primary ETFs and underlying local shares.

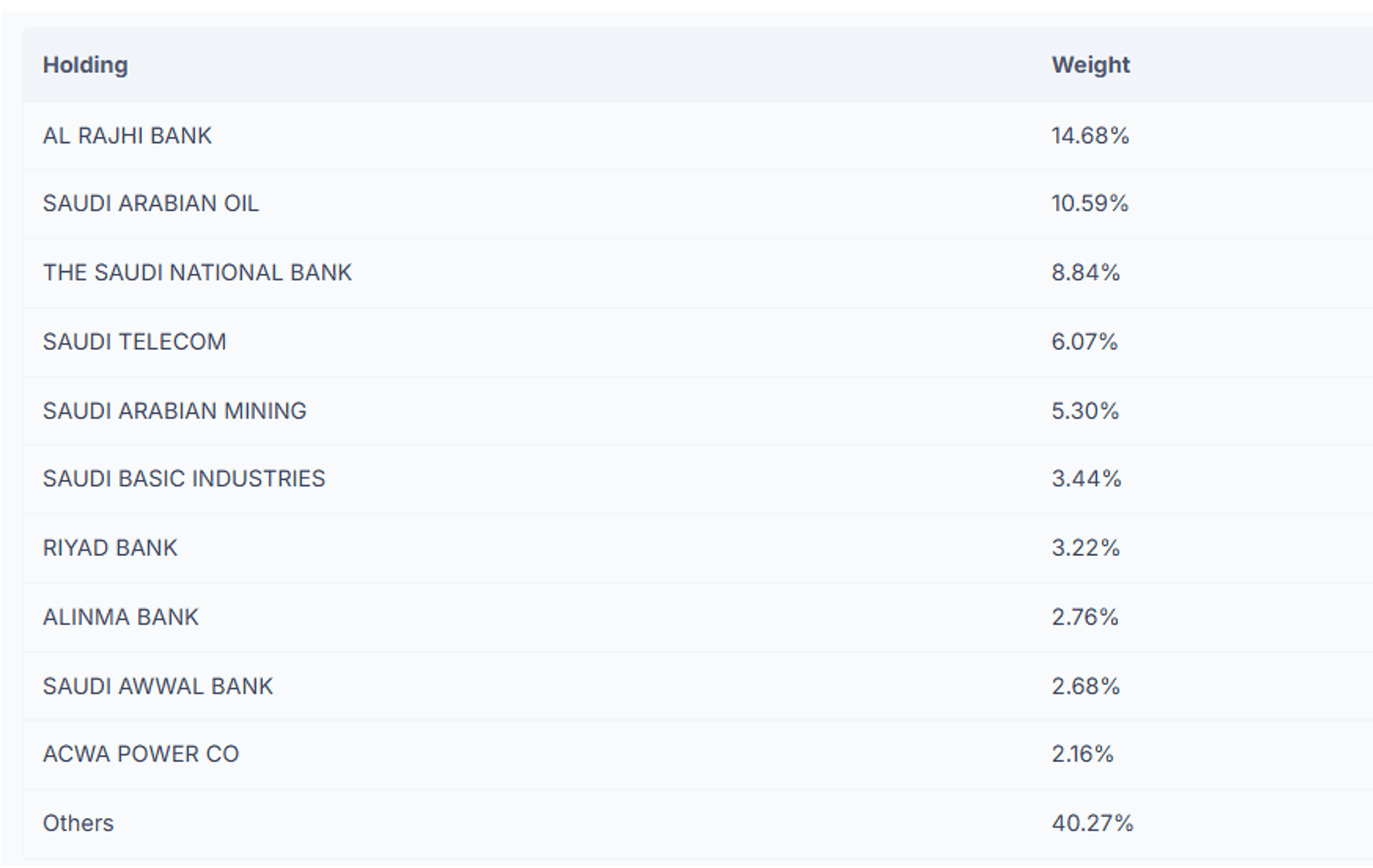

Top Holdings in the KSA ETF

Volume Trends in the KSA US-Listed ETF

The UAE fund’s strength remains closely linked to the performance of its largest constituents. Emaar Properties, which represents approximately 14% of the index, has reached fresh highs this week, reflecting continued resilience in Dubai’s real estate market. The second-largest holding, First Abu Dhabi Bank, at roughly 11.5% weight, remains a proxy for liquidity conditions and capital formation across Abu Dhabi. During MSCI rebalance windows, shifts in weightings for such large-cap constituents can materially influence ETF trading patterns, particularly when passive vehicles must execute size in a compressed time frame.

The broader backdrop for this renewed interest remains constructive. Saudi Arabia’s continued opening to foreign investors, along with sustained development across the UAE’s capital markets ecosystem, has made both markets increasingly accessible to global allocators. Activity on the Abu Dhabi Securities Exchange (ADX) and the Dubai Financial Market (DFM) has drawn more international attention over the past year, particularly as investors look to diversify emerging market exposure beyond traditional Asia-heavy allocations.

What makes this moment notable is not simply that prices are firm, but that volume expanded dramatically during a known structural catalyst. Quarterly MSCI rebalances frequently act as inflection points, revealing where passive capital must flow and where active managers choose to lean in or lean away. The fact that both UAE and Saudi funds experienced outsized turnover alongside firm pricing suggests that, beyond mechanical reweighting, there may be genuine incremental demand emerging for GCC exposure.

If elevated turnover persists beyond the rebalance window, it would reinforce the idea that international capital is increasingly comfortable expressing exposure to Gulf equities through U.S.-listed vehicles. For a region once considered peripheral within emerging markets portfolios, that would mark a meaningful structural shift rather than a one-day index event.