Gold and silver declined sharply in March and April despite heightened geopolitical tensions, defying typical safe-haven expectations. Gold fell from its record high of $5,405/oz (reached on 29 January 2026) to a key technical support level near $4,075/oz, its 200-day moving average, representing a peak-to-trough decline of approximately 24%. Silver's drawdown was even steeper, falling nearly 28% from its March peak before recovering. According to the World Gold Council's Gold Return Attribution Model (GRAM), the primary culprit was a sharp drop in market volatility: as risk appetite returned and US equities rallied, the safe-haven premium collapsed. Compounding this, central banks and leveraged investors used gold as a source of liquidity and funding during the stress episode, a dynamic the WGC explicitly flagged as a headwind while the Strait of Hormuz disruption persisted.

As of 16 May, 2026

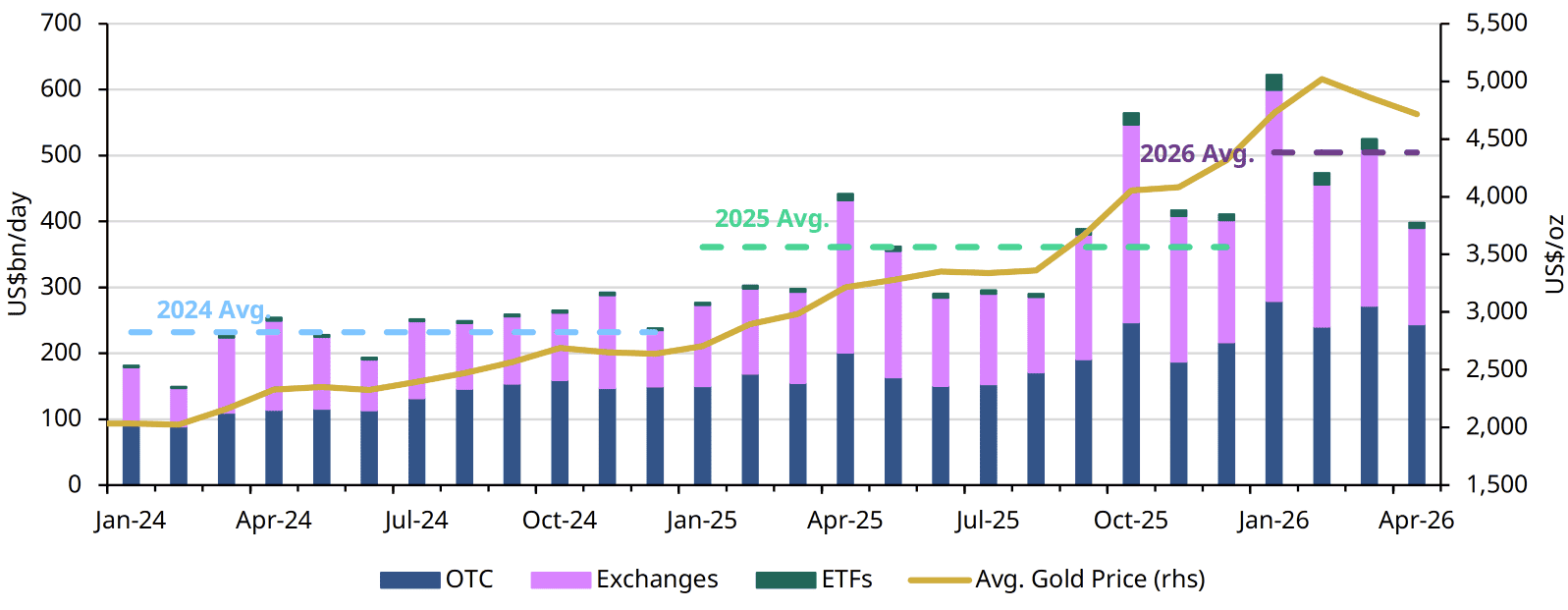

COMEX managed money net long positions remained firmly in neutral territory, rising only modestly to 5 tonnes ($1bn) in April. Yet gold closed the month at $4,611/oz, essentially flat (0.1%), and retained a year-to-date gain of 5.6% in USD terms, evidence of the resilience beneath the volatility. The rebound was also visible in fund flows: global gold ETFs recorded $6.6bn in net inflows in April alone, the strongest monthly figure of 2026, lifting total holdings to 4,137 tonnes, the third highest level ever recorded. Europe led with $3.7bn, followed by Asia at $1.8bn, suggesting investors were actively buying the dip rather than exiting the trade. While trading volume dropped from the previous month, it remains above the 2025 average but below the 2026 average.

(Sources: World Gold Council Gold Market Commentary April 2026, published 7 May 2026; WGC ETF Flows Report May 2026)

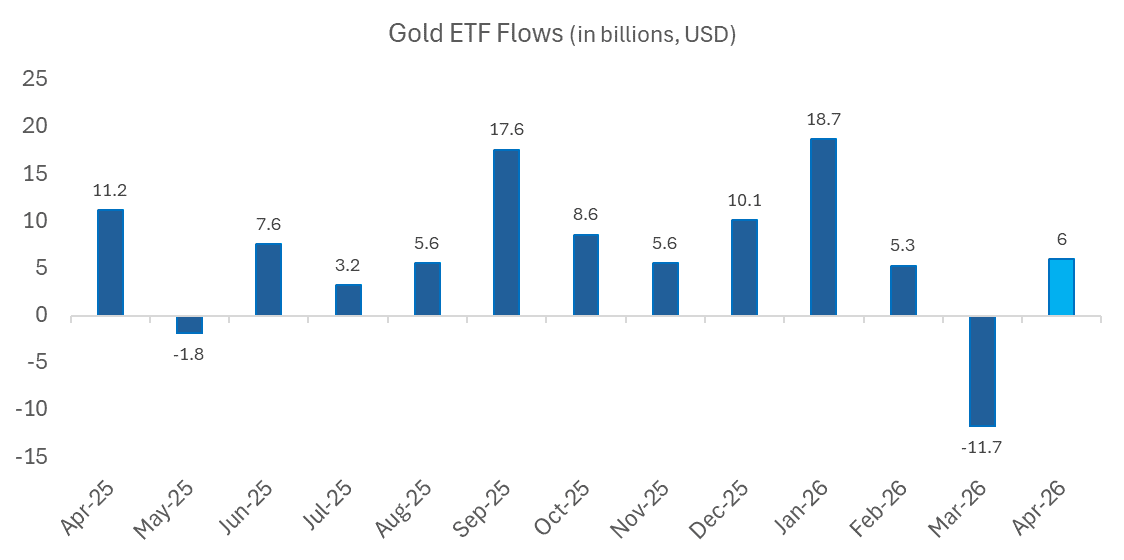

ETF Demand declined in March and rebounded in April

What distinguished this correction from prior commodity sell-offs was the resilience of institutional positioning. Gold ETF lost a significant amount during March of 2026, equivalent to 11.7 billion in net outflows, the first major drawdown since May of 2025. Despite the price drawdown, global gold ETFs rebounded in April, amassing $6.6 billion in net inflows, with all regions contributing. Gold ETF flows continue to be net negative since the beginning of the war, but net positive for the year to date.

Source: Bloomberg

This lifted total AUM back to $615 billion and collective holdings to 4,137 tonnes, the third highest level ever recorded (just below the record of 4,176t set on 27 February 2026). Source: World Gold Council, 7 May 2026. Europe led the regional recovery, posting $3.7bn in inflows driven by the UK, Switzerland, and Germany as investors responded to geopolitical risk and energy price pressure. Asia extended its inflow streak to an eighth consecutive month, adding $1.8bn, with Hong Kong SAR recording a single-month record of $732mn following a new product listing. North America reversed its March outflows with $1bn in inflows, though flows softened late in the month as the dollar strengthened and yields rose.

For GCC investors, access comes primarily via international brokerage platforms and cross-listed products available through Abu Dhabi and Dubai. The largest global vehicles, SPDR Gold Shares (GLD) and iShares Gold Trust (IAU), offer scale, liquidity, and tight bid-ask spreads. European UCITS structures from WisdomTree and iShares have also gained traction among Gulf family offices due to their tax efficiency and accessibility through regional private banks.

Silver Is No Longer Just a High-Beta Gold Trade

Silver's rebound deserves a separate analytical lens. While gold remains primarily a monetary asset driven by real rates and central-bank demand, silver sits at the intersection of monetary metals and industrial supply chains, electrification, solar, semiconductors, AI data centres, and power infrastructure.

"J.P. Morgan Global Research forecasts silver prices averaging around $81/oz in 2026, pointing to demand from industrial uses and noting that silver is increasingly showing up in AI data centres." J.P. Morgan Global Research, 2026

The global silver market is forecast to remain in deficit for a sixth consecutive year in 2026. Physical investment demand is expected to rise 20% to 227 million ounces, its highest in three years, while total supply grows only 1.5% to 1.05 billion ounces. Industrial demand is projected at 650 million ounces, slightly lower due to price-driven thrifting in solar photovoltaics, but still structurally robust given electrification and compute infrastructure tailwinds.

A Uniquely Complex Portfolio Balancing Act

For GCC investors, the dynamic is distinctive: the region simultaneously sits at the epicentre of the geopolitical catalyst and benefits economically from higher energy pricing. Elevated oil revenues support regional fiscal balances and local equities while geopolitical escalation simultaneously increases demand for defensive allocations such as gold and silver.

This creates an increasingly visible portfolio balancing pattern among regional allocators. GCC equity exposure benefits from stronger crude revenues; bullion ETFs act as a hedge against escalation risk, inflation surprises, or broader global market instability. As ETF adoption expands across the Gulf, products such as GLD, IAU, and SLV are being integrated into tactical asset-allocation frameworks alongside equities, Sukuk, and thematic technology exposures rather than treated purely as long-term stores of value.

For Saudi-based investors, the AlBilad Gold ETF (Tadawul: 9405) provides a Shariah-compliant, on-exchange route to physical gold exposure, with no international brokerage or bullion storage required. The fund manages approximately SAR 255.85 million in AUM with 7.01% YTD returns as of May 18, 2026. As the region's first Shariah-compliant commodity gold ETF on Tadawul, it remains the most direct locally listed vehicle for Gulf investors seeking gold within an Islamic finance framework.

The Structural Case Is Larger Than the Headlines

Gold and silver are no longer trading purely on Iran risk or short-term geopolitical stress. The rebound increasingly reflects a broader reassessment of inflation persistence, sovereign debt sustainability, AI-driven infrastructure spending, and global liquidity conditions.

If tensions continue easing, both metals could face bouts of short-term profit-taking. But the structural story sits elsewhere: the growing recognition that the global economy is entering an era of enormous capital requirements, infrastructure spending, and sovereign borrowing. Historically, those environments have supported precious metals over the long run, particularly when investors question whether traditional fiscal frameworks can absorb those pressures smoothly. For GCC portfolios, that dual mandate regional growth exposure paired with global monetary hedges makes gold and silver an enduring allocation rather than a tactical trade.