The Saudi Exchange has introduced a new Market Making Framework for its Exchange-Traded Funds (ETFs), a strategic move aimed at boosting liquidity and efficiency in the Saudi capital market. It has unveiled a newly developed ETF Market Making Framework, scheduled to go live in December 2025.

This initiative is part of the Kingdom’s broader Vision 2030, which seeks to transform the Saudi economy and develop its financial sector. The framework extends to equities, derivatives, and fixed-income markets, facilitating the presence of dedicated market makers who ensure continuous buy and sell orders for a listed security during trading hours.

This development complements the broader regulatory reforms introduced under the Capital Market Authority’s agenda to align Saudi Arabia’s capital markets with global best practices.

With the new framework, the Kingdom is creating an environment that supports greater product innovation, facilitates institutional participation, and advances its Vision 2030 objective of positioning Saudi Arabia as a leading investment hub.

The Saudi Arabian government targets to increase the industry’s AUM to 40% of the GDP by 2030, a significant jump from 26% in 2024.

ETF Market Growth Saga

The Kingdom’s ETF market has evolved steadily over the past 15 years:

- 2010 – Establishment of the ETF market with two listings: Yaqeen Saudi Equity ETF and Yaqeen Petrochemical ETF.

- 2019 – Approval of the first ETF backed by Sukuk assets, the Albilad Saudi Sovereign Sukuk ETF, expanding product diversity and catering to Shariah-compliant investors.

- 2022 – Listing of the first ETF with an international underlying asset and enhancement of creation/redemption mechanisms for ETFs through PTTP Phase 1.

- 2023 – Listing of the first technology-focused ETF, the AlBilad MSCI US Tech ETF.

- 2024 – Listing of two ETFs tracking Chinese equities: the Albilad CSOP MSCI Hong Kong China Equity ETF and the SAB Invest Hang Seng Hong Kong ETF, alongside the launch of the first ETF targeting SMEs.

- 2025 – SAB Invest introduced the first Saudi quant ETF, while Yaqeen the first MENA ESG ETF.

As per HSBC report, the number of ETFs rose to 12 in May 2025 from 7 in 2022 in Saudi Arabia, with AUM surging to around $2.03 billion from $410 million in 2022.

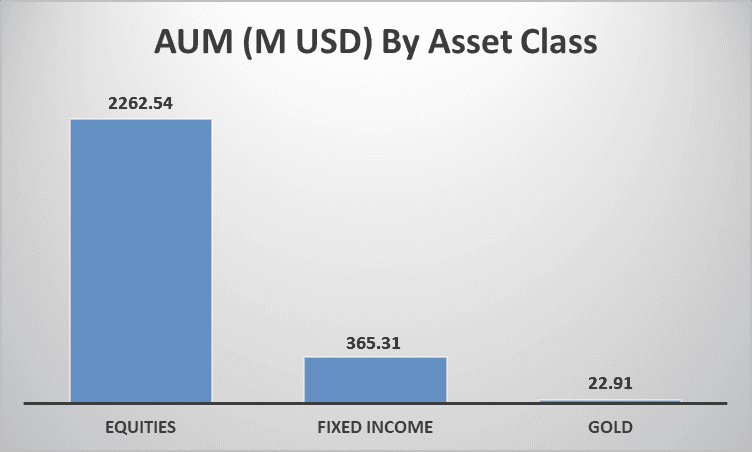

Total number of ETFs in Saudi Arabia (as of September 9, 2025) is provided below:

Key Components Of The Saudi Exchange’s Market Making Framework

- Market Maker Role: Contribute to market liquidity and price formation by continuously placing orders and adhering to obligations set by the Exchange. The Exchange uses a competitive, order-driven market making model.

- Performance Measurement: The framework uses specific parameters to measure a market maker’s performance, including the minimum bid/ask quantity (volume), the tightness of spreads (maximum spread), and their presence time (as a percentage in compliance).

- Market Maker Criteria: To be a market maker, a firm must be an Exchange Member and enter into a Market Making Agreement with the Exchange. The Exchange has the authority to accept or reject applications.

- Market Maker Monitoring: The Capital Market Authority oversees compliance with Market Conduct regulations. The Saudi Exchange’s Market Monitoring team continuously monitors adherence to the obligations and requirements on a daily basis.

Obligations and incentives for Market Makers

The obligations are categorized into three schemes: A, B, and C. The intensity of the obligations varies depending on factors such as the underlying asset’s liquidity and the agreement with the Fund Manager. For all three schemes, market makers are required to maintain a presence of 80% of the trading day and a minimum size of 50,000. The maximum spread obligations are as follows:

- Scheme A: 0.65%

- Scheme B: 1.00%

- Scheme C: 2.00%

Incentives: In exchange for meeting their obligations, market makers are eligible for a 100% discount on several commissions. This includes commissions for:

- Exchange trading (0.9bps)

- Edaa settlement & safekeeping (0.6bps)

- Muqassa Clearing (0.5bps)

- CMA trading (3bps)

Selection Process: The selection of an obligation group (A, B, or C) for a specific ETF is decided through a “Match Making process” between the ETF Fund Manager and the Market Maker. The chosen group must satisfy the Fund Manager’s objectives for liquidity and marketability while also being commercially viable for the Market Maker. The final agreement is submitted to the Saudi Exchange, and the group can be changed in the future if the Fund Manager requests it.

In a Nutshell

Overall, this development complements the broader regulatory reforms introduced under the Capital Market Authority’s agenda to align Saudi Arabia’s capital markets with global best practices.

The new framework is designed to enhance ETF market liquidity by formalizing the roles and obligations of market makers, while establishing a clear structure for engagement between market makers and fund managers. By doing so, it aims to ensure tighter bid-ask spreads, smoother trading, and more efficient price discovery for investors.