January’s data from Taiwan Semiconductor Manufacturing Company points firmly to the latter. The world’s largest contract chipmaker reported NT$401.3 billion ($12.7 billion) in revenue for the month, a 37% year-on-year increase and its fastest growth pace in months. The figure ran ahead of TSMC’s own ~30% revenue growth guidance for 2026, immediately reinforcing the view that global AI infrastructure spending remains resilient.

Momentum was visible on a sequential basis as well. January revenue rose nearly 20% month-on-month, a notable acceleration for a company operating at TSMC’s scale. Importantly, this growth was driven by sustained demand for advanced AI chips, with AI accelerators already contributing a high-teens share of total revenue.

Unlike sentiment-driven indicators, TSMC’s revenue reflects confirmed orders and production throughput. With capital expenditure expected to reach as much as $56 billion this year, roughly 25% higher than in 2025, January’s numbers offer one of the clearest quantitative signals yet that AI spending is still translating into real manufacturing demand.

What is actually driving TSMC’s January revenue surge?

TSMC’s momentum is driven by advanced chips for AI data centers. As the manufacturing partner for companies such as Nvidia, Apple, and AMD, the company sits at the most constrained and strategic point of the AI hardware supply chain.

Management has highlighted that AI-related chips have moved rapidly from experimental workloads to core revenue drivers. The combination of rising AI accelerator penetration and strong month-on-month growth suggests that demand is broadening rather than peaking.

How big is the AI infrastructure buildout behind the growth?

The clearest validation of this demand lies in capital allocation. TSMC has indicated plans to invest up to $56 billion in 2026, compared with roughly $45 billion in 2025. The majority of this spending is directed toward advanced manufacturing nodes required for AI and high-performance computing.

NVIDIA CEO Jensen Huang has described the current phase as a “once-in-a-generation infrastructure buildout,” a view echoed by supplier investment decisions. Hyperscalers such as Amazon and Meta Platforms continue to commit tens of billions of dollars annually to AI-ready data centers, sustaining demand for advanced chips.

How does AI chip demand translate into ETF-level exposure?

As AI infrastructure spending scales, its impact is increasingly visible at the index and ETF level, rather than through individual stocks alone. Semiconductor manufacturing now acts as a bottleneck layer in the AI value chain, and companies tied to this layer carry growing weight in global equity benchmarks.

For investors outside the U.S., this exposure is often accessed through ETFs. In the GCC, this linkage is already taking shape.

GCC US Tech and AI ETFs

Within the GCC, investor participation in the global AI and U.S. technology cycle is increasingly visible through a set of regionally listed ETFs offering distinct yet complementary exposures across artificial intelligence themes and U.S. equities.

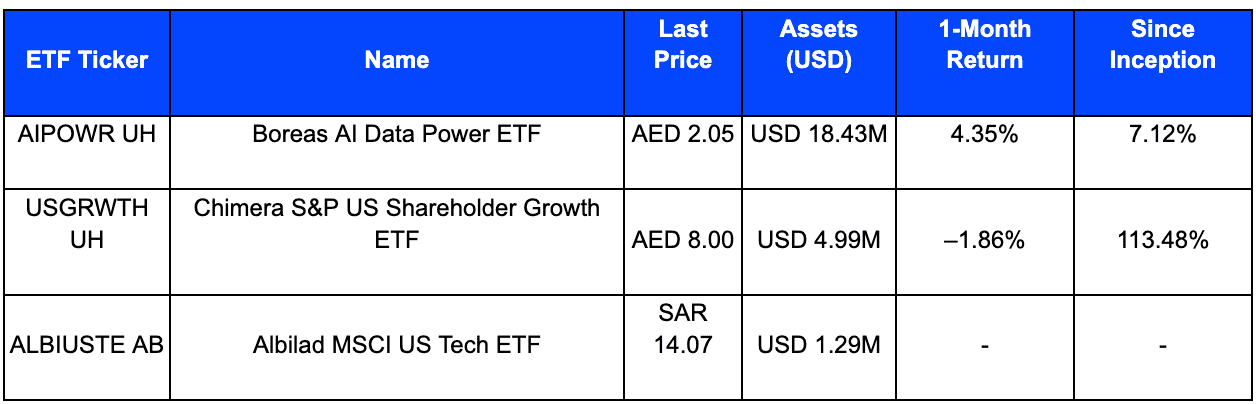

The Boreas AI Data Power ETF (AIPOWR UH), trading near AED 2.05, represents one of the region’s more thematic vehicles aligned with AI, data, and computing-power trends. The fund manages approximately USD 18.43 million in assets, making it the largest among this group. Recent performance data shows a 1-month return of +4.35% and a since-inception gain of +7.12%, highlighting early momentum consistent with AI-linked market dynamics.

Complementing this AI-focused exposure, the Chimera S&P US Shareholder Growth ETF (USGRWTH UH) trades near AED 8.00, with assets of roughly USD 4.99 million. The ETF has recorded a 1-month return of –1.86%, while delivering a since-inception return of +113.48%, reflecting its longer operating history and broader exposure to U.S. growth-oriented equities.

Similarly, the Albilad MSCI US Tech ETF (ALBIUSTE AB), priced around SAR 14.07, manages approximately USD 1.29 million in assets. The fund provides concentrated exposure to U.S. technology equities, a segment that typically exhibits higher volatility alongside periods of strong structural growth.

Taken together, these vehicles illustrate how GCC investors are accessing the same structural forces underpinning global AI demand, spanning AI infrastructure, demonstrating themes, diversified U.S. growth exposures, and technology-centric allocations.

Beyond thematic products, GCC-listed ETFs tracking U.S. and global indices carry indirect AI exposure through large technology constituents whose capital expenditure feeds directly into semiconductor demand. This linkage is increasingly visible in regional data: GCC ETF market monitor – 2025 annual review. The year of thematic ETFs

source: Lunate

Signals beneath the surface

Despite strong headline growth, investor caution has not disappeared. Concerns around capital intensity, valuation, and historical technology cycles remain part of the discussion. However, several data points suggest the current phase is grounded in real demand: AI accelerators already represent a material share of revenue, capital expenditure continues to rise, and monthly revenue momentum remains strong.

What does TSMC’s revenue surge mean for investors next?

TSMC’s 37% January revenue growth is best viewed as a signal, not a spike. It confirms that AI infrastructure spending is flowing through manufacturing, earnings, and capital investment decisions. For global investors and particularly those in the GCC, accessing markets through ETFsthe takeaway is the takeaway. AI exposure today is less about chasing headlines and more about understanding where infrastructure demand sits within indices and portfolios.

As long as AI spending continues at scale, the semiconductor backbone supporting it will remain a central driver of market and ETF performance.