The global market for exchange-traded funds has expanded to roughly USD 18.8 trillion in assets and now comprises more than 14,000 products worldwide. The scale is vast enough that professional allocators, from private banks to sovereign institutions, must navigate an increasingly crowded landscape. Despite this proliferation, the evaluation process continues to revolve around a core set of principles involving strategy, methodology, liquidity, costs, tracking behaviour, scale, governance, structure, risk, sustainability, and operational support.

For investors in the GCC, these considerations are layered with additional structural and regulatory concerns, including the distinction between UCITS and U.S.-domiciled funds, the implications of withholding tax, Shariah compliance, and the practicalities of trading on ADX, DFM, and Tadawul.

What follows is a structured examination of how institutional ETF analysis unfolds in practice and why these factors determine portfolio construction from Abu Dhabi to Riyadh.

1-Strategy, Exposure and the Role of the ETF

Every evaluation begins with clarity about the investment purpose. An ETF must provide a specific type of exposure, whether broad-market beta, a factor tilt such as value or low volatility, a thematic focus such as renewable energy or artificial intelligence, a sector allocation, fixed income duration management, or access to commodities.

The central question is always the same: which role will the fund play inside a multi-asset portfolio?

An ETF may function as a core holding such as global equities or aggregate bonds, or it may serve as a satellite exposure that supplements an existing allocation, such as emerging-market small caps. It can be used for tactical adjustments, for example through short-duration bonds during periods of rate uncertainty. Some strategies are designed for hedging through currency-hedged equity baskets, while others are intended to enhance yield through covered-call structures where mandates allow such techniques.

Investors who often carry a home-market bias through allocations to MENA equities and regional alternatives, the relevance and differentiation of global ETF exposure matter significantly more than in other markets. The objective is rarely to duplicate what the portfolio already owns, but instead to introduce new risk factors, geographies, or sectors with precision

2-Index Quality and Methodology

Since an ETF is essentially the physical expression of its benchmark, the credibility and construction of the index become central to the analysis. Reputable providers such as MSCI, FTSE Russell, S&P Dow Jones, and Solactive are usually favoured because their methodologies are transparent, consistent, and widely stress-tested.

Indices differ substantially in how they are built. The main variables include weighting schemes, the frequency of rebalancing, the presence of liquidity or ESG screens, and any constraints that affect concentration. These rules determine turnover and, by extension, trading costs. A thematic index with narrow constituents and frequent reconstitutions, for example, often produces higher slippage and more variable tracking.

The key question is whether the index captures the exposure it claims to represent. An ETF marketed as an artificial-intelligence strategy should genuinely allocate to companies with material AI-driven revenue, not simply to large technology firms with incidental involvement.

3-Liquidity in Both the Secondary and Primary Markets

Liquidity determines whether investors can move capital efficiently and with minimal market impact. The conventional focus on average daily volume or headline bid–ask spreads tells only part of the story. Equally important is the presence and responsiveness of market makers and authorised participants who facilitate creation and redemption activity.

Liquidity exists at three levels. The first is the liquidity of the underlying securities, which ultimately defines the elasticity of the ETF. The second concerns activity on the ETF’s primary listing venue, whether that is London, New York, or Frankfurt. The third involves liquidity on regional exchanges when the fund is cross-listed on ADX, DFM or Tadawul. These Gulf listings are growing in number but typically show lower on-exchange volumes, which is why institutional trades are often routed through the primary market instead.

The objective is not simply to find an ETF that trades frequently but to ensure that blocks of USD 10 to 100 million can be executed without distorting prices. A liquid underlying basket with strong AP support can offer superior execution even when the ETF itself appears lightly traded. ,

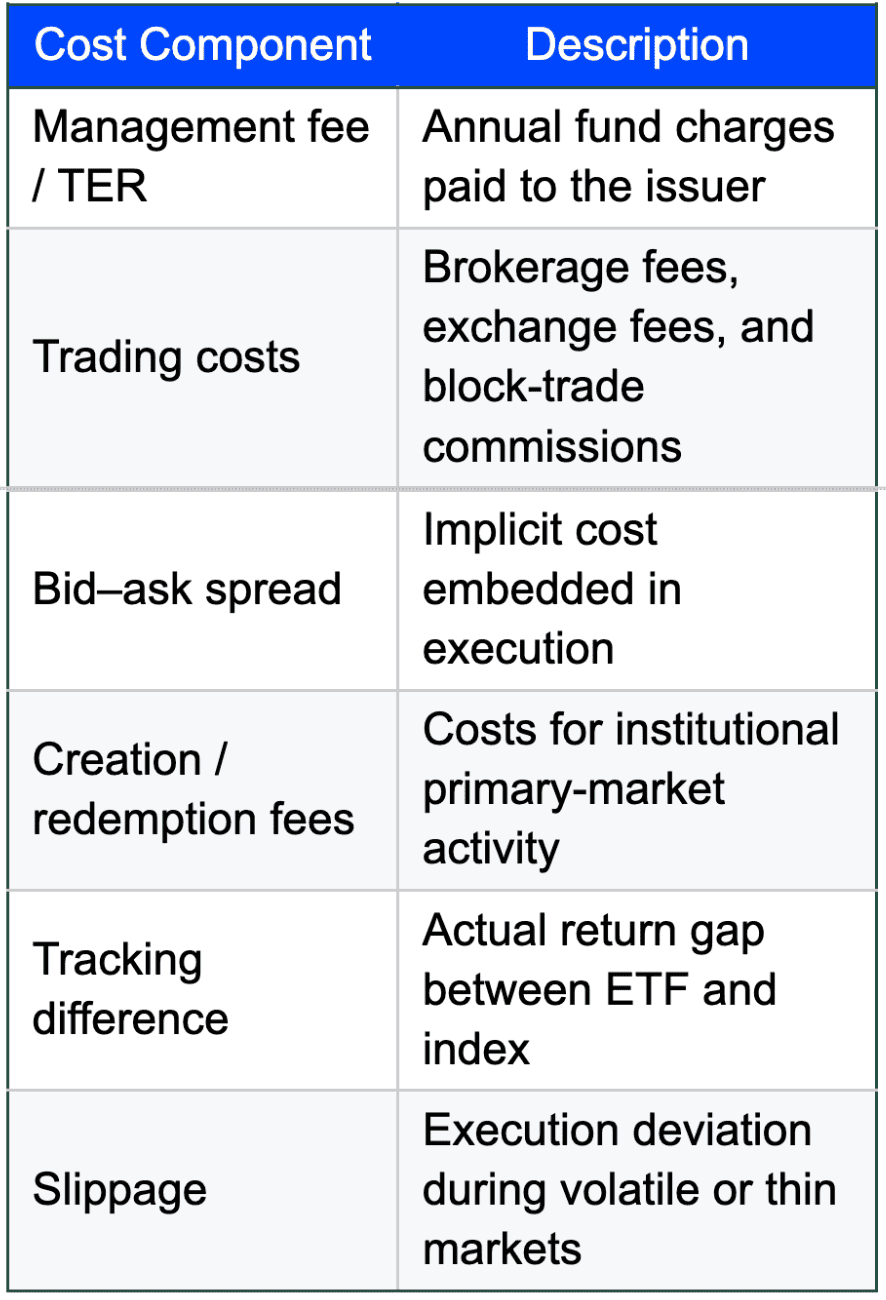

4-Explicit and Implicit Costs

The Total Expense Ratio is rarely the decisive factor on its own. Professionals examine the entire cost structure, which includes both explicit expenses and implicit frictions. The explicit costs include brokerage commissions and creation or redemption fees for large orders. The implicit components include bid-ask spreads, the degree of slippage during execution, and the fund’s realised tracking difference relative to its index.

The table below summarizes the typical components of ownership cost:

5-Tracking Quality

Tracking behavior reveals how effectively a fund delivers the exposure it promises. Analysts study tracking error, which measures the variability of the ETF’s return relative to its index, and they evaluate the replication approach.

Full physical replication tends to suit large, liquid benchmarks. Optimised sampling is more efficient for broad universes where owning every constituent is impractical. Synthetic replication is used when markets are difficult to access, although some regional mandates restrict its use.

Dividend treatment, tax drag, cash balances, and rebalancing efficiency all influence tracking. During market stress, high-quality ETFs maintain consistent behaviour, whereas weaker structures may see their deviations widen noticeably.

6-Fund Size, Scalability and Long-Term Viability

Asset size remains a reliable indicator of operational stability. ETFs that have achieved sufficient scale tend to operate more efficiently and face lower closure risk. This is particularly relevant for thematic strategies that require larger asset bases to manage high turnover and for fixed income strategies that must trade bonds at institutional scale.

Institutional teams monitor how assets are growing, how diversified the investor base is, and whether the fund has established a stable history. A young fund may be promising but is often monitored for a period before being adopted.

7-Issuer Reputation and Operational Strength

The ability of the ETF provider to manage liquidity, maintain tight spreads, and operate complex strategies is a central differentiator. Institutions often prefer issuers with a proven track record in similar asset classes, robust risk-management frameworks, and direct capital-markets teams who can coordinate large trades with authorised participants.

In the GCC, the presence of regional support teams, Arabic-language resources, and familiarity with local custodians and brokerages can play a meaningful role. Strong operational backing often translates into better execution quality and more reliable tracking.

8-Regulatory and Structural Considerations

Structural features influence tax outcomes, diversification rules, reporting requirements, and investor eligibility.

Domicile is particularly important.

Ireland-domiciled UCITS funds benefit from European regulatory protections and treaty-based tax advantages. U.S.-domiciled ETFs offer exceptional scale and liquidity but are often tax-inefficient for Gulf investors.

Fund structure also matters. UCITS imposes diversification thresholds and strict oversight. U.S. 40-Act funds operate differently and may provide more flexibility but with different tax implications.

Shariah compliance introduces another analytical layer. Investors examine which board oversees screening, how purification is calculated, and whether the methodology aligns with institutional religious requirements.

Cross-listing rules on regional exchanges further influence settlement processes, operational convenience, and access for local institutions.

9-Performance and Risk Characteristics

Performance analysis extends well beyond headline returns. Institutions compare funds with their benchmarks and their peer groups across multiple horizons. Factor exposures are closely evaluated to ensure there are no unintended biases. Concentration levels, volatility patterns, drawdowns, and correlations with existing holdings all inform how the ETF interacts with the broader portfolio.

In fixed income, duration, credit quality, and yield-curve positioning are scrutinized. Currency behavior is also relevant, especially for UAE investors who may weigh the advantages of USD-hedged versus unhedged exposures.

10-Sustainability and ESG Factors

Where sustainability is part of the mandate, investors review the clarity and rigour of ESG methodologies. The differences between exclusion-based and best-in-class screening approaches can be material. Impact metrics such as carbon-intensity scores are examined alongside the alignment of the ETF’s methodology with the internal ESG frameworks used by family offices, sovereign wealth funds, and pension plans.

Although ESG adoption in the GCC is uneven, interest is rising among institutions managing international portfolios.

11-Distribution, Partnership and Ongoing Support

Operational relationships increasingly influence ETF selection. High-quality issuers provide analytical tools, portfolio-construction support, trading guidance, and research coverage. Training, local events, and responsive capital-markets desks contribute to smoother implementation and better execution.

Reliable partnership reduces friction and ensures that the ETF continues to function effectively long after initial allocation.

Final Thoughts

ETF evaluation has evolved into a multi-dimensional process that spans strategy design, index construction, liquidity, cost structure, tracking behaviour, scale, regulatory architecture, risk characteristics, sustainability, and operational robustness. In the GCC, the analysis is further shaped by Shariah requirements, tax considerations, domicile preferences, and the realities of local-market liquidity.

While many ETFs appear similar at first glance, careful examination reveals meaningful differences. The most suitable products are those that combine rigorous methodology, efficient liquidity, coherent structure, and strong operational support, allowing them to integrate cleanly into portfolios built for long-term institutional objectives across the Gulf.