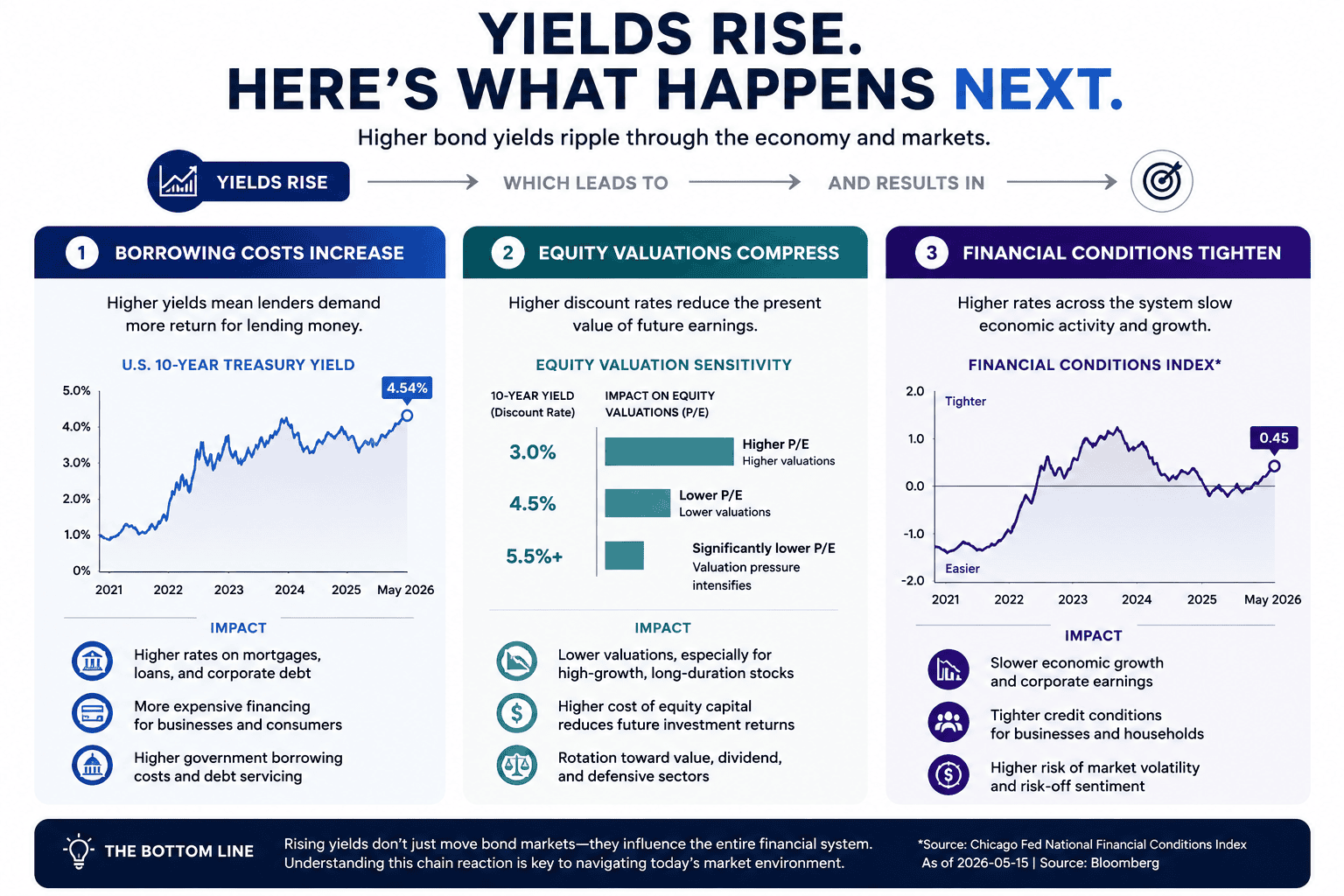

U.S. Treasury yields surged this week, with the 10-year Treasury yield climbing above 4.5% and the 30-year Treasury yield briefly crossing the 5% mark, levels not seen consistently since the 2023 tightening cycle. Equities, meanwhile, moved sharply lower as investors reassessed the outlook for interest rates, inflation, and monetary policy under incoming Fed Chair Kevin Warsh.

The reaction underscores a growing reality in global markets where investors may want rate cuts, but the bond market is no longer convinced they can arrive without consequences.

As of 2026-05-15, Nasdaq futures were down more than 1%, while the S&P 500 also retreated as rising yields pressured high-growth technology shares. Reuters reported that traders are increasingly positioning for a “higher-for-longer” rate environment amid persistent inflation concerns and renewed geopolitical risks tied to energy markets.

Why Rising Yields Matter So Much

Treasury yields sit at the center of global financial markets.

The impact is particularly severe for long-duration growth sectors such as technology and artificial intelligence (AI), where investors are paying today for earnings expected years into the future. That dynamic explains why technology-heavy indices weakened as Treasury yields climbed. The higher the discount rate, the lower the present value of future cash flows, a critical issue for richly valued AI and semiconductor stocks that have led markets over the past two years. The market is also confronting a deeper concern: whether the new Fed leadership can realistically ease policy without reigniting inflation.

Enter Kevin Warsh

A former Fed governor and long-time critic of expansive central-bank balance sheets, Warsh has repeatedly argued for a more disciplined monetary framework and a reduced Federal Reserve footprint in markets.

That matters because the Fed still holds roughly $6.7 trillion in assets even after years of quantitative tightening (QT), the process of shrinking its balance sheet. Markets increasingly believe further balance-sheet reduction could keep upward pressure on long-term Treasury yields, especially as U.S. fiscal deficits remain elevated.

In effect, investors fear the Fed may be entering a difficult balancing act:

- cut rates too quickly and inflation could rebound,

- stay restrictive for too long and growth could slow materially.

The bond market appears to be signalling that inflation credibility now matters more than short-term equity support.

The GCC Investor Angle

Across the GCC, equity markets showed mixed reactions as rising U.S. Treasury yields tightened global financial conditions and pressured investor sentiment.

Saudi Arabia’s Tadawul All Share Index (TASI) fell 0.6% to 11,187.7 in April, while Abu Dhabi’s FTSE ADX General Index rebounded 2.7% after suffering its steepest monthly decline in six years in March. Dubai’s DFM General Index climbed 6.1% following a sharp 16.4% selloff the previous month, supported by renewed buying in financial and real estate names.

Kuwait’s All Share Index advanced 5.3%, making it one of the region’s strongest-performing markets during the period, while Qatar’s QE20 Index gained 2.9% and the broader Qatar All Share Index rose 3.1%. More recent trading sessions, however, pointed to renewed caution, with Dubai, Abu Dhabi, and Kuwait edging lower as higher global yields continued to weigh on regional risk appetite.

ETFs to Watch in This Environment

Several ETF categories are likely to remain central to the “higher-for-longer” debate:

The contrast is becoming increasingly stark:

- AI and growth ETFs continue to benefit from structural demand trends,

- while bond-market volatility is forcing investors to reassess valuations and portfolio risk.

The Bigger Message From Markets

The market story is no longer simply about whether the Fed cuts rates.

It is about whether investors trust inflation to remain contained if it does.

That distinction matters because Treasury yields are now driving global asset pricing more aggressively than central-bank guidance itself. Equities may still benefit from AI optimism and resilient earnings, but the bond market is reminding investors that liquidity is no longer free.

And for the new Fed chair, that may be the hardest message of all.