Oil, risk premia, and why Gulf markets often wobble then re-price fast

Every serious U.S.-Iran escalation over the past decade has followed a familiar market script. An overnight jump in Brent, a wobble in global equities, and sharp often exaggerated moves in Gulf markets at the open.

Yet history also shows that unless Gulf oil or shipping lanes are directly hit, GCC equities and the ETFs that track them tend to stabilize quickly, sometimes outperforming broader emerging markets within days.

For ETF investors, the nuance matters. The GCC ETF universe is small, concentrated, and liquidity-sensitive, meaning geopolitical shocks can distort prices and flows far more than fundamentals would justify.

The three transmission channels that matter most

1. Oil: the fastest and loudest signal

Oil remains the dominant shock absorber and amplifier for GCC ETFs.

- Fear alone moves prices. Even rhetoric around the Strait of Hormuz has historically added several dollars to Brent, while credible disruption scenarios model double-digit dollar spikes.

- Index math matters. Saudi and Kuwait equity benchmarks and the ETFs tracking them carry heavy energy weightings. A $10 move in Brent mechanically upgrades earnings expectations for producers and fiscal balances, often offsetting initial equity risk-off.

The result is a paradox Gulf investors know well: oil up sharply, equities briefly down then higher, once markets conclude supply is constrained but Gulf exports are still flowing.

2. Risk sentiment vs. the “energy windfall” trade

U.S. strikes typically trigger a global risk-off move: stronger USD, lower U.S. Treasury yields, weaker EM beta. GCC ETFs feel this immediately through foreign flows.

But recent history including the June 2025 U.S. strikes on Iranian nuclear assets shows a rapid pivot. Gulf markets opened lower, then reversed intraday as investors faded worst-case scenarios and re-priced higher oil revenues and reduced regional uncertainty.

For ETFs, this often shows up as:

- Brief NAV discounts widening at the open

- Fast normalization once oil stabilizes and local buyers step in

- Higher realized volatility, even when weekly returns end flat or positive

3. Perceived threat to Gulf infrastructure

This is the real regime-changer.

Markets have consistently distinguished between:

- U.S.–Iran confrontation elsewhere, which Gulf markets can “look through”; and

- Direct attacks on GCC bases or energy assets, which permanently re-rate risk premia.

Analyst reaction to Iran’s strike on Qatar’s Al Udeid base in 2025 was telling, it was framed as breaking the region’s perceived insulation from high-intensity conflict. In ETF terms, that translates into structural underperformance versus EM, not just a knee-jerk sell-off.

Chimera sharia UAE, Chimera sharia KSA, albilad msci (growth), msci (equity)

Why ETFs amplify the move in the Gulf

A thin, concentrated ecosystem

On-shore GCC ETFs remain tiny relative to underlying markets, roughly sub-USD 1 billion in local ETF AUM against more than USD 2.5 trillion in GCC equity market capitalization (as of mid-2025, based on exchange disclosures and industry surveys).

How Regional Equity ETFs Are Affected

Heightened regional risk and global macro volatility tend to transmit into GCC markets through a small set of highly visible, locally listed equity ETFs, where flows and sentiment can move prices faster than underlying fundamentals.

- Chimera S&P UAE Shariah ETF

As a Shariah-screened proxy for UAE equities, the ETF is typically sensitive to risk sentiment and foreign positioning. During periods of geopolitical stress, defensive sector tilts within the Shariah universe can help cushion downside, but thinner liquidity means price moves can still be amplified. - Chimera S&P KSA Shariah ETF

This ETF reflects Saudi equity exposure through a Shariah-compliant lens. In risk-off episodes, it often sees short-term volatility driven by global EM flows, even when domestic fundamentals remain stable, as international investors adjust regional exposure quickly. - Albilad MSCI Saudi Growth ETF

Growth-oriented Saudi equities tend to be more sensitive to global risk repricing. Rising geopolitical uncertainty or shifts in U.S. rates can disproportionately affect valuation-sensitive names within the growth segment, leading to sharper ETF price swings. - Albilad MSCI Saudi Equity ETF

As a broader Saudi market tracker, this ETF acts as a core barometer for foreign and institutional sentiment toward the Kingdom. It is often used for tactical positioning, making it susceptible to inflows and outflows during periods of heightened uncertainty. - Chimera FTSE ADX 15 ETF

Tracking the largest and most liquid Abu Dhabi-listed stocks, this ETF concentrates exposure in financials and large-cap names. While this can provide relative stability, concentration risk means that shifts in sentiment toward a handful of constituents can quickly affect performance.

Scenario map: what a U.S. strike means for GCC ETFs

Scenario 1: Limited, one-off U.S. strike (contained conflict)

This is the market’s base case.

- Likely pattern: Gap-down at the open → intraday recovery

- ETF impact: Temporary discounts, small outflows, quick stabilization

- Drivers: Oil up, Hormuz open, “overhang resolved” narrative

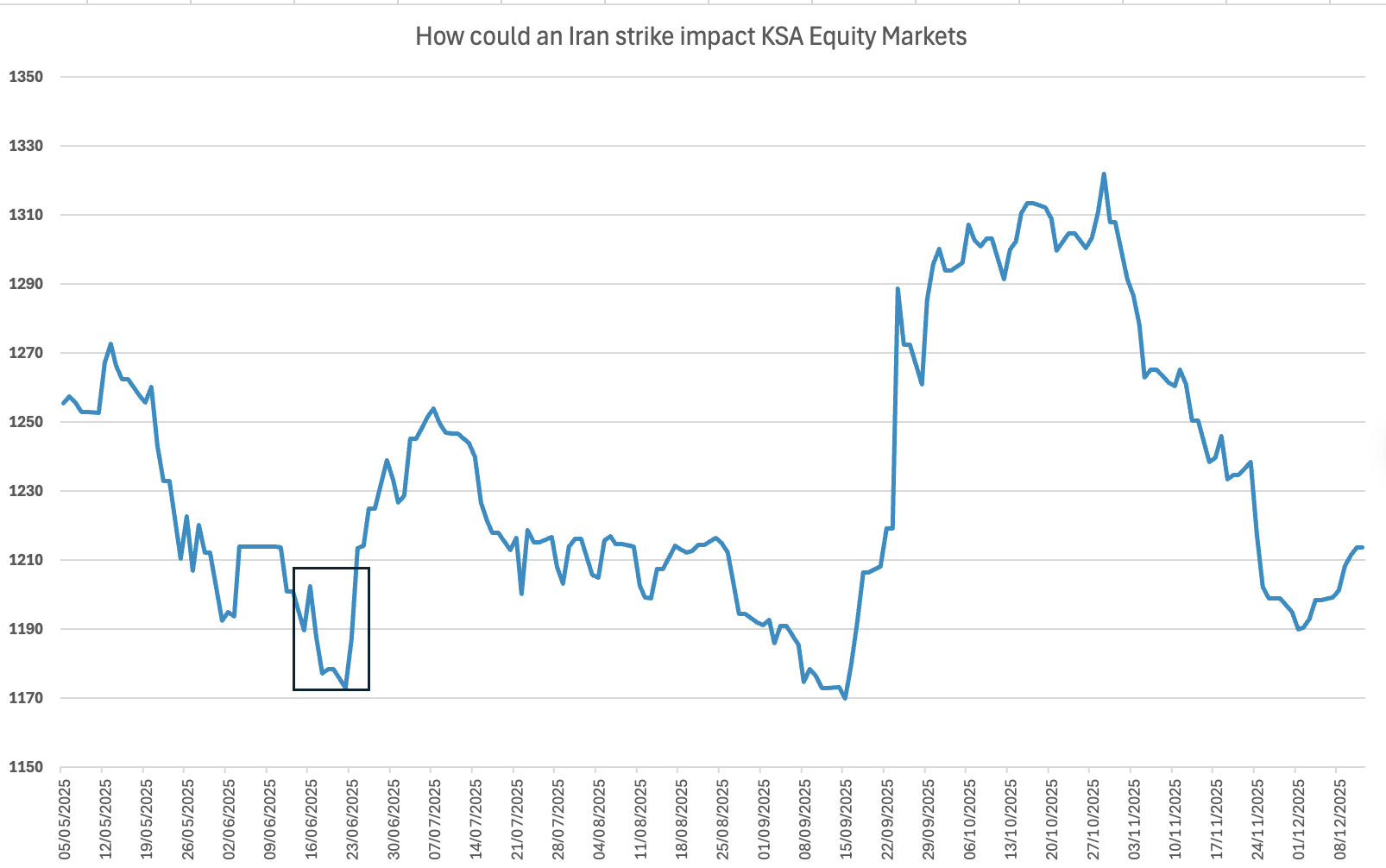

Saudi and UAE-heavy ETFs often recover within days, mirroring what was observed on 22 June 2025 when most Gulf benchmarks closed higher despite escalation.

Scenario 2: Prolonged tit-for-tat, but managed risk

Missiles, cyber activity, proxy attacks but no direct Gulf hits.

- Oil: Elevated but choppy; can even fall once worst fears fade

- ETFs: Trade as a hybrid, defensive oil exporter plus high-beta EM

- Flows: Episodic outflows on headlines, followed by selective re-entry

This environment tends to reward energy-tilted Saudi ETFs over more diversified UAE or Qatar products, though volatility stays high.

Scenario 3: Serious disruption in the Strait of Hormuz

The market’s tail risk.

- Oil: Sharp spike; LNG markets dislocated

- ETFs: Pulled in opposite directions energy earnings surge, non-oil sectors suffer

- Outcome: Extreme dispersion between Saudi-heavy ETFs and more diversified GCC funds

Even here, pipeline capacity in Saudi Arabia and the UAE partially caps duration, but not initial shock.

Cross-asset feedback loops investors often miss

- USD and rates: A stronger dollar and lower U.S. yields typically tighten EM financial conditions, dragging on passive flows into GCC equity ETFs.

- Relative safe-haven effect: Improved external balances mean some allocators treat Saudi and GCC assets as relative EM havens, supporting demand for products like Janus Henderson GCC Sovereign USD Bond Core UCITS ETF during equity stress.

- Internal sector rotation: Banks, telecoms and domestically focused names often outperform cyclicals, muting index-level drawdowns even when headlines are alarming.

Bottom line for ETF investors

A U.S. strike on Iran almost always produces headline-driven volatility in GCC ETFs, but history suggests that oil flow continuity and Gulf insulation matter far more than the strike itself. For now, the dominant pattern remains sharp but often short-lived dislocations, amplified by thin ETF liquidity rather than collapsing fundamentals.