Beijing is publicly framing its latest rare-earth export controls as “retaliatory, not escalatory” and urging Washington back to the table, just as the White House threatens 100% tariffs and fresh export controls on critical software. Markets moved sharply before diplomacy could catch up. China-linked equity ETFs such as KWEB, as well as Gulf-listed funds like Chimera, Albilad, and SABB, all felt the impact as investors recalibrated exposure to technology, trade, and supply-chain themes.

China’s Ministry of Commerce (MOFCOM) released a detailed Q&A defending its rare-earths measures as legal, licensed, and narrowly tailored while accusing the United States of applying double standards.

The message between the lines was simple: keep talking, avoid a spiral. For GCC and UAE investors, this policy volley matters because it ripples directly into regional and cross-listed ETFs through tariff headlines, export-control uncertainty, and supply-chain disruptions in strategic sectors such as semiconductors and electric vehicles.

The Policy Clash in Brief

China’s position: MOFCOM insists that its export controls on medium and heavy rare earths are legal and license-based rather than outright bans. Beijing says it notified partners in advance and expects the supply-chain impact to be limited. The ministry also points to recent U.S. restrictions such as new Entity List additions, an expansion of the “Affiliates Rule,” and new port fees as the real escalation.

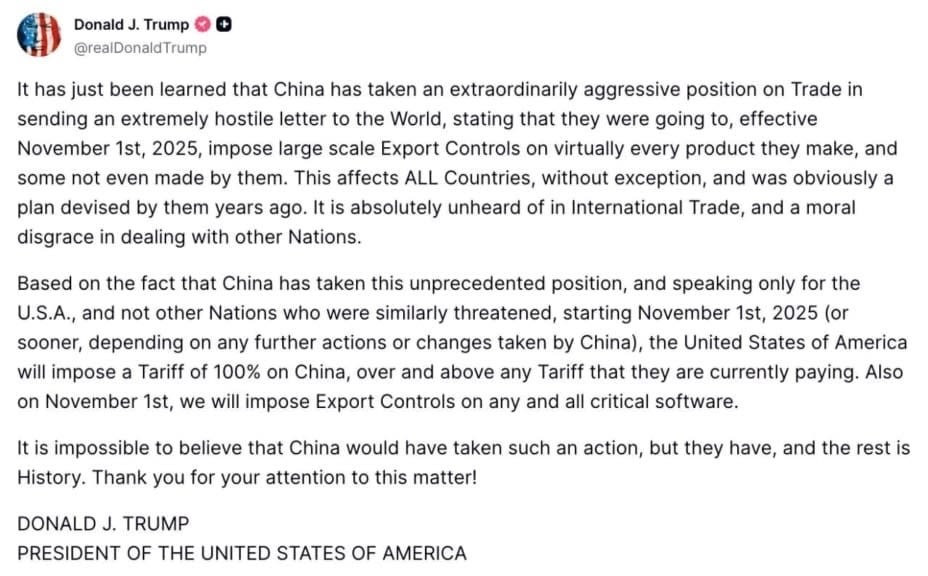

Washington’s stance: The White House has announced plans for 100% tariffs and fresh software export controls, describing them as a response to Beijing’s measures. Global media coverage has interpreted the move as the end of a fragile truce ahead of a potential leaders’ meeting.

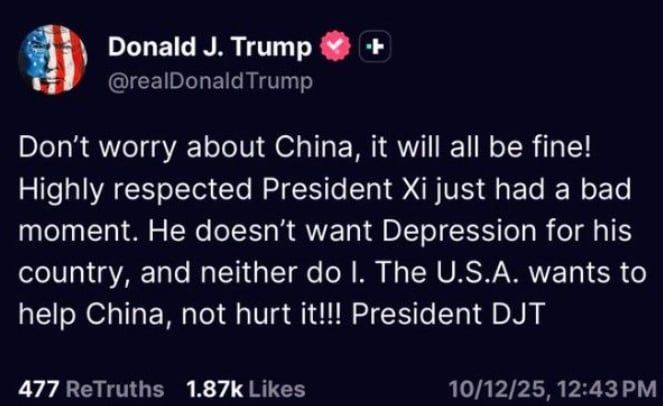

Reality check on intent: Beijing emphasizes that its actions are retaliatory rather than offensive, signaling that they could be reversed if talks resume. Even Trump posted a reassuring message that “it will be fine”. Analysts, however, see a broader pressure campaign unfolding on both sides, with rare earths emerging as a bargaining chip ahead of future negotiations.

ETF Markets React

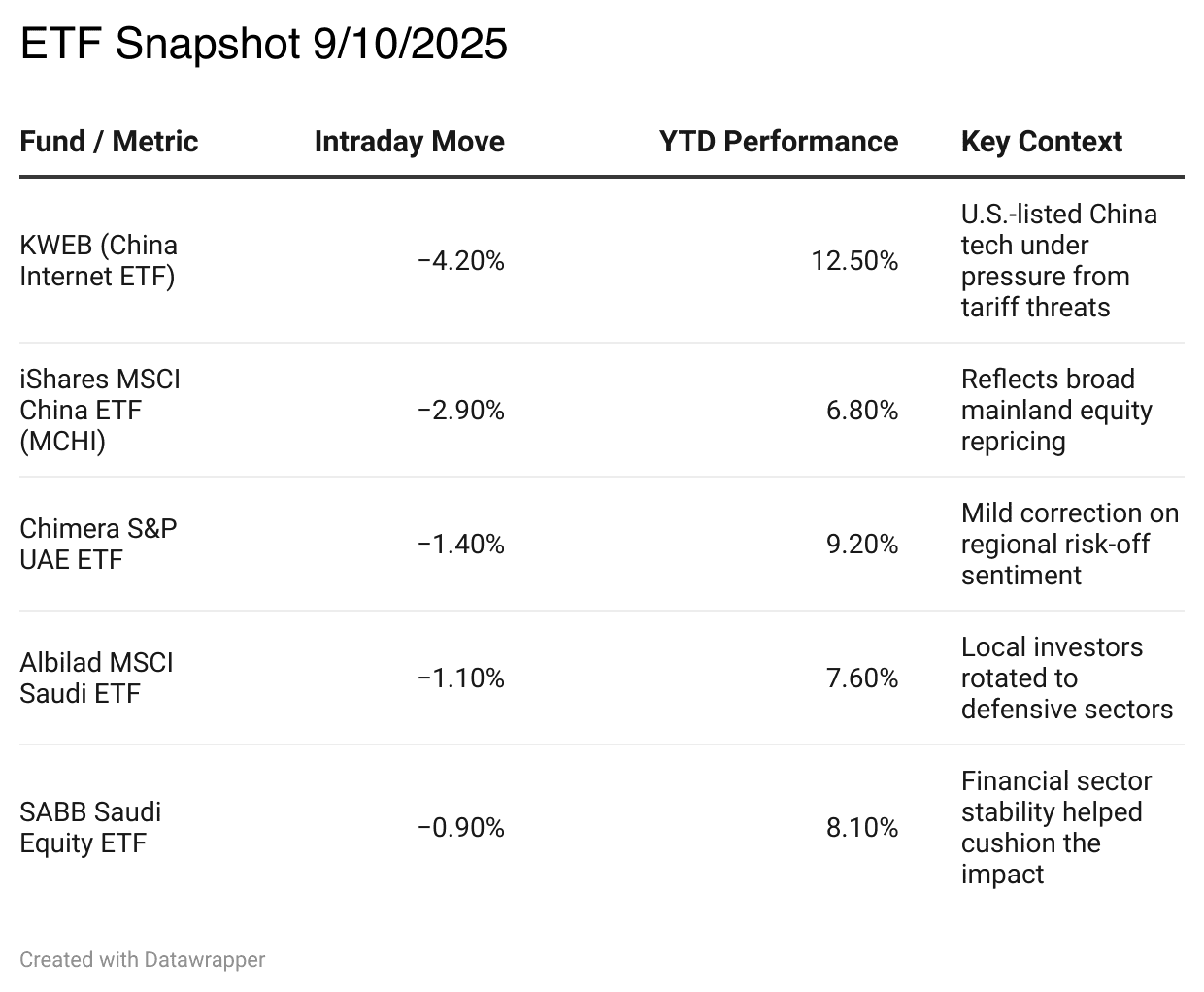

China-related ETFs bore the brunt of the volatility. The KraneShares CSI China Internet ETF (KWEB), a bellwether for U.S.-listed Chinese tech, fell more than 4% in intraday trading before stabilizing as investors weighed the risk of deeper trade restrictions. Broader China equity funds, including MSCI China and Asia-Pacific ETFs, registered declines of 2% to 3% over the same period.

Gulf-listed vehicles with regional or global equity exposure also felt the tremor. The Chimera S&P UAE ETF, Albilad MSCI Saudi ETF, and SABB Saudi Equity ETF each posted small but noticeable declines as risk sentiment turned defensive. Traders in Abu Dhabi and Riyadh reported thinner liquidity and wider spreads in China-focused feeder funds, suggesting that institutional desks were trimming cross-border risk rather than exiting positions outright.

Despite the volatility, many of these funds remain positive year to date. KWEB, which had benefited from optimism around China’s post-reopening stimulus and AI-linked growth, still shows a double-digit gain for the year. The GCC equity ETFs mentioned above have also maintained healthy year-to-date returns supported by robust regional earnings and steady oil prices.

Figures represent approximate moves based on available market data and public exchange snapshots.

The relatively small moves in GCC-listed ETFs compared to the sharp swings in China-linked funds illustrate a key point: regional markets remain tethered to global risk sentiment but are buffered by local fundamentals and liquidity support.

How the China–U.S. Line Feeds the ETF Tape

Tariffs and export controls have become macro shock triggers for global equity investors. The latest U.S.–China exchange re-priced growth assumptions, supply-chain stability, and trade flow forecasts, tightening financial conditions at the margin and pushing volatility indices higher.

At the same time, China’s rare-earth licensing mechanism functions as a strategic lever rather than an outright embargo. It allows flexibility in how strictly the controls are applied, depending on diplomatic temperature. That flexibility keeps risk premia elevated across sectors such as semiconductors, electric vehicles, and industrial technology. These are the same industries that underpin large thematic ETFs like KWEB and MSCI China.

Markets have read the subtext clearly. Beijing’s statements emphasize dialogue and restraint, while Washington’s tone points to deterrence and resolve. This combination leaves two potential paths: renewed negotiations that could calm markets or further policy missteps that might extend the downturn. Investors across New York, Riyadh, and Dubai are watching closely, aware that volatility will persist as long as communication between the two capitals remains strained.

Market Watchpoints and Data Considerations

The data surrounding last week’s market reaction remain fragmented. Different venues recorded varying intraday lows for Chinese equities, highlighting liquidity imbalances during periods of stress. For clearer signals, NAV-based ETF data offer a smoother read of performance.

ETF flow numbers should be viewed as preliminary since dashboard data are often revised after settlement. Single-day redemptions or inflows rarely tell the full story.

On the policy front, Beijing’s rare-earth licensing system appears flexible enough to permit continued civil and commercial use, while Washington’s tariff implementation schedule and “critical software” definitions are still in flux. Any official rule text or postponement could immediately reshape market sentiment, making policy sequencing the variable that investors must watch most closely.

Market Lessons and Investor Implications

The market correction was driven primarily by macro shocks rather than any structural weakness in ETF mechanisms. Tariff threats and export controls combined with a fragile investor backdrop to trigger a sharp, sentiment-driven selloff.

Major ETFs such as KWEB and MCHI in the United States, along with GCC-listed funds like Chimera, Albilad, and SABB, demonstrated resilience through orderly trading and limited outflows. Their positive year-to-date performance underscores that investors continue to see value in both Chinese recovery themes and Gulf-region growth.

The broader outlook remains one of negotiation risk, not systemic failure. Beijing’s insistence that its actions are retaliatory rather than escalatory leaves open the possibility of renewed dialogue. Washington’s tariff rhetoric, meanwhile, suggests the potential for further friction before any easing. Until clarity emerges, headlines rather than fundamentals are likely to continue steering ETF prices and investor sentiment.