Market structure changes rarely make headlines, but they often matter more than they seem, particularly for ETF investors. The Dubai Financial Market (DFM) has introduced a revised tick size regime effective April 6, 2026, quietly lowering the cost of trading across listed securities, including ETFs.

At its core, the reform introduces greater granularity in price increments, particularly in the mid-cap range where trading activity and many ETF underlying holdings are concentrated.

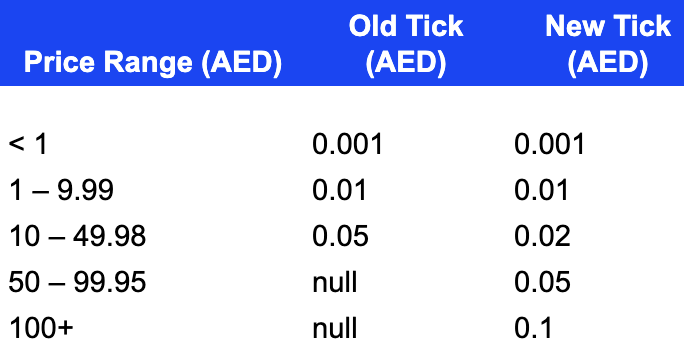

Tick Size Structure: Before vs After

The key shift is in the AED 10-50 band, where tick size drops by 60%, from 0.05 to 0.02 directly compressing the minimum possible spread.

What This Means for Trading Costs

A useful way to estimate minimum trading cost is:

(Tick Size ÷ Price ÷ 2)

This approximates half the bid-ask spread in a one-tick market.

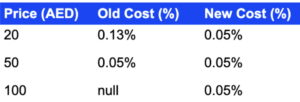

Before vs After: Cost Comparison

Example (AED 20):

- Before: 0.05 ÷ 20 ÷ 2 = 0.125%

- Now: 0.02 ÷ 20 ÷ 2 = 0.05%

This represents a 60% reduction in minimum trading cost for stocks in that range.

Why This Matters for ETF Investors

For ETF investors, this is a direct and positive development.

ETFs rely heavily on secondary market liquidity, where investors trade units on exchange. Lower tick sizes translate into:

- Tighter bid-ask spreads

- Lower execution costs

- Reduced slippage when entering or exiting positions

Because ETFs derive liquidity from their underlying securities, improvements at the stock level feed directly into ETF pricing efficiency. In other words, cheaper trading in underlying equities helps tighten ETF spreads.

What stands out in the new framework is the normalisation of trading costs. Whether a security trades at AED 20 or AED 100, minimum costs now converge around ~0.05%. This suggests deliberate calibration by DFM to standardize trading efficiency across price tiers rather than applying a blanket reduction.

The Bigger Picture

This move brings DFM closer to global best practices, where dynamic tick sizing is used to balance liquidity provision with pricing precision. While smaller ticks reduce costs, they must remain large enough to incentivise market makers, a balance DFM appears to be targeting.

For investors, particularly those active in ETFs, the takeaway is straightforward: lower ticks mean lower hidden costs. These changes may not be immediately visible like brokerage fees, but they compound over time improving execution quality and overall portfolio efficiency.

In that sense, DFM’s update is less about changing how markets look, and more about improving how they function, quietly reducing friction, one basis point at a time.