Tensions between the Federal Reserve and the White House escalated sharply over the weekend, triggering notable volatility across global financial markets. Fed Chair Jerome Powell revealed that the U.S. Department of Justice had threatened him with a potential criminal indictment linked to his congressional testimony on the $2.5 billion renovation of the Fed’s headquarters in Washington, D.C. Powell described the investigation and related subpoenas as a “pretext” aimed at pressuring the central bank to cut interest rates, further intensifying the long-running dispute with President Donald Trump’s administration.

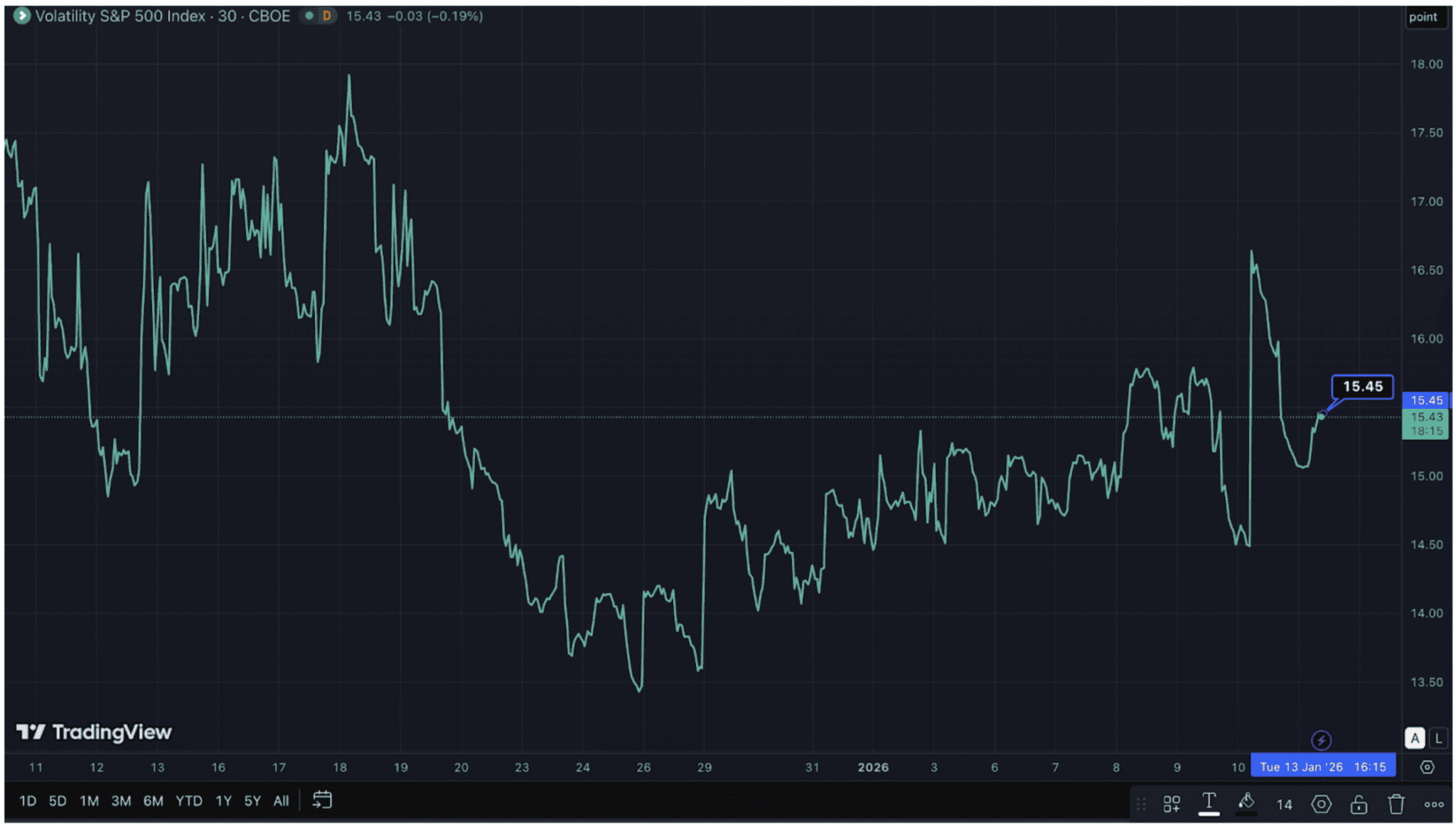

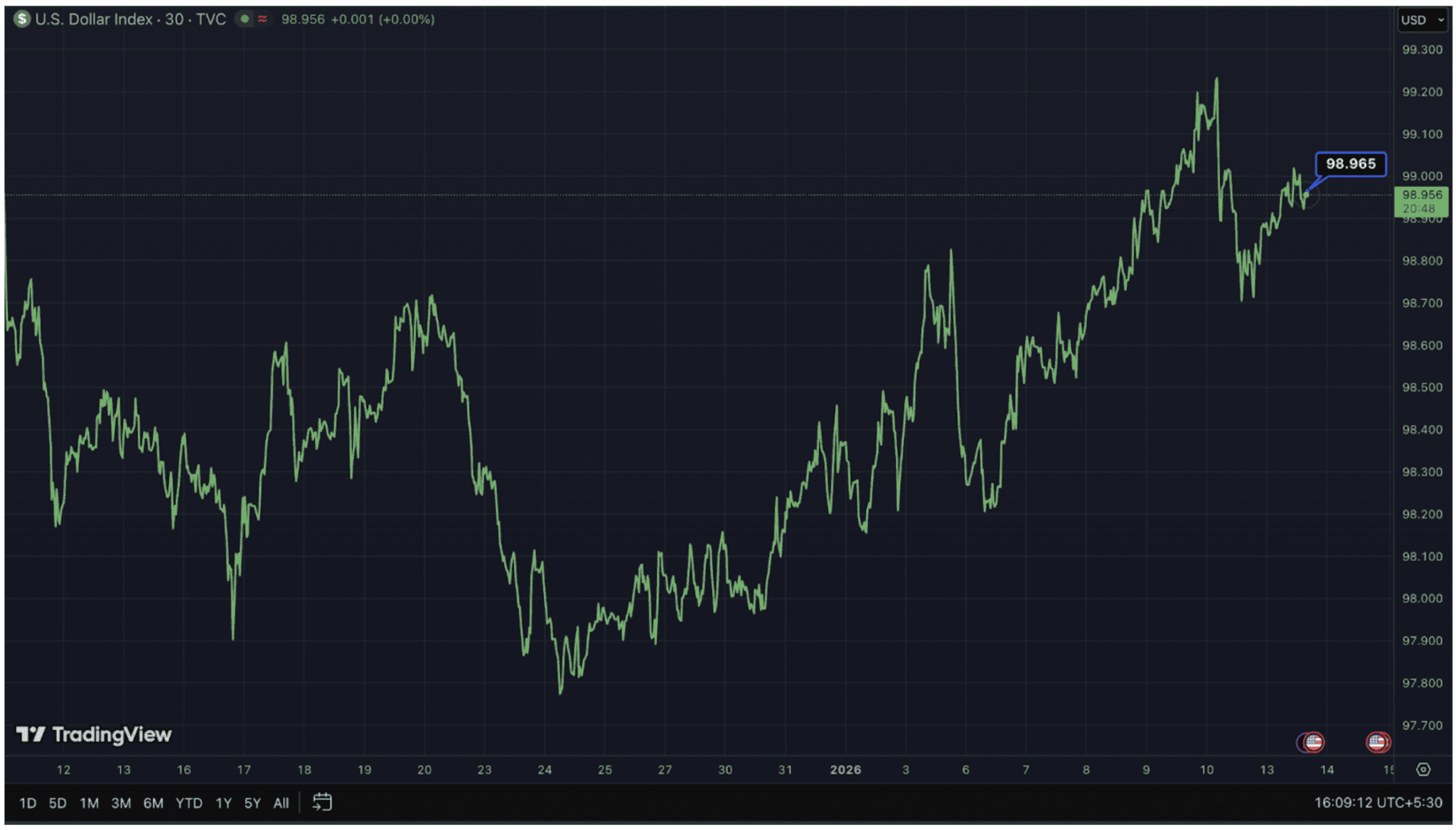

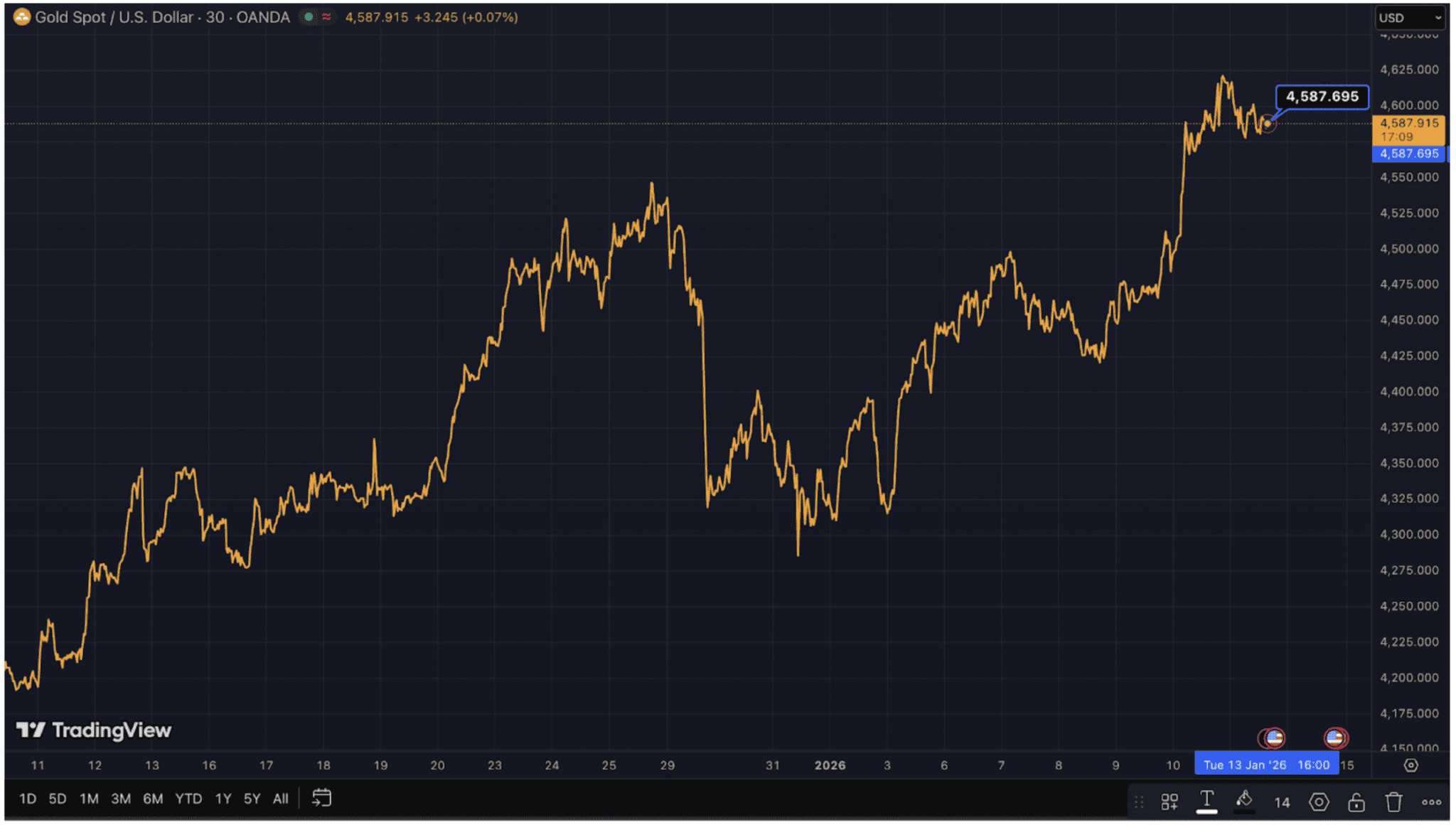

The reaction was immediate. S&P 500 and Nasdaq futures fell by more than 0.6% ahead of the U.S. market open, the S&P volatility index (VIX) jumped sharply, and gold surged to a record $4,600 an ounce as traders sought safe havens amid uncertainty. At the same time, the U.S. dollar weakened broadly, with the U.S. Dollar Index (DXY) retreating from recent highs, sliding about 0.2% to around USD 98.95 on Monday, January 12, 2026, as concerns over Fed independence and potential policy shifts weighed on demand for the greenback against major currencies.

Volatility Index (VIX)

What Sparked the Crisis?

The DOJ investigation, approved by a Trump-appointed U.S. attorney, focuses on whether Powell misled Congress regarding cost overruns and project details tied to the Fed’s headquarters renovation. Powell has maintained that higher costs reflected inflation, tariffs, and unforeseen construction challenges, arguing that the legal action is politically motivated and intended to influence monetary policy, particularly interest-rate decisions.

Impact on the U.S. Dollar

The U.S. dollar weakened following the escalation, as investors reassessed confidence in U.S. monetary policy and the Federal Reserve’s independence. Rising expectations of interest-rate cuts, combined with heightened political risk, reduced the dollar’s appeal as a safe-haven asset and prompted flows toward alternatives such as gold and U.S. Treasuries. As a result, demand for dollar-denominated assets softened, leaving the greenback vulnerable to further downside if policy uncertainty persists.

A weaker dollar has important implications for Gulf Cooperation Council markets, as most regional currencies are pegged to the USD and therefore move in tandem. Dollar softness can increase import costs and place mild upward pressure on inflation, but it can also improve the competitiveness of non-oil exports and services. Transmission is relatively direct, with GCC policy rates typically tracking the Federal Reserve; regional central banks mirrored Fed rate cuts in 2025, and markets currently expect a further 75 basis points of easing in 2026, supporting credit growth and activity in non-oil sectors.

U.S. Dollar Index (DXY)

Implications for GCC ETFs

For GCC-focused ETFs, the environment presents a mixed but increasingly differentiated outlook.

Gold and Safe-Haven ETFs

Gold and commodity-linked ETFs are likely to remain well supported by safe-haven demand. In this context, the Albilad Gold ETF (9405) stands out as a key regional beneficiary, increasing by 2.37% over the last two days. As a Tadawul-listed, Shariah-compliant ETF backed by physical gold, it provides GCC investors with direct exposure to rising gold prices amid heightened political risk, dollar weakness, and falling real yields.

| ETF | Recent 2-Day % Return |

| Albilad Gold ETF (9405) | 2.37% |

Gold Spot Rate

Equity and Rate-Sensitive ETFs

By contrast, equity ETFs with significant exposure to banks, financial services, and other rate-sensitive sectors may face near-term headwinds. Financial stocks are particularly sensitive to changes in interest-rate expectations and risk premiums, and global policy uncertainty can place additional pressure on valuations. ETFs heavily weighted toward these sectors could therefore experience elevated volatility relative to broader market benchmarks.

Fixed Income and Currency-Hedged Strategies

At the same time, currency-hedged and fixed-income ETFs may attract rising interest as investors seek to manage USD volatility while maintaining exposure to yield-generating assets. Expectations of future rate cuts could further support demand for such strategies, especially among investors looking to diversify away from pure dollar risk.

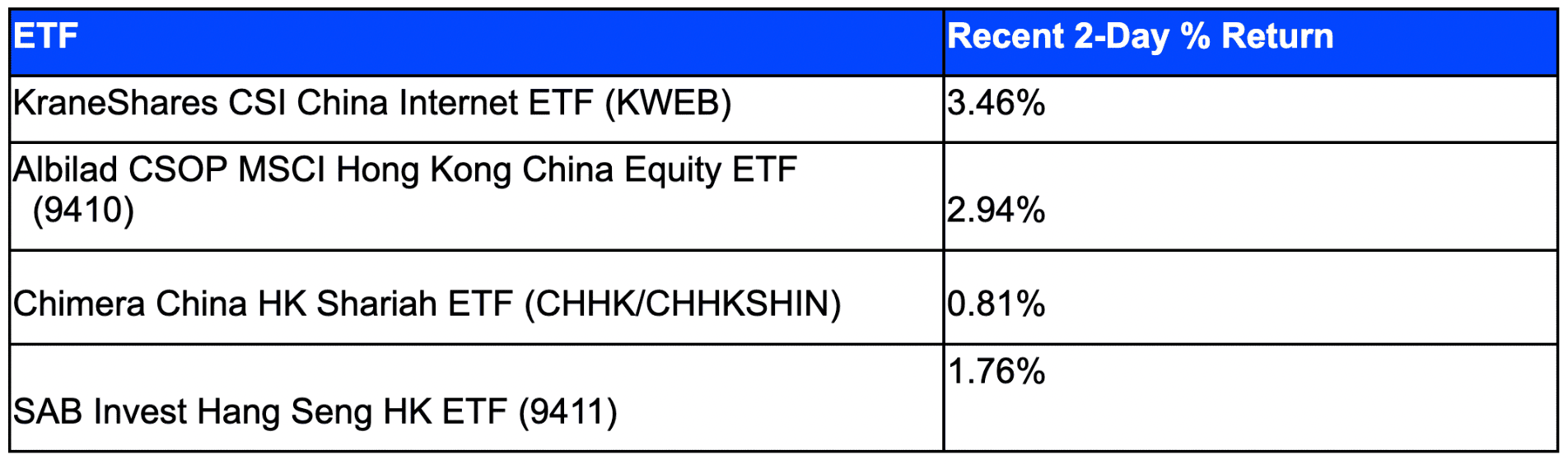

Emerging Markets Angle, China ETFs Listed in the GCC

A softer U.S. dollar and declining U.S. rate expectations are historically supportive for emerging-market assets, particularly China. Improved liquidity conditions, lower USD funding stress, and portfolio rebalancing away from U.S. assets can drive renewed inflows into China-focused equities.

Below are the four China-focused ETFs commonly tracked by GCC investors, along with their recent cumulative 2-day performance: (as of 11th Jan to 13th Jan)

The strong short-term performance of China-linked ETFs, particularly internet and Hong Kong-exposed strategies, highlights how EM assets may benefit from USD softness and shifting global risk sentiment.

Positioning and Outlook

In practical terms, the current backdrop suggests that GCC ETF investors may benefit from a more balanced and flexible allocation approach. Commodity- and precious-metal-linked ETFs are likely to remain supported as safe-haven demand persists, while sector-specific equity ETFs, especially those tied to financials, may continue to experience elevated volatility. Currency-diversified and hedged strategies could gain prominence as shifts in dollar strength reshape relative returns across global asset classes.

Overall, the Fed-Powell conflict underscores how political risk and monetary policy uncertainty in the U.S. can have far-reaching effects beyond domestic markets. For GCC ETF investors, this episode underscores the importance of balancing defensive exposures with growth-oriented assets, while closely monitoring developments in U.S. policy credibility, dollar dynamics, and global risk sentiment as markets continue to adjust.