A striking cross-asset message is emerging early in 2026: the commodity complex is no longer moving in isolated pockets. Gold and silver are printing fresh records, copper is pushing to new highs, and European carbon prices are back at multi-month peaks, all at the same time.

The common thread is not a single supply shock but a macro cocktail; cooling inflation readings, rising conviction that the U.S. Federal Reserve is nearing (or entering) a rate-cut cycle, and a market that is increasingly willing to pay up for scarce assets tied to security, electrification, and decarbonization.

That convergence matters for GCC investors because the region increasingly accesses these themes through listed ETFs, often in local wrappers or through cross-listed exposures. And because GCC currencies are largely USD-pegged, the USD rate path can feed directly into local asset pricing and flows, even when the underlying story is global.

Precious metals: the “rates + risk” trade is back on the table

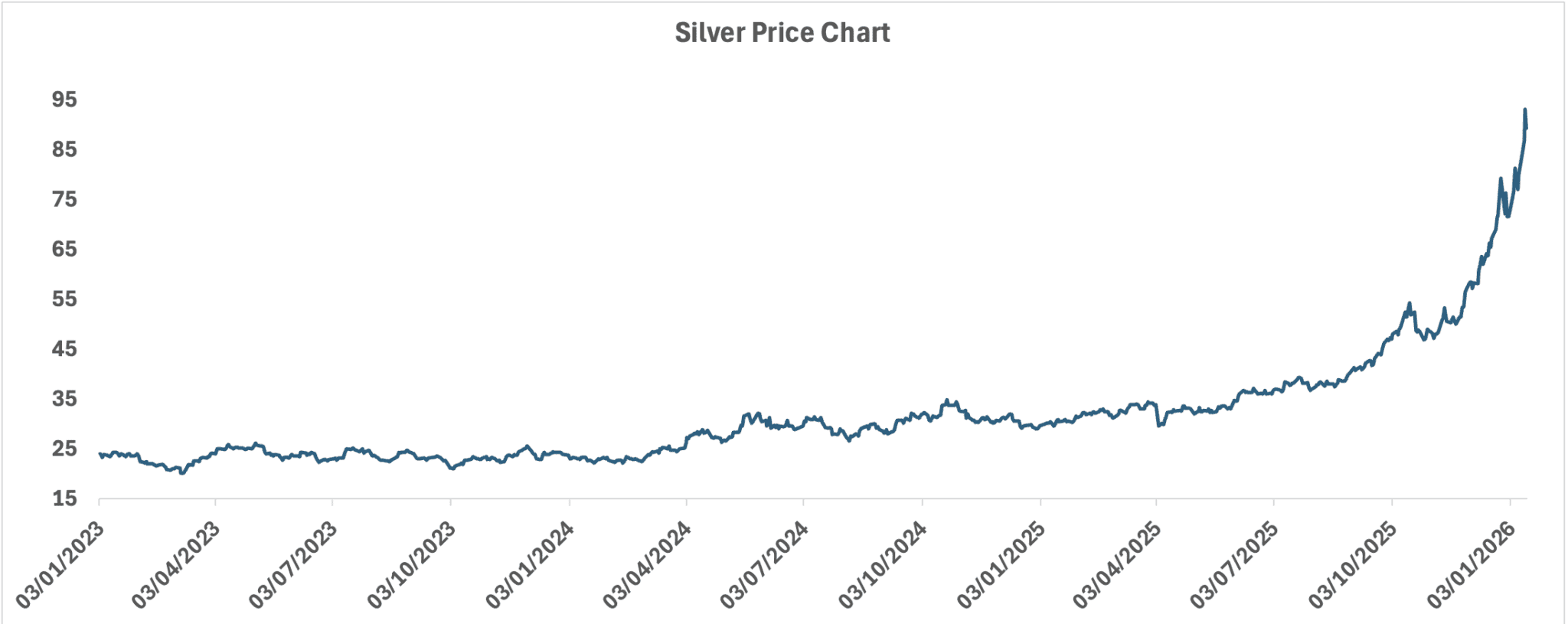

The most dramatic move has been in precious metals. Spot gold hit a record around $4,639/oz on 2026-01-14, while spot silver pushed above $90/oz a major psychological level that signals the rally has shifted from “fundamental improvement” to “momentum + positioning” territory.

What changed?

In the immediate term, softer-than-expected U.S. inflation data helped pull forward expectations of Fed easing. Reuters reported that CPI undershot forecasts, and markets repriced the probability and timing of rate cuts. Lower expected policy rates generally support non-yielding assets like gold because they reduce the opportunity cost of holding them.

But rates are only half the story. Gold’s rally also reflects persistent geopolitical uncertainty and a deeper institutional bid. Reuters noted continued strong central bank demand, with China adding to gold reserves for a 14th consecutive month, and highlighted very large inflows into gold-backed ETFs during 2025. In other words, gold is being treated less like a tactical hedge and more like a strategic reserve asset especially in a world where politics and policy credibility are seen as increasingly fragile

Silver

Silver’s surge is similar but more volatile. Silver behaves like a hybrid partly monetary metal and partly industrial input. That combination can turn bullish quickly when growth expectations stabilize and investors crowd into high beta inflation hedges. The move above $90/oz underscores that risk appetite is now chasing the metal’s convexity, not just its defensive qualities.

Beyond its monetary role, silver’s rally is increasingly underwritten by technology: it is a critical input in solar photovoltaics, power electronics, and advanced semiconductors, turning the metal into a quiet beneficiary of both energy transition capex and AI-era hardware demand.

This is exactly why gold ETFs remain structural winners in the region, easy to trade, familiar, and increasingly used as a conviction allocation. Silver is likely to see growing interest too, but investors should expect significantly higher drawdowns than gold in any risk-off reversal.

Copper: electrification meets tight supply and a market that wants scarcity

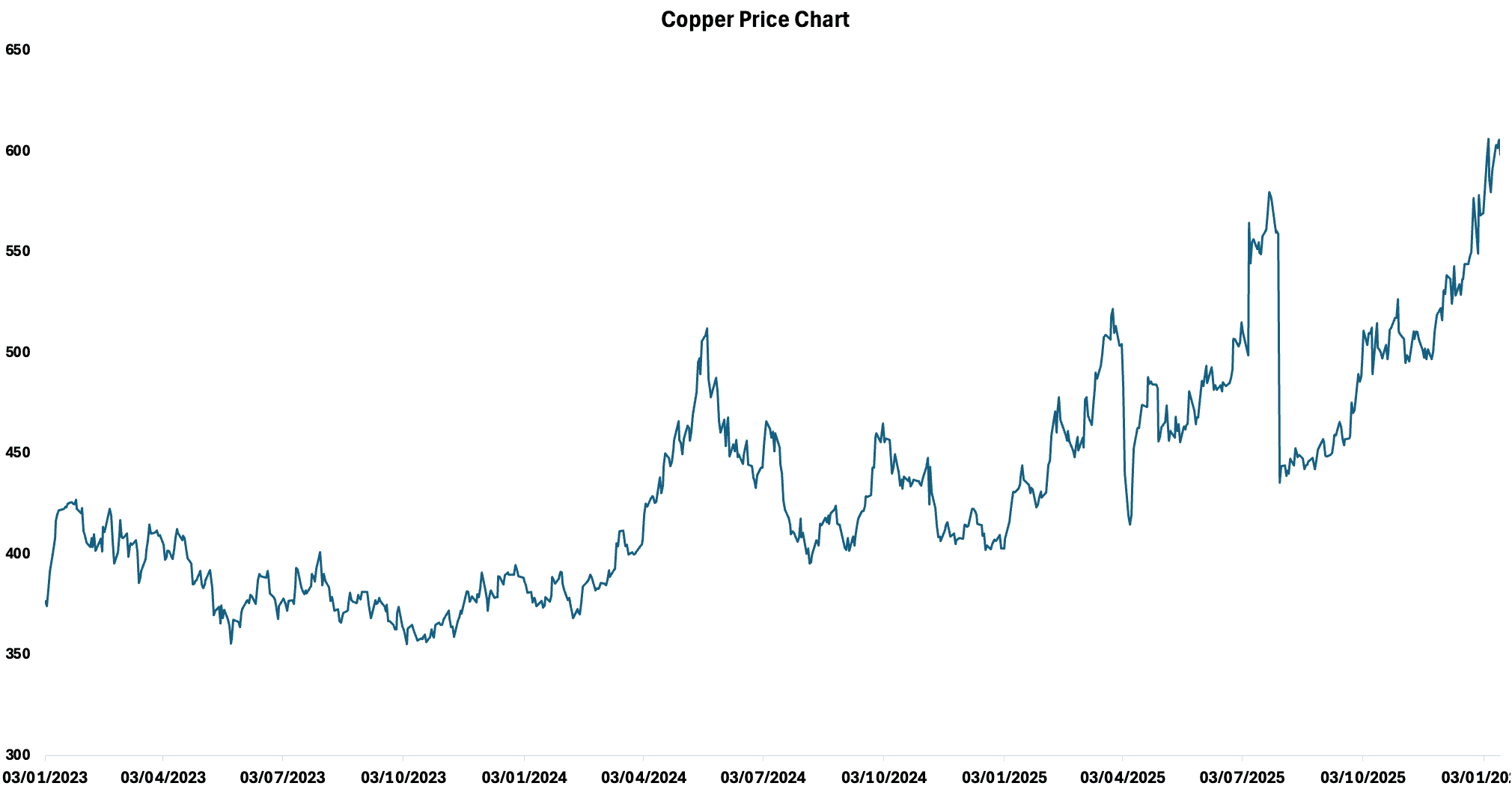

If gold is the trust trade, copper is the \infrastructure trade. Prices have surged to new records, with industry reporting copper moving beyond $13,000/ton on the LME in early January. Trading Economics also shows copper near $5.99/lb as of 2026-01-14, reflecting the sharp run-up into the new year.

The bull case has three pillars:

- Structural demand: electrification, grid upgrades, EV supply chains, and data-center buildouts are copper-intensive. The market increasingly prices copper as a strategic input, not just a cyclical industrial metal.

- Copper’s scarcity premium is being reinforced by technology itself: AI data centres, cloud infrastructure, and high-voltage grid upgrades are far more copper-intensive than previous digital cycles, embedding structural demand into what used to be a purely industrial metal.

- Supply discipline and bottlenecks: permitting delays, declining ore grades, and project lead times keep supply response sluggish. Even when prices surge, mines can’t instantly add output.

- Positioning and inventories: market structure is amplifying moves. Argus flagged the role of inventory shifts and the intensity of the bull run, while Mining.com noted the explosive start to 2026 even as it cautioned that underlying demand, especially from China could soften.

S&P Global highlighted that copper may be overextended, pointing to diverging views between Western specs and China positioning, with shorts on the Shanghai Futures Exchange at notably wide levels.

Translation: copper is being pulled upward by global thematic capital, but it still lives and dies by real-economy demand, particularly from China.

Copper’s “new highs” narrative is already pushing investors toward theme access vehicles whether through miners, diversified materials ETFs, or broader energy-transition baskets. But copper is also where mean reversion can be violent if China demand disappoints or if financial positioning unwinds.

Carbon: pricing policy risk and monetizing decarbonization

The surprise for many investors is carbon: it’s no longer an obscure European policy instrument. It’s increasingly a tradeable macro input, and early 2026 is reinforcing that. European carbon permits have moved back toward fresh highs, with Trading Economics showing EU carbon permits around €90.74 as of 2026-01-13.

S&P Global reported EU Allowances around €86.57/mtCO₂e in mid-December after contract rollover dynamics and supportive auction mechanics.

Why is carbon rising?

- Policy tightening and scope expansion: The EU’s carbon market continues to evolve, and new rules are widening the pool of obligated emissions. For example, maritime compliance costs in the EU ETS phase in to 100% from 2026, increasing the “real economy” demand for allowances tied to shipping activity.

- Trade policy reinforcement: The EU’s carbon border adjustment mechanism (CBAM) is coming into force, reinforcing the idea that carbon has become embedded in global trade economics for carbon-intensive goods.

- Financial participation: As carbon becomes a recognized asset class, financial positioning and contract roll effects can amplify price moves.

For ETF investors, the cleanest single-ticker proxy remains carbon-focused ETFs such as KRBN, which provides exposure to carbon allowance futures. KRBN last traded around 131 AED

Carbon is a compelling “new macro” theme for regional investors precisely because it is policy-anchored and diversifying as its drivers are not identical to equities, rates, or oil.

The global setup: one macro regime, three expressions

Put the pieces together and you can see the regime forming:

- Gold is pricing policy credibility + geopolitical anxiety + easier money.

- Silver is pricing the same, but with leverage and industrial beta.

- Copper is pricing electrification scarcity + capital cycle constraints, with a watchful eye on China demand.

- Carbon is pricing tightening decarbonisation policy and increasingly, trade and industrial compliance.

The connective tissue is that markets are becoming more willing to own “hard constraints” finite metals, finite carbon budgets, especially when the path of interest rates looks less restrictive.

What GCC investors should watch next

- U.S. rates and the USD path: With GCC currencies largely pegged to the dollar, the Fed’s direction tends to transmit quickly into local financial conditions. A sustained rate-cut narrative is generally supportive for precious metals and often constructive for risk-linked commodities.

- China demand signals: Copper bulls can coexist with China weakness for a while until they can’t. Watch industrial data, property stabilisation signals, and China futures positioning for early warnings of a sentiment shift.

- Carbon policy headlines: Carbon is a policy market first. Changes to auction schedules, market linking (EU-UK), compliance scope, or CBAM enforcement can reprice the asset quickly.

- ETF implementation costs: For investors accessing these themes via ETFs, the key operational variables are tracking, liquidity, and especially for futures-based products like carbon roll mechanics.

GCC-Accessible ETFs Linked to the Commodity Rally

| Theme | ETF | Exchange | Ticker | Exposure Type |

| Gold | Albilad Gold ETF | Tadawul | 9405.SR | Physical gold |

| Silver | iShares Silver Trust | NYSE | SLV | Physical silver |

| Copper | iShares Copper and Metals Mining ETF | NYSE | ICOP | Copper and Metals Miners |

| Carbon | KraneShares Global Carbon ETF | ADX | KRBN | Carbon allowances (futures) |

Bottom line

Early 2026 is delivering a rare alignment: defensive metals, industrial metals, and decarbonization assets are all making new highs together.

That doesn’t guarantee the rally is linear; if anything, it raises the odds of sharp corrections but it does signal a broader shift in global investor preference toward assets that hedge policy risk, monetise structural transitions, and benefit when the cost of money starts to fall.