Hedge funds were once viewed as the opposite of ETFs. One promised discretion, complexity and alpha; the other offered transparent, low-cost market exposure. That distinction is becoming less clean. New Bloomberg Intelligence data shows hedge funds have tripled their ETF exposure over the past three years to roughly $300 billion, equal to about 9% of reported 13F assets.

That matters because hedge funds are not buying ETFs the way retail investors do. For them, ETFs are trading tools, hedges, liquidity sleeves, macro instruments and sometimes short positions. The result is a more complex relationship: hedge funds increasingly rely on ETFs, even as ETFs continue to compete with hedge funds for investor capital.

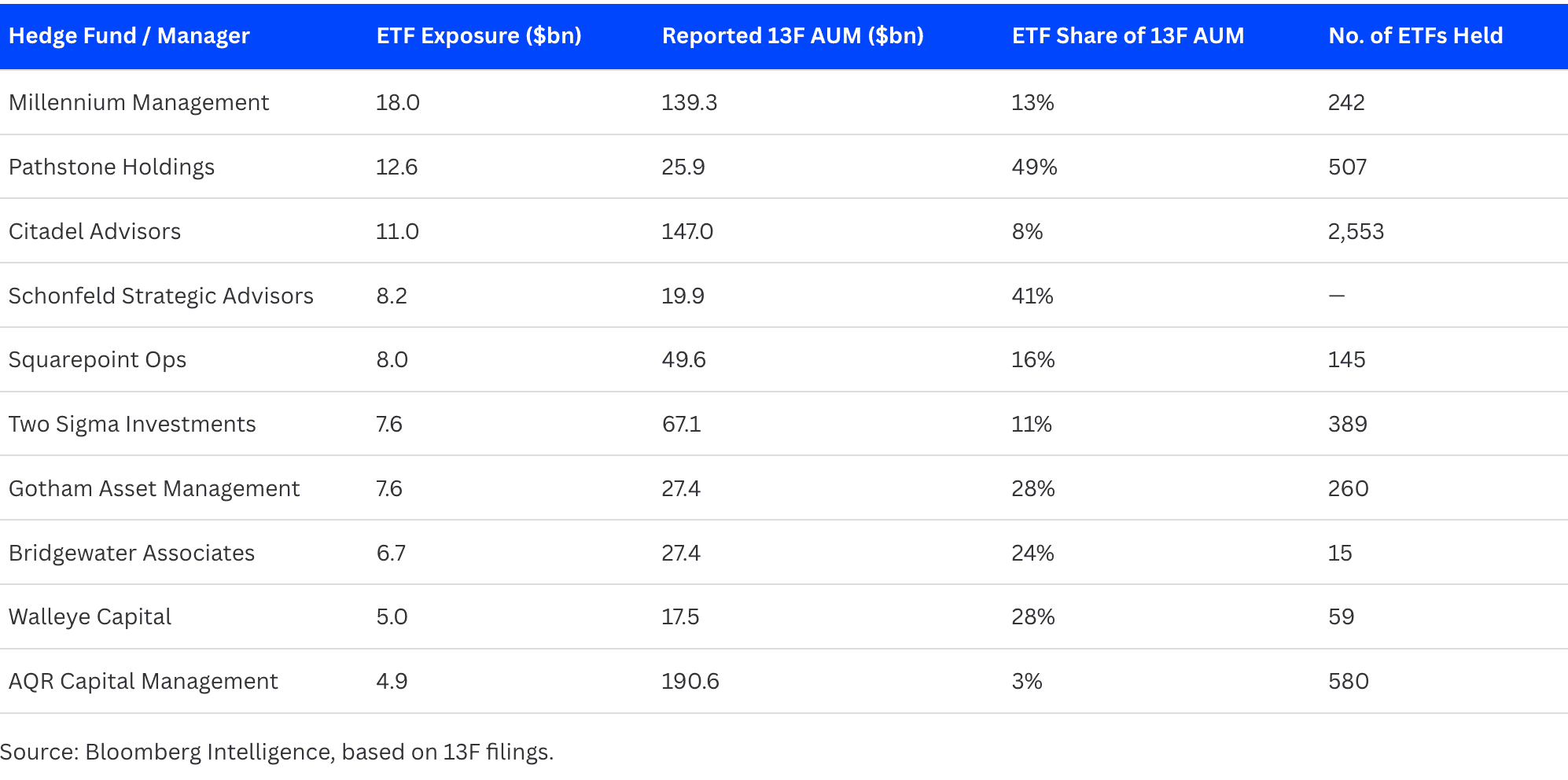

The data is based on 13F filings, which are quarterly disclosures required by the U.S. Securities and Exchange Commission (SEC) for institutional investment managers with at least $100 million in relevant securities under discretion. These filings are imperfect; they are delayed and do not fully capture short positions or derivatives but they remain one of the clearest windows into institutional ETF ownership.

Who Holds the Most ETFs?

According to Bloomberg Intelligence, Millennium Management leads hedge funds by ETF exposure, with $18.0 billion held across 242 ETFs. Pathstone Holdings follows with $12.6 billion, while Citadel Advisors holds $11.0 billion across more than 2,500 ETFs.

The spread is telling. Some firms, such as Citadel and AQR, hold hundreds or even thousands of ETFs, suggesting ETFs are being used as modular instruments across strategies. Others, such as Bridgewater, hold fewer funds but with larger allocation significance, implying broader macro or asset-allocation use.

Why Hedge Funds Use ETFs

The first reason is liquidity. Large ETFs such as SPY and QQQ trade with deep markets and tight spreads, making them useful for quickly adjusting exposure. State Street describes SPY as the world’s most traded ETF, with average daily volume of about 64 million shares, while Invesco says QQQ is the second-most-traded ETF in the U.S. by average daily volume as of end-2025.

For hedge funds, that liquidity has several uses. ETFs can equitize cash, hedge sector or market exposure, express macro views, manage factor risk, or create relative-value trades. A fund can buy a basket of semiconductor stocks and short a broad technology ETF, or own emerging-market debt while hedging with a country or currency-linked ETF. In many cases, ETFs are simply faster and cheaper than building or unwinding a basket of individual securities.

The second reason is precision. The ETF market now spans sectors, countries, commodities, fixed income, factors, options strategies and crypto. That gives hedge funds an expanding toolkit for exposures that once required futures, swaps or bespoke baskets.

Why This Matters for the ETF Industry

The rise of hedge fund ETF usage reinforces how far the wrapper has evolved. ETFs are no longer just passive products for buy-and-hold investors. They are now part of institutional market plumbing.

The broader ETF market has already been expanding rapidly. ICI data shows U.S. ETF net share issuance reached a record $1.1 trillion in 2024, up from $597 billion in 2023, while Citigroup recently projected U.S. ETF assets could more than double to $25 trillion by 2030.

Hedge fund adoption adds another layer to that growth story. It suggests ETFs are becoming not only asset-allocation vehicles, but also instruments for trading, liquidity management and risk transfer.

Hedge Funds Are Moving Closer to the GCC

The growing use of ETFs by hedge funds is increasingly intersecting with another trend: their physical expansion into the Gulf.

Over the past two years, several major global hedge funds have established or expanded offices in regional hubs such as Abu Dhabi and Dubai. Firms including Millennium Management, Point72 Asset Management, Balyasny Asset Management, and ExodusPoint Capital Management have all increased their presence in the UAE, while Bridgewater Associates has also deepened engagement with regional sovereign investors.

This is being driven by a combination of capital access, regulatory support, and geographic positioning, with Abu Dhabi in particular emerging as a key hub for institutional asset managers.

As hedge funds establish local operations, demand for liquid, tradable instruments including ETFs tends to follow, reinforcing the role of ETFs not just as investment vehicles, but as core tools within institutional portfolios.

The GCC Angle

As UAE and Saudi exchanges build out ETF ecosystems, institutional adoption will depend not only on headline themes, but also on spread quality, market-making depth, and the ability to enter or exit positions efficiently.

This is especially relevant as regional ETFs expand beyond broad market exposure into active, thematic, Shariah-compliant and options-based strategies. If ETFs are to become serious institutional tools in the GCC, they need the same attributes hedge funds value globally: transparency, tradability and reliable liquidity.

The Bottom Line

Hedge funds using ETFs is not a contradiction. It is a validation of the ETF structure. The world’s most sophisticated investors are increasingly using ETFs because they are liquid, precise and operationally efficient.

The irony is that ETFs were once marketed as the low-cost alternative to active management. Today, active managers themselves are among their heaviest users.