The International Monetary Fund has added its voice to a market already rattled by war, warning that the conflict in the Middle East has interrupted what had been a steadier global growth path. In its Spring Meetings commentary on April 14, the IMF said the closure of the Strait of Hormuz and damage to critical energy infrastructure have raised the prospect of a major energy shock, with consequences far beyond the region.

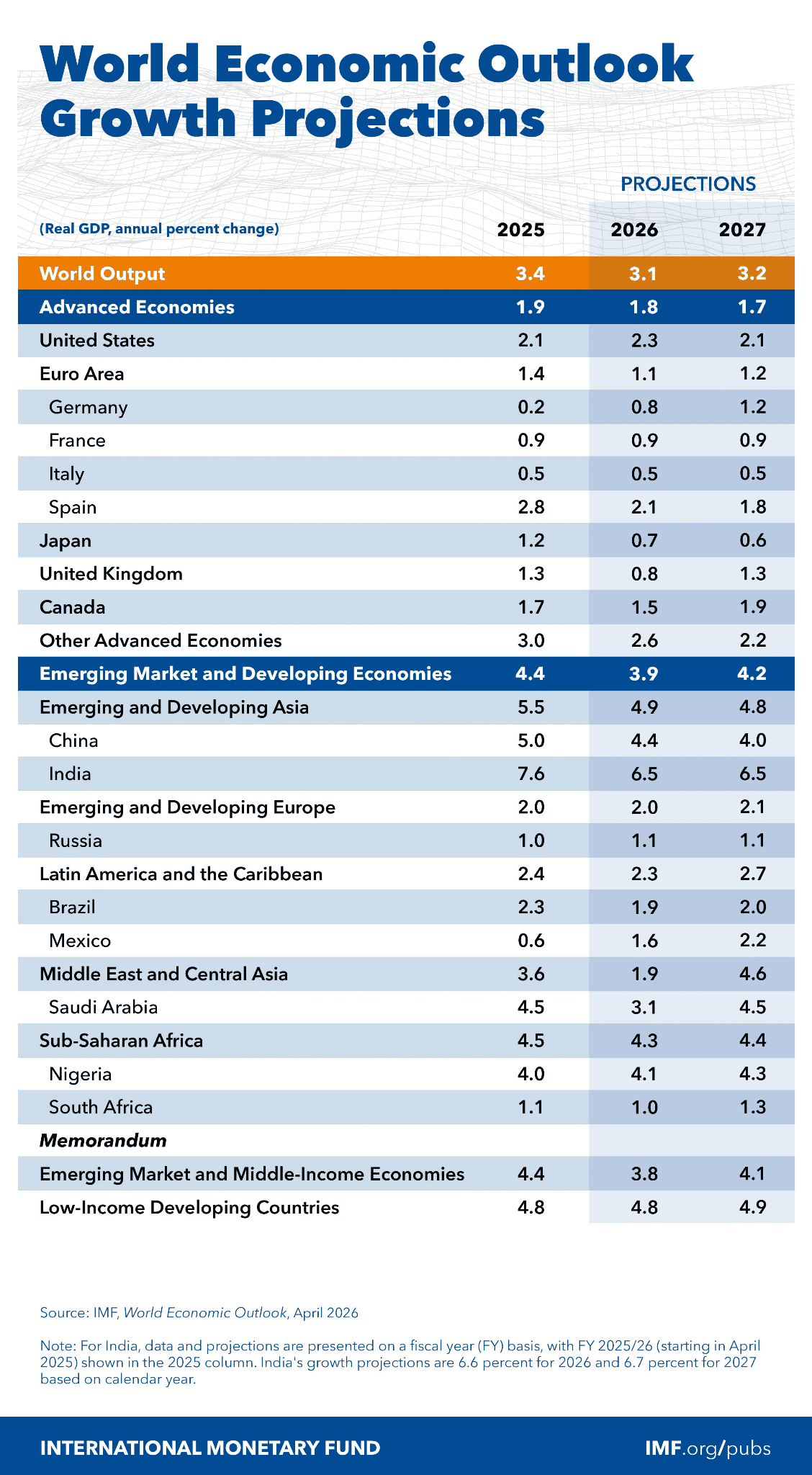

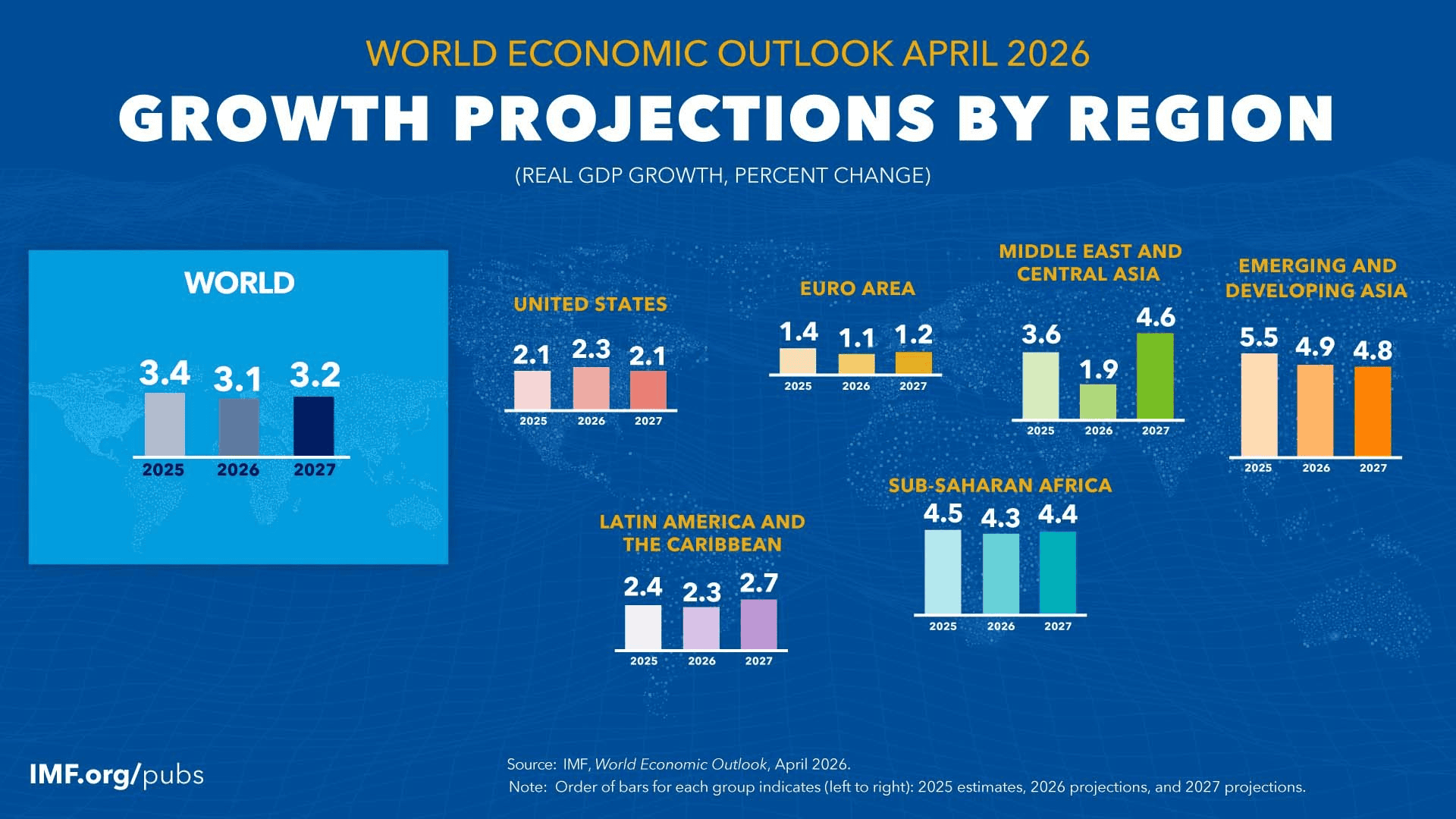

The headline numbers are sobering. In the IMF’s reference scenario, which assumes the conflict is relatively short-lived, global growth slows to 3.1% in 2026 and headline inflation rises to 4.4%. In a more adverse scenario, the Fund sees the potential for materially weaker growth and much hotter inflation if energy disruptions persist and financial conditions tighten further. Reuters and AP, summarising the same IMF outlook, reported that the downside case could drag global growth as low as 2% while sending inflation above 6%.

At the centre of the concern is oil. Reuters reported on April 15 that Brent crude was still trading near $95 a barrel as markets weighed whether diplomacy might reopen a path to calmer supply conditions, even as traffic through Hormuz remained heavily disrupted. The IMF’s own baseline assumes energy prices rise 19% this year, a reminder that even a conflict that cools before year-end can leave a sizable inflation scar. That matters because oil shocks do not stay in the oil market; they move into transport, fertilisers, industrial inputs and, eventually, consumer prices.

For Gulf investors, higher crude prices can look positive for hydrocarbon-linked state revenues, but the IMF was explicit that parts of the Gulf are also among the most exposed if the war directly impairs infrastructure or export routes. In the Fund’s briefing, officials said the damage is likely to be uneven, with conflict-affected Gulf economies facing the sharpest hit while other energy exporters may gain from price support but still suffer from broader inflation and trade disruption. Saudi Arabia, for example, was cited by the IMF as seeing a meaningful downgrade in 2026 growth because of weaker oil activity despite still-expanding output overall.

That sets up an interesting test for ETFs on the Abu Dhabi Securities Exchange. ADX said in February that it had 21 listed ETFs, underlining how quickly the market has become the region’s deepest ETF venue.

For investors trying to express a view on resilience rather than simply on oil, the obvious local building blocks are:

Chimera FTSE ADX 15 ETF (CHADX15), which tracks the exchange’s 15 largest names

Chimera S&P UAE Shariah ETF (UAEA), for domestic equities through a Shariah screen

Chimera S&P UAE UCITS ETF (UAED), for broader UAE equity exposure

Chimera JP Morgan Global Sukuk ETF (SUKUK), which offers access to investment-grade global sukuk.

The distinction matters. CHADX15, UAEA and UAED are equity expressions of UAE and ADX market exposure, so they may benefit if local liquidity and energy-linked earnings hold up, but they remain vulnerable to regional risk-off sentiment.

SUKUK is the more defensive instrument in the ADX toolkit: it is fixed income, globally diversified, and explicitly Shariah-compliant, which could make it more relevant for GCC allocators seeking ballast if volatility in regional equities worsens. In other words, this is not just a story about who wins from $90-plus oil; it is also about portfolio construction when inflation risk returns and shipping lanes become part of macroeconomics.

The IMF’s warning, then, is bigger than a single growth downgrade. It is a reminder that geopolitics can quickly turn into an asset-allocation problem. For ADX investors, the most useful ETF lens is not a heroic bet on crude, but a more practical question: how much of a portfolio should sit in regional equities that may be buoyed by higher energy prices, and how much should be parked in instruments like global sukuk that may prove steadier if the war’s economic aftershocks last longer than markets hope.