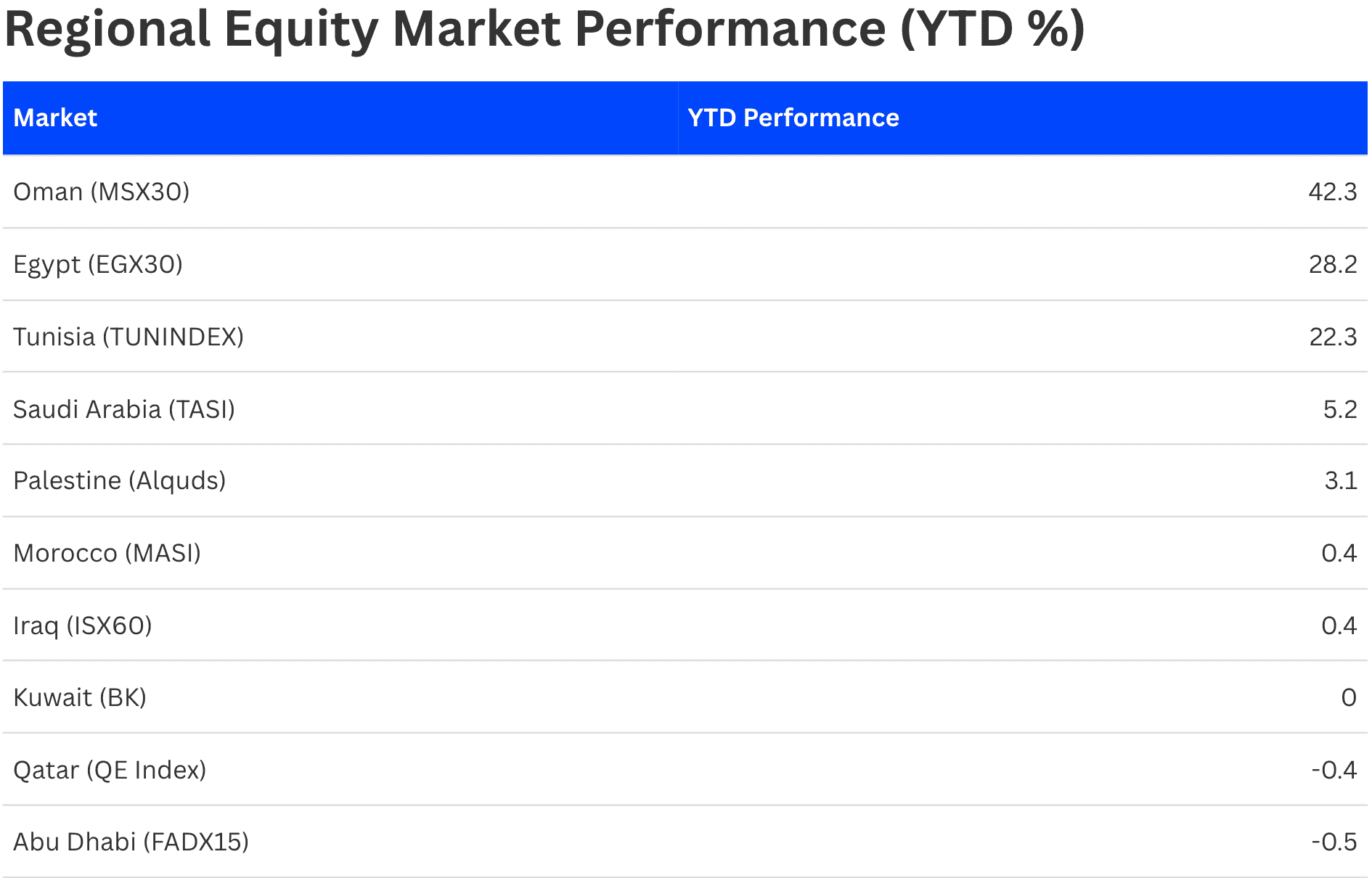

Oman’s stock market has quietly become one of the strongest-performing exchanges in the Arab world this year, with the Muscat Stock Exchange’s MSX30 Index rising 42.3% year-to-date as of May 7, 2026, according to the Arab Federation of Capital Markets (AFCM).

The rally places Oman well ahead of larger Gulf peers and highlights a broader divergence emerging across regional equity markets in 2026. While some GCC exchanges have struggled with oil volatility, geopolitical tensions, and foreign outflows, others are benefiting from banking strength, domestic reforms, and renewed investor positioning.

Saudi Arabia’s Tadawul All Share Index (TASI), the region’s largest equity market, was up 5.2% year-to-date, while Abu Dhabi’s FADX15 was marginally negative at -0.5%. Dubai’s DFMGI remained under pressure, down 1.9% over the same period.

Egypt also stood out despite macroeconomic volatility, with the EGX30 climbing 28.2% year-to-date, while Tunisia’s TUNINDEX advanced 22.3%. Kuwait’s benchmark index was broadly flat.

The performance gap is notable because GCC markets entered 2026 with broadly similar macro conditions: elevated oil prices, strong fiscal balances, and continuing infrastructure investment. Yet flows have become increasingly selective.

That divergence is increasingly being expressed through GCC-listed ETFs. Saudi Arabia’s market is primarily tracked through products such as the Albilad MSCI Saudi Equity ETF and Albilad MSCI Saudi Growth ETF on Tadawul, while UAE exposure is commonly accessed through the Chimera S&P UAE Shariah ETF listed on ADX. As regional performance gaps widen, these ETFs are increasingly becoming tactical allocation tools rather than simple passive market trackers.

Oman’s surge has coincided with improving fiscal metrics, stronger oil revenues, and rising investor optimism around economic diversification initiatives. The exchange has also benefited from relatively lighter foreign ownership positioning compared with larger GCC markets, which tend to react more directly to global risk sentiment.

Trading activity across the region, however, paints a more mixed picture.

Saudi Arabia continued to dominate regional liquidity, recording approximately $1.78 billion in trading value and over 298 million shares traded during the latest AFCM reporting session. Abu Dhabi and Dubai also maintained substantial activity levels despite softer index performance.

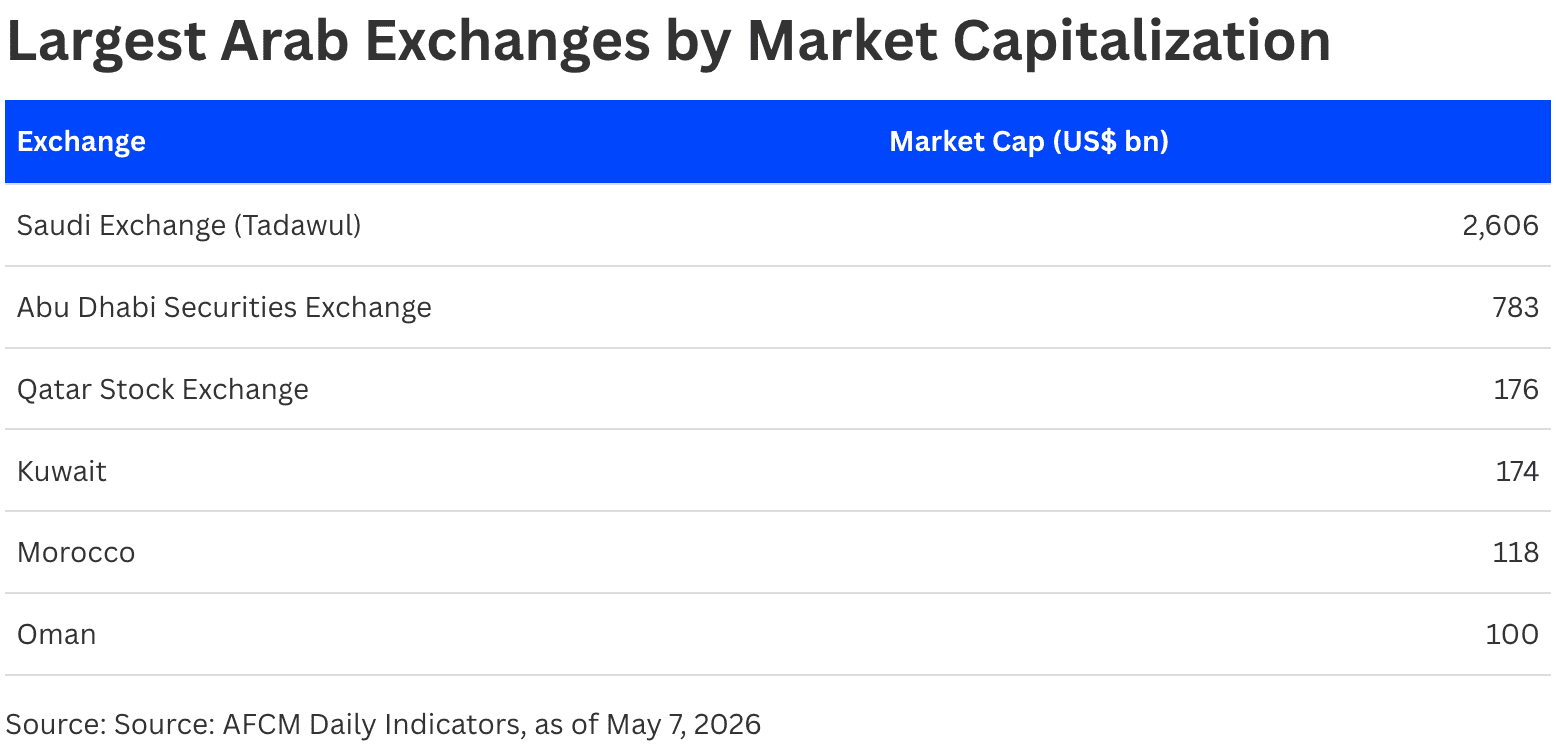

The contrast between performance and size is striking. Oman’s market capitalization remains relatively modest at roughly $100 billion compared with Saudi Arabia’s $2.6 trillion equity market, yet it has materially outperformed larger regional peers this year.

For investors, the data underscores an important shift underway in GCC equities. The region is no longer trading as a single macro oil story. Domestic reform cycles, liquidity conditions, sector composition, and foreign participation trends are increasingly driving country-level performance differences across Arab markets.