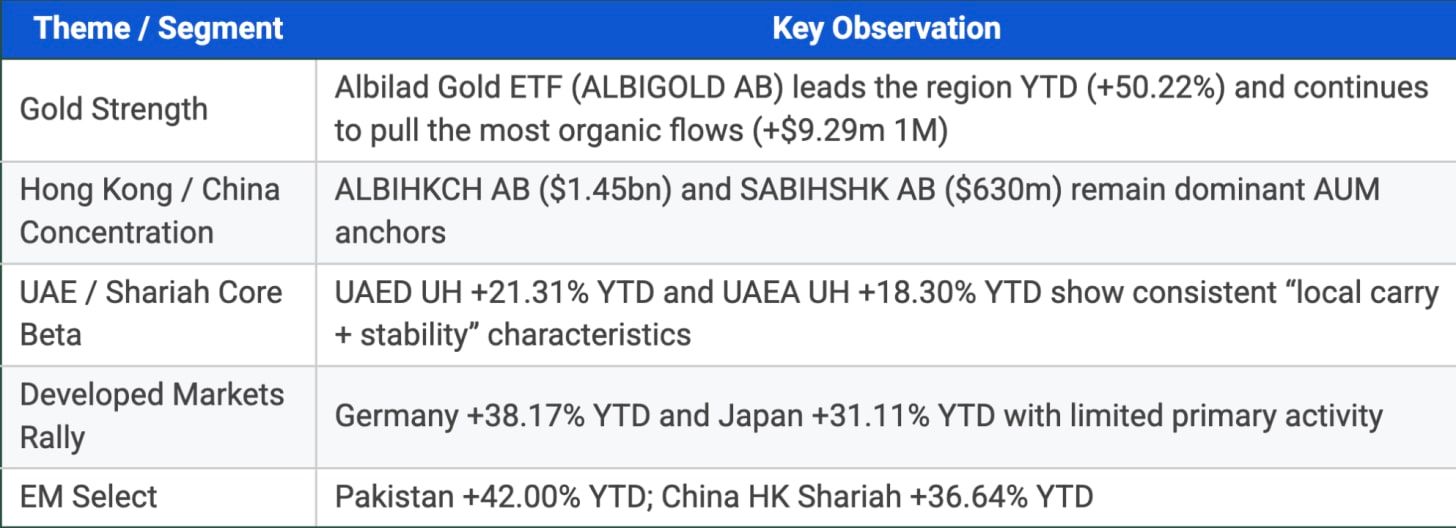

GCC ETF performance in October reflected a divergence between thematic global exposures and regional core beta. Gold continued to dominate both returns and flows, supported by safe-haven demand, macro uncertainty, and rising conviction trade adoption within GCC investors. Meanwhile Hong Kong / China–linked ETFs remain by far the largest asset concentration in the region, highlighting that international beta, when packaged in a familiar, listed, Shariah-suitable wrapper continues to attract GCC capital at scale.

Locally, UAE equity ETFs delivered another month of resilience, supported by stable earnings trends, ongoing structural improvements in liquidity, and strong corporate action pipelines. Shariah filters continue to play a structural role in the region not only as a religious preference variable, but increasingly as a practical quality filter, which tightens universes and reduces unintended factor drift. Despite that, primary creations across the region were quiet, suggesting price action was driven more by secondary market activity than by strategic allocation shifts in October.

Performance Highlights

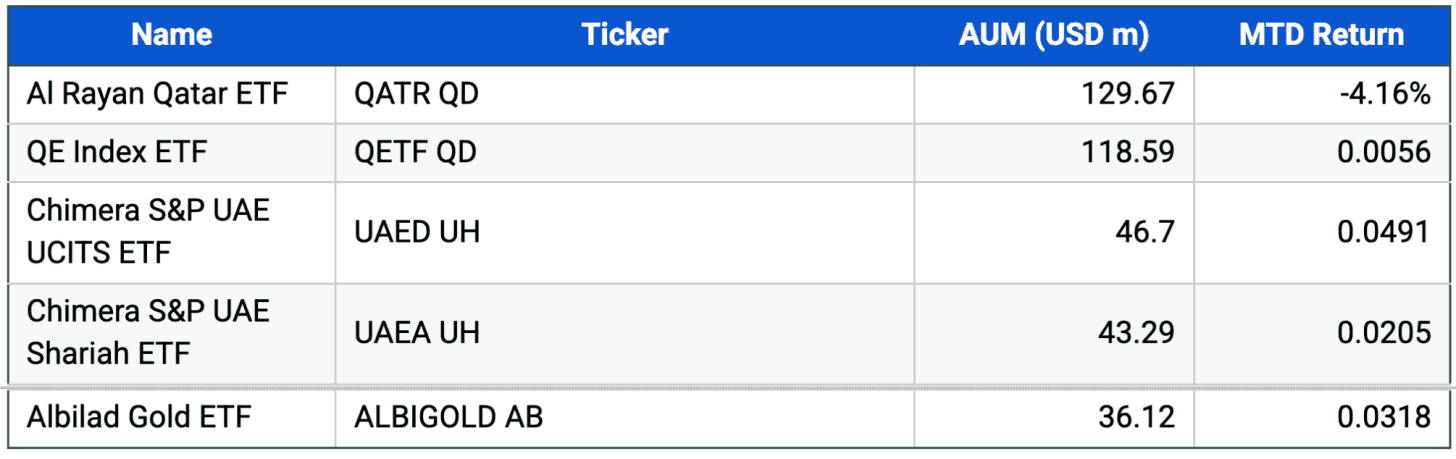

Core GCC ETFs – Monthly Snapshot

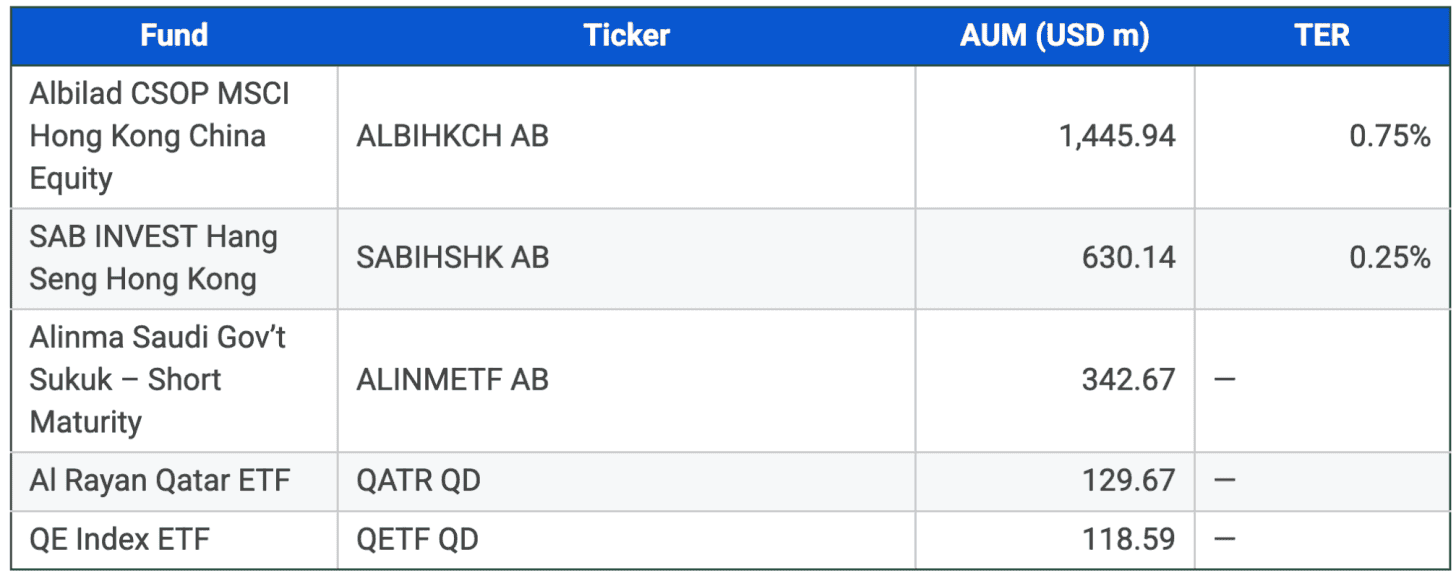

Top GCC ETFs by Assets

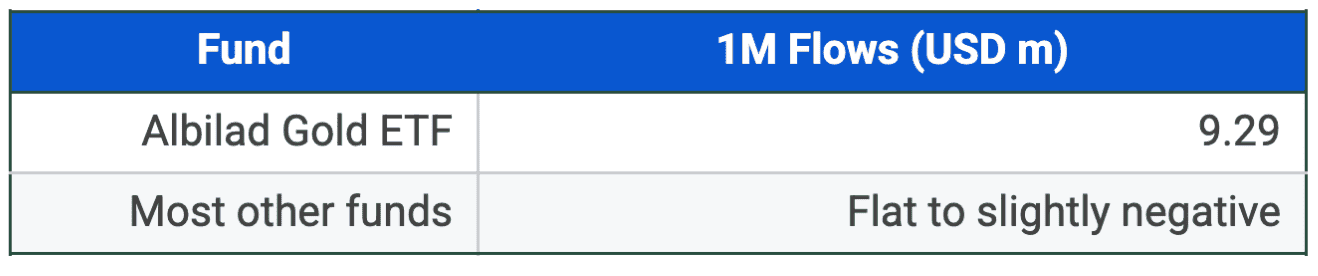

Flows

Costs & Liquidity

Costs remain reasonable for the region, with a median TER near ~0.75%. Hong Kong index trackers sit at the lower end of the range, while narrow single-country Shariah products are priced higher due to more restrictive universes and index licensing.

Liquidity dispersion remains wide, from <1,000 shares/day in niche funds to >200,000 shares/day in Albilad Gold highlighting where natural demand and trading comfort currently cluster. As more global issuers cross-list and market-makers scale, we expect spreads to tighten and implementation cost gaps to narrow.

Outlook into November

As GCC investor engagement with cross-listed global ETFs continues to grow, flows could begin to shift toward mega-cap thematic US tech, carbon markets, and India allocations — themes that are becoming more referenced across institutional CIO agendas and sovereign conversations.

Local markets have the structural capacity to capture that rotation especially as the listing pipelines in UAE, Saudi and Qatar continue to modernize and operational infrastructure (trading, settlement, interdealer liquidity) continues to improve.