The Shariah-compliant ETF universe is larger than most retail guides suggest, but it is still small, concentrated, and incomplete.

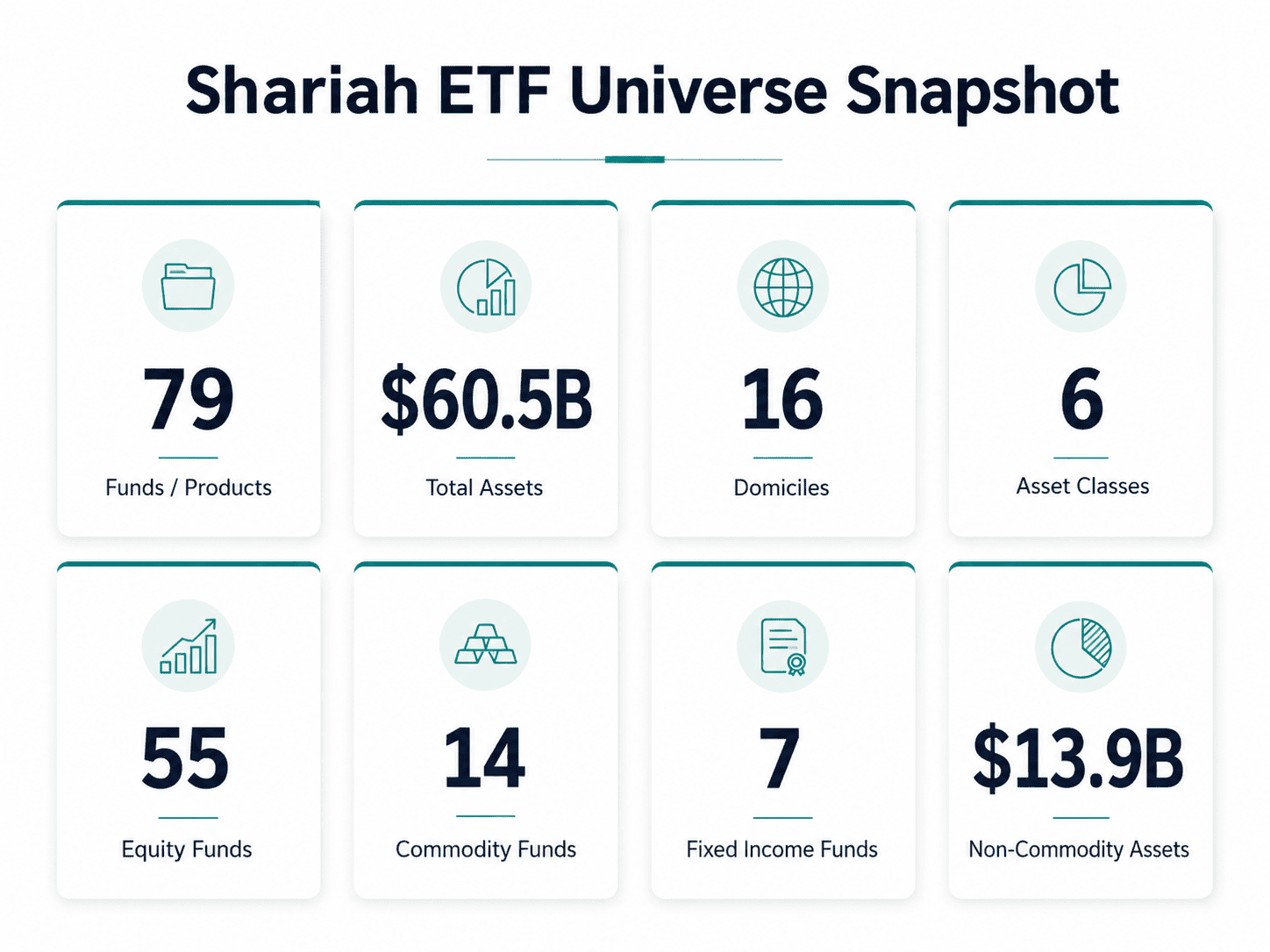

Currently there are 79 Shariah-compliant ETFs and ETPs with around $60.5 billion in assets across 16 domiciles and six asset classes. On paper, that sounds like a meaningful market. In practice, the universe is still narrow. Around 77% of total assets sit in commodity products, mostly gold and precious-metal ETPs.

The Shariah-compliant ETF market exists, but it is not yet a complete portfolio ecosystem. Investors can access gold, global equities, U.S. equities, some sukuk, and a growing number of regional equity products. But the market remains light in fixed income, income strategies, real estate, multi-asset solutions, cash-like products, and low-cost regional building blocks.

The Market Is Still Small

The global ETF industry has crossed $23 trillion in assets. Against that, the Shariah-compliant universe at around $60.5 billion, represents less than 0.3% of global ETF assets.

Islamic finance is a global industry, Muslim investors represent a large and growing investment audience, and ETFs have become one of the most important vehicles for low-cost portfolio construction. Yet Shariah-compliant ETFs remain a very small corner of the global ETF market. Which indicates an early market to explore.

The Universe Is Broad by Count, But Concentrated by Assets

The first thing to understand is the difference between fund count and asset scale.

Equity products dominate by number the Shariah compliant ETFs. There are around 55 equity funds, making equity the largest category by product count. But those equity funds hold only around $11.7 billion, or roughly 19% of total assets.

Commodities tell the opposite story. There are only 14 commodity products, but they hold around $46.7 billion, or roughly 77% of the universe. This is mainly driven by large physical gold and precious-metal products.

Fixed income remains small. There are around 7 fixed-income products, with around $1.2 billion in assets. Real estate and multi-asset exposure are almost absent.

This is the market’s biggest imbalance: investors may see nearly 80 products, but most of the capital is concentrated in one asset class.

Commodities Still Dominate the Asset Base

The biggest product in the Shariah-compliant ETF market is Invesco Physical Gold ETC, with around $26.5 billion in assets. Other large products include WisdomTree Physical Gold, WisdomTree Physical Swiss Gold, WisdomTree Physical Silver, and WisdomTree Core Physical Gold.

The key word is physical. For Shariah investors, the structure matters as much as the asset itself. A gold or silver product is generally easier to assess when it is backed by real, allocated metal held in custody, rather than exposure created synthetically through derivatives or unsecured financial contracts.

That links back to core Islamic finance principles: the investment should be tied to a real underlying asset, ownership should be clear, and the structure should avoid riba interest, excessive uncertainty or gharar, and speculation or maysir. Physical commodity products can fit more naturally within that framework, but only when the custody, ownership, redemption, and trading mechanics have been reviewed and approved by qualified Shariah scholars.

This helps explain why commodity products, especially gold, make up such a large share of the Shariah ETF universe. Gold products are important, and for many Muslim investors they are a natural Shariah-compliant store of value. But investors should still check whether each product has a Shariah certificate and whether its structure, custody, and trading mechanism have been reviewed by qualified Shariah scholars.

It also explains why the total Shariah ETF universe looks much bigger than the investable portfolio universe actually feels. Gold can play a role in a portfolio, but gold alone does not build a complete portfolio.

Once commodity products are removed, the non-commodity Shariah ETF universe falls to around $13.9 billion. That is the more relevant number for investors looking for diversified equity, sukuk, income, and allocation products.

Assets Are Concentrated Offshore

The second major concentration is domicile.

Ireland has 19 products and around $33.8 billion in assets. Jersey has 7 products and around $17.4 billion. Together, they account for roughly 85% of the total assets in the dataset.

This is largely because many of the largest UCITS and commodity products are domiciled in Ireland and Jersey. These are important markets for ETF infrastructure, cross-border distribution, and exchange-traded commodity products.

By contrast, Muslim-majority markets have a more limited asset scale. Saudi Arabia has 11 products and around $1.8 billion in assets. The UAE has 11 products but only around $238 million. Malaysia has 7 products with around $261 million. Qatar, Turkey, Pakistan, Nigeria, and other markets remain much smaller.

Product Launches Have Accelerated Since 2020

The Shariah-compliant ETF universe is still being built.

Since 2020, 51 products have launched, representing around 65% of the full universe by fund count.

The most active years were 2020, with 11 launches, 2022, with 13 launches, and 2024, with 9 launches. There were also 5 launches in 2026.

This matters because the market should not be judged like a fully developed ETF ecosystem. It is closer to an early-stage product category moving into its next phase.

A Few Products Hold Most of the Money

The universe is also concentrated at the fund level.

The top 5 products account for around 72% of total assets. The top 10 products account for around 84%. Many of the largest products are gold, silver, or broad global equity funds.

This concentration creates a gap between headline size and practical depth. A market can have $60 billion in assets, but if most of that capital sits in a few commodity products, investors still do not have enough diversified tools to build complete portfolios.

The largest non-commodity products include funds such as SP Funds S&P Sharia Industry Exclusions ETF, iShares MSCI World Islamic UCITS ETF, Albilad CSOP MSCI Hong Kong China ETF, and Invesco Dow Jones Islamic Global Developed Markets UCITS ETF. These products show that equity demand exists, but the universe remains heavily dependent on a small number of issuers and strategies.

Flows Show Where Demand Is Emerging

Flows show that investor demand is not limited to gold. While commodities dominate total assets, recent flow activity is also appearing in equity and sukuk building blocks.

Among USD-reported products, the strongest YTD inflows were led by SP Funds S&P Sharia Industry Exclusions ETF, with around $620 million in inflows, followed by WisdomTree Core Physical Gold at around $314 million, SP Funds Dow Jones Global Sukuk ETF at around $206 million, and iShares MSCI EM Islamic at around $190 million.

Top Shariah ETFs by YTD Inflows

The biggest YTD outflows came from Invesco Physical Gold ETC, at around $908 million, followed by WisdomTree Physical Silver at around $631 million, WisdomTree Physical Gold at around $485 million, and WisdomTree Physical Swiss Gold at around $460 million.

Top Shariah ETFs by YTD Outflows

The outflow side is heavily concentrated in precious-metal products. The largest YTD outflow came from Invesco Physical Gold ETC, which saw around $908 million leave the product. It was followed by WisdomTree Physical Silver, with around $631 million in outflows, WisdomTree Physical Gold, with around $485 million, and WisdomTree Physical Swiss Gold, with around $460 million.

The important point is that the biggest outflows are not coming from the broader Shariah equity category. They are mostly coming from large gold, silver, platinum, and palladium products. That suggests the current outflow pressure is more tied to positioning in precious metals than a rejection of Shariah-compliant ETFs as a portfolio category.

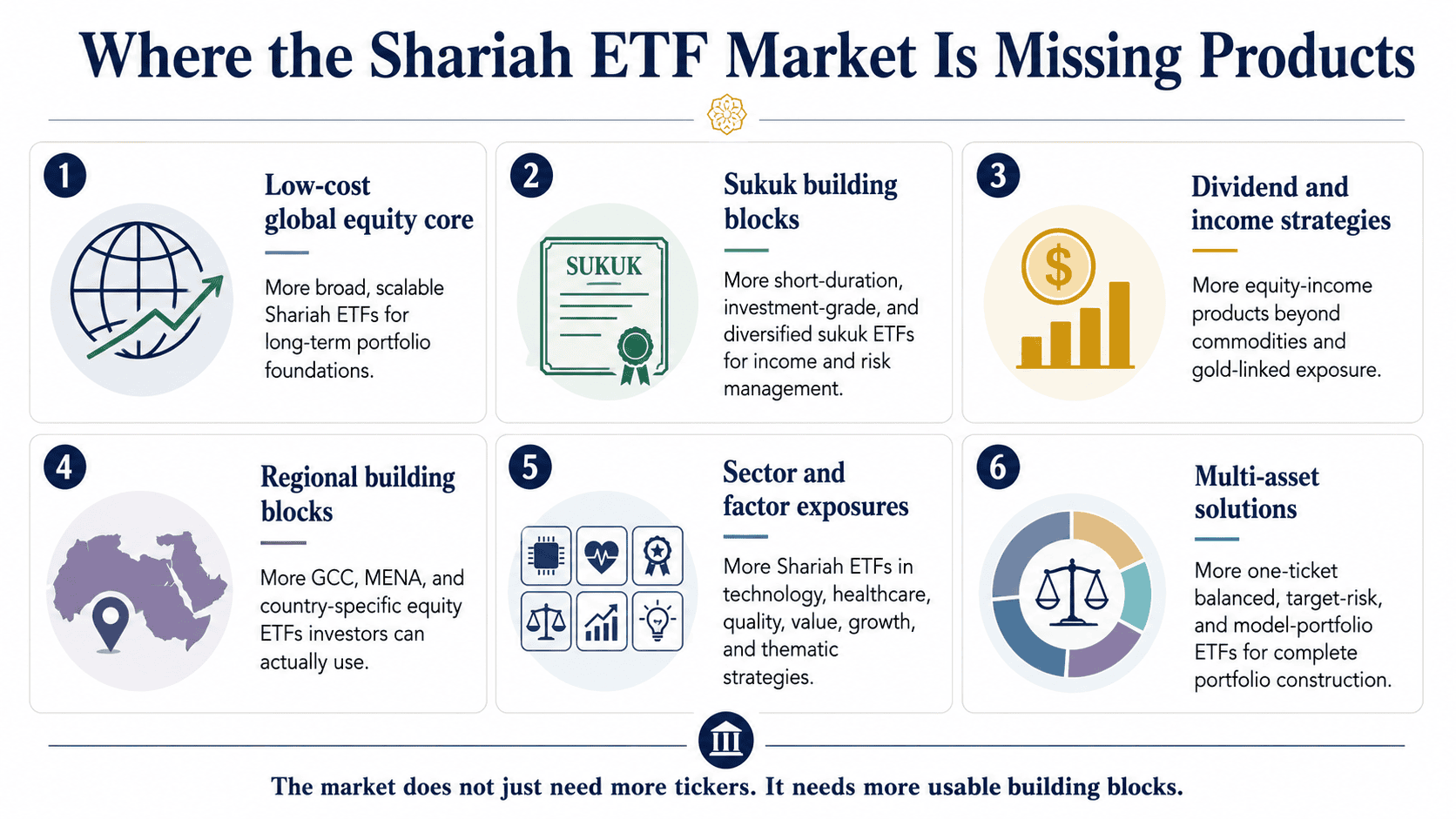

Why We Need More Shariah-Compliant ETFs

The market does not need more Shariah ETFs just for the sake of more tickers. It needs better products in the categories that matter most for portfolio construction.

First, the market needs more core equity building blocks. There are global and U.S. Shariah equity ETFs, but the market still needs more low-cost choice across global, U.S., emerging-market, GCC, and country-specific exposures.

Second, the market needs more fixed-income and sukuk products. Fixed income is one of the weakest parts of the universe. There are only 7 fixed-income products in the dataset, with around $1.2 billion in assets. For Muslim investors who want balanced portfolios, this is a major limitation.

Third, the market needs more income strategies. Dividend ETFs, sukuk income ETFs, short-duration sukuk, and diversified income products could become major categories. The launch of new GCC dividend products shows that income is one of the most important opportunities.

Fourth, the market needs more regional exposure. Saudi Arabia, the UAE, Qatar, Malaysia, Turkey, and other Islamic finance markets should have deeper ETF ecosystems. Local investors need simple ways to access their own markets without buying individual stocks.

Fifth, the market needs more multi-asset products. One of the biggest gaps is the lack of simple Shariah-compliant allocation funds that combine equities, sukuk, commodities, and cash-like exposure in one vehicle.

The Opportunity for Issuers

The opportunity is to build the missing infrastructure for Muslim investors.

This is where the market can grow, through better portfolio tools.

Final thoughts

The Shariah-compliant ETF universe includes 79 products and around $60.5 billion in assets today. But the market is still far from complete.

Most assets remain concentrated in commodities. Most scale sits offshore. Equity products have grown, but fixed income, income strategies, real estate, and multi-asset solutions remain underbuilt.

That is why the next phase of Shariah ETFs should be about building the missing portfolio infrastructure for Muslim investors: diversified, low-cost, transparent, liquid, and usable across real portfolios.

Investors should also be careful with commodity ETFs. A commodity exposure is not automatically Shariah-compliant just because the underlying asset is gold or another physical commodity. Investors should check whether the product has a clear Shariah certificate, who issued it, and whether the fund structure, custody, and trading mechanism have been reviewed by qualified Shariah scholars.

The demand is already there. The product set still needs to catch up.