The Korean defense industry has been rising in prominence especially in the GCC and in light of the US Iran conflict.

As geopolitical risks rise across the region, Gulf countries are accelerating investments in air defense, missile interception, and rapid-response systems. Increasingly, that demand is being met by South Korean manufacturers, whose combination of cost efficiency, fast delivery, and technology transfer aligns closely with regional priorities.

At the center of this shift is missile defense, driven by rising regional security needs amid the recent conflict in the region and it is increasingly accessible to investors through listed Korean defense companies and ETFs.

Missile Defense Demand Is Driving the Market

Recent tensions have reinforced a critical reality: missile interceptors are now one of the most essential layers of modern defense systems. Compared to traditional large-scale military platforms, interceptor systems are:

- Faster to deploy

- More cost-effective

- Highly scalable

- Designed for real-time threat environments

South Korea’s Cheongung-II (KM-SAM) system has emerged as a standout solution, already deployed in both the UAE and Saudi Arabia. With reported interception success rates near 90%, it is increasingly seen as a credible and more cost-efficient alternative to Western systems such as Patriot.

For GCC countries, this matters. Defense strategy is shifting from deterrence alone to active protection of infrastructure, cities, and population centers. Korean systems are playing a key role in enabling that transition.

From Buyer to Strategic Partner

The relationship between South Korea and the GCC is also evolving beyond simple procurement.

The UAE has signed defense cooperation agreements exceeding $35 billion, covering air defense, aerospace, and naval capabilities. Similarly, Saudi Arabia is aligning Korean partnerships with its Vision 2030 goal of localizing defense production, including joint R&D and manufacturing initiatives.

This reflects a deeper shift. Unlike traditional suppliers, South Korea offers:

- Technology transfer

- Local production partnerships

- Long-term maintenance ecosystems

This model aligns closely with GCC ambitions to build domestic defense industries, not just import capabilities.

Speed Is the Competitive Advantage

While global leaders like Lockheed Martin and BAE Systems dominate high-end systems, South Korea has built its reputation on execution.

Its defense companies, including Hanwha Aerospace, Hyundai Rotem, and Korea Aerospace Industries are structured for rapid production and delivery, a critical advantage in today’s environment where procurement timelines are shrinking.

This is why order backlogs are expanding. Countries are no longer just buying capability, they are buying certainty of delivery.

How to invest in the Korean defense opportunity?

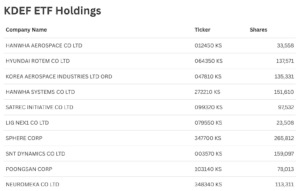

For investors, this trend is increasingly accessible through the PLUS Korea Defense Industry Index ETF (KDEF).

The ETF tracks a basket of South Korean defense-linked companies and provides direct exposure to the sector’s growth. According to its February 2026 factsheet, the fund holds 23 companies and is heavily concentrated in industrial and aerospace segments.

These are precisely the companies benefiting from rising GCC demand for missile defense, artillery systems, and aerospace platforms.

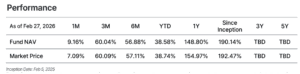

Performance has also reflected this momentum. As of February 2026, the ETF has delivered:

- ~38% year-to-date

- ~148% over one year

- Nearly 190% since inception

This underscores how closely defense equities are tracking geopolitical demand cycles.

A Strategic Alignment, Not a Trade

The broader story is not just about exports, it is about alignment.

The GCC is investing heavily to ensure regional stability and protection of its economies and citizens, while South Korea is positioning itself as a reliable, long-term partner capable of supporting that objective through technology, speed, and collaboration.

As defense spending continues to rise globally, this partnership is likely to deepen.

For investors, that creates a clear thematic:

the rise of a new defense supply chain, faster, more flexible, and increasingly centered around Asia.