BlackRock is progressing from crypto experimenter to infrastructure innovator, exploring plans to place traditional ETFs, covering equities and bonds onto public blockchains. Bolstered by the success of its spot Bitcoin ETF and tokenized money-market fund (BUIDL), valued at over $2.2 billion, the firm is now eyeing tokenization of mainstream ETFs tied to real-world assets.

Tokenization promises 24/7 trading, frictionless cross-border access, real-time settlement, and new collateral uses all underpinned by blockchain transparency. This innovation has profound ramifications for global markets, and especially for GCC ETF investors, who routinely grapple with limited access to U.S. products, regulatory frictions, and liquidity constraints in regional exchanges.

Tokenization Takes Shape: Global Data & Infrastructure

Nasdaq has recently filed a proposal (SR-NASDAQ-2025-072) with the U.S. SEC to allow tokenized equity securities and exchange-traded products (ETPs) including ETFs to trade on its main market. Researchers suggest this could potentially unlock trillions of dollars in liquidity over time.

BlackRock’s tokenized money market fund, BUIDL, launched in 2024 and has surpassed $1.9 billion in assets under management (AUM), with institutional demand surging one report notes approximately $800 million added within just two weeks during its growth spurt.

Meanwhile, the broader real-world asset (RWA) tokenization market has grown by 380% over the past three years, reaching $24 billion by mid-2025. Forecasts from Standard Chartered suggest this market could balloon to $30 trillion by 2034, a stark indication of tokenization’s vast potential.

Although on-chip asset volumes are still modest relative to traditional finance, the trend is clear: tokenization is moving from experimental stages to scaled institutional adoption, supported by rising demand, regulatory pilots, and infrastructure upgrades.

What’s Already Happening in the GCC

Abu Dhabi Global Market has already green-lit a live tokenized fund. On October 31, 2024, Abu Dhabi–based Realize launched the Realize T-BILLS Fund (RBILL), which invests in U.S. Treasury ETFs from BlackRock and State Street and issues a $RBILL token that represents fund units on Ethereum and IOTA. The fund set a $200 million AUM target and is managed by Neovision Wealth Management; the regulator confirmed it as ADGM’s first tokenized T-bills fund, with the structure explicitly allowing token trading on public chains. Reuters reported the launch and mechanics, while ADGM’s notice and Realize’s fund page detail the token rails and objectives.

The GCC experiment sits alongside global tokenized cash and Treasury pilots that have scaled rapidly. Franklin Templeton’s OnChain U.S. Government Money Fund reported about $707 million in net assets as of July 31, 2025, while trackers show the broader on-chain real-world-asset market at roughly $29.17 billion as of September 12, 2025. These figures illustrate that tokenized fixed income is moving from concept to production, with GCC regulators already providing a tested path via ADGM.

Why This Could Matter for GCC ETF Investors

Access and tax treatment are the immediate draws. Many Gulf investors use Ireland-domiciled UCITS ETFs to access U.S. markets because U.S. dividends paid into a U.S.-domiciled ETF are generally withheld at 30% for investors from countries without a treaty, while the U.S.–Ireland treaty allows 15% withholding inside Irish UCITS that hold U.S. equities.

Tokenized ETFs, if structured through treaty-friendly domiciles and distributed on public chains, could preserve the treaty benefit while easing subscription and settlement frictions that often complicate access to U.S. products from the GCC.

Liquidity and tradability are the other levers. Tokenization enables 24/7 trading and fractional ownership, which can deepen secondary market activity around smaller ticket sizes and off-exchange hours. Public dashboards show tokenized Treasuries and cash equivalents have surpassed about $7.4 billion on public chains by early September 2025, and total tokenized RWAs ex-stablecoins hover in the $26–29 billion range.

If GCC issuers extend the RBILL template to tokenized sukuk or tokenized equity ETFs, ADX, DFM, and Tadawul listings could be complemented by on-chain units that broaden the investor base, compress bid–ask spreads in quiet sessions, and improve collateral utility in repo and DeFi workflows.

Sharia compliance is feasible but will require clear guardrails. Programmable on-chain units make it easier to embed screening, purification, and asset-use controls at the smart-contract level, yet issuers and regulators will still need to codify standards for tokenized sukuk and Islamic equity exposures.

In practice, the GCC follows the AAOIFI standards (Bahrain-based) that draw on all four Sunni schools of jurisprudence, though Hanafi and Shafi’i interpretations dominate in the UAE, Qatar, and much of Southeast Asia, while Hanbali is most prevalent in Saudi Arabia. These jurisprudential traditions influence how financing structures are screened for riba (interest), gharar (excessive uncertainty), and asset-backing.

With ADGM already admitting a tokenized Treasury product and Singapore’s MAS Project Guardian coordinating multi-bank pilots for tokenized funds and bonds, the policy momentum exists to translate these standards into the Gulf’s regulatory vernacular.

Challenges & Caveats on Tokenization

Regulatory Alignment

Tokenized ETFs would have to bridge the gap between traditional clearing cycles (T+2) and instant blockchain settlement. This isn’t just a technical issue but a regulatory one: today, ETFs in the U.S. rely on the Depository Trust & Clearing Corporation (DTCC), while on-chain assets would bypass that infrastructure. Reconciling parallel systems could expose investors to mismatches in settlement and legal ownership. Custody obligations also remain unresolved: under current SEC rules, registered custodians must hold client assets, yet tokenized ETFs might reside in digital wallets or smart contracts, raising questions about who bears fiduciary responsibility.

Liquidity Realism

While tokenized Treasuries and money-market funds have surpassed $7 billion AUM on public chains, secondary market activity remains thin. Studies show that many tokenized RWA tokens are held by a handful of wallets, with relatively few active daily transactions. This suggests current demand is concentrated among institutions testing settlement efficiency, not broad retail participation. Without exchange-level liquidity, tokenized ETFs could risk becoming “buy-and-hold shells” rather than fluid trading instruments.

Investor Protections

Tokenized ETFs introduce additional risks tied to smart contracts, oracles, and cross-chain interoperability. Unlike a traditional ETF, where errors or fraud fall under securities law with established recourse, a coding error in a smart contract or manipulation of an oracle feed could result in immediate losses. This raises questions about jurisdiction: would an investor in Dubai, trading a tokenized ETF issued in Ireland but built on Ethereum, fall under UAE law, EU law, or no clear framework at all? The SEC and ESMA have acknowledged this gap but have yet to propose comprehensive safeguards.

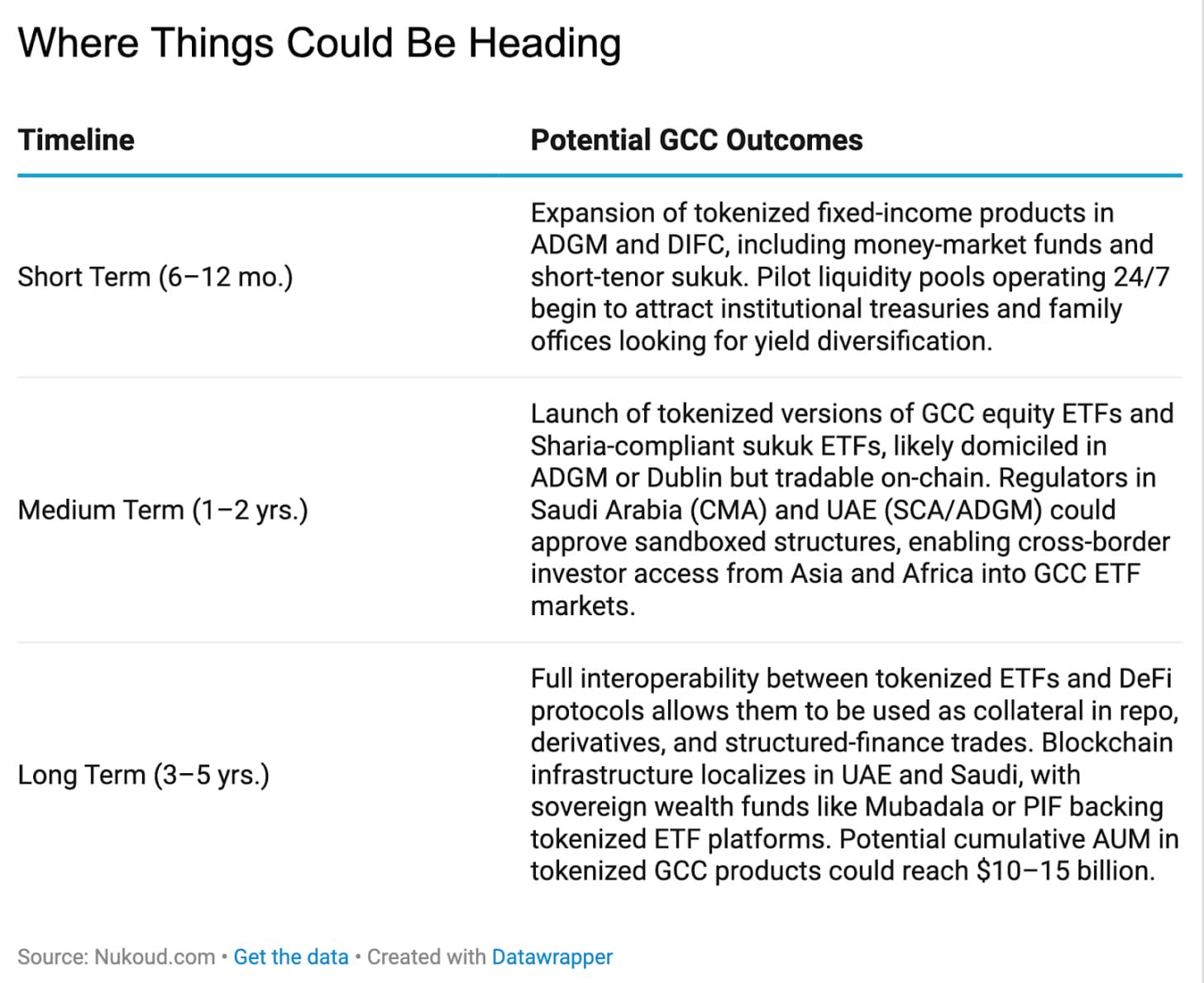

Tokenization as the Next Frontier for ETF Markets

BlackRock’s move into tokenizing ETFs marks an important moment in integrating traditional finance with blockchain capabilities. For GCC investors, this opens new frontiers: easier global access, Sharia-compliant innovation, and potentially deeper liquidity for ETF products.

But unlocking this future will require progress on regulation, secondary market infrastructure, and investor protections. Tokenization may not just be a technical transformation it could become a strategic tool for broadening asset access across the Gulf.