In the rapidly evolving world of finance, Exchange-Traded Funds (ETFs) have cemented their position as a fundamental investment vehicle, appealing equally to newcomers and experienced traders. These funds offer a powerful blend of diversification, low cost, and flexibility, presenting a highly attractive substitute for actively managed mutual funds and the complexities of selecting individual stocks. Read about ETF investing in 2026

Let’s understand the history of ETFs:

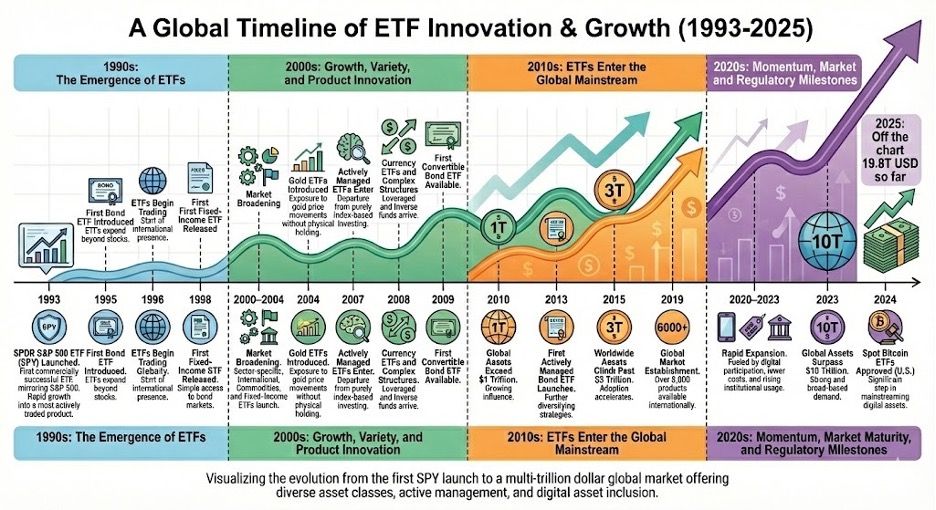

1990s: The Emergence of ETFs

ETFs began their modern rise in 1993 with the launch of the SPDR S&P 500 ETF (SPY) on the American Stock Exchange one of the first funds to achieve true commercial success and a simple, tradable way to track the S&P 500.

From there, the product set quickly widened: bond and fixed-income ETFs emerged in the mid-1990s, ETFs began trading outside the U.S. by 1996, and by the early 2000s the market had expanded into sectors, international exposures, commodities, and broader fixed income.

A major milestone came in 2004 with the introduction of gold ETFs, allowing investors to access gold price movements without owning physical metal, followed by the arrival of actively managed ETFs (2007), currency ETFs, and more complex leveraged and inverse structures (2008), and niche exposures such as convertible-bond ETFs (2009).

By the 2010s, ETFs had moved firmly into the global mainstream with worldwide assets exceeding $1 trillion in 2010, expanded to more than $3 trillion by 2015, and by 2019 there were over 6,000 ETFs available internationally.

The 2020s then brought both maturity and acceleration, driven by digital adoption, lower costs, and deeper institutional usage, pushing global ETF assets past $10 trillion in 2023. Regulatory milestones also helped broaden the universe, notably the approval of spot Bitcoin ETFs in the U.S. in 2024, bringing digital assets further into traditional portfolios.

By 2025, total global ETF assets are estimated at roughly $19.8 trillion, highlighting just how central ETFs have become to modern investing.

- 1993: The SPDR S&P 500 ETF (SPY) is launched on the American Stock Exchange, becoming the first ETF to gain commercial success and offering investors an easy way to mirror the performance of the S&P 500. It rapidly grew into one of the most actively traded products in the market.

- 1995: ETFs expand beyond stocks with the introduction of the first bond ETF.

- 1996: ETFs begin trading outside the United States, marking the start of their global footprint.

- 1998: The first fixed-income ETF is released, giving investors simple access to bond markets through an exchange-traded instrument.

2000s: Growth, Variety, and Product Innovation

- 2000-2004: The ETF market broadens significantly with the launch of sector-specific funds, international ETFs, and products offering exposure to commodities and fixed-income assets.

- 2004: Gold ETFs are introduced, enabling investors to participate in gold price movements without holding the physical metal.

- 2007: Actively managed ETFs enter the market, representing a departure from purely index-based investing.

- 2008: The lineup expands further with the arrival of currency ETFs and more sophisticated structures, including leveraged and inverse funds.

- 2009: The first ETF targeting convertible bonds becomes available.

2010s: ETFs Enter the Global Mainstream

- 2010: Global ETF assets exceed $1 trillion, underscoring the model’s growing influence.

- 2013: The first actively managed bond ETF launches, further diversifying active strategies.

- 2015: Worldwide ETF assets climb past $3 trillion as adoption accelerates.

- 2019: ETFs firmly establish themselves in global markets, with over 6,000 products available internationally.

2020s: Momentum, Market Maturity, and Regulatory Milestones

- 2020-2023: The ETF sector experiences rapid expansion fueled by increased digital participation, lower costs, and rising institutional usage.

- 2023: Global ETF assets surpass $10 trillion, reflecting strong and broad-based demand.

- 2024: The approval of spot Bitcoin ETFs in the U.S. marks a significant point in bringing digital assets into the mainstream investment landscape.

- 2025: Off the chart 19.8T USD so far

From Wrapper to Market Infrastructure

What began as a low-cost indexing experiment has become a central pillar of global capital markets. As of end-November 2025, exchange-traded funds collectively held about US$19.4 trillion in assets worldwide, spread across more than 15,600 ETFs and roughly 30,400 listings on 83 exchanges in 65 countries, according to industry data.

Assets have expanded at a striking pace up roughly 31% year-to-date in 2025, from about US$14.9 trillion at the end of 2024 reflecting how ETFs are now routinely used for everything from long-term asset allocation to short-term liquidity management.

The scale is also increasingly institutional: a handful of global providers dominate flows and assets, with the largest alone controlling well over a quarter of the market. For investors in the GCC, this sheer depth and standardization is precisely what makes ETFs such a powerful transmission mechanism linking regional portfolios to global markets with unprecedented efficiency.

ETFs In GCC

The history of Exchange-Traded Funds (ETFs) within the Gulf Cooperation Council (GCC) region is relatively recent, yet it has rapidly accelerated, driven by a regional strategic focus on capital market deepening and economic diversification. Read more about it here.

While global ETFs were pioneered in the 1990s, the GCC market began its journey in the early 2010s. Saudi Arabia was among the first movers, introducing locally listed ETFs to provide exposure to domestic equities and specific market segments. The UAE followed closely, launching ETFs that offered access to regional equities and Sharia-compliant strategies, reflecting strong demand from both retail and institutional investors.

For many years, however, the local GCC-domiciled ETF market remained small, with a low asset base, and the primary vehicle for global investors to gain regional exposure was through US-listed funds, such as the iShares MSCI Saudi Arabia ETF, which launched in 2015.

As of October 25, there are 33 ETFs actively trading in the GCC market, including 17 in the UAE (around $337 million), 13 in Saudi Arabia (about $2.6 billion), 2 in Qatar and 1 in Egypt, With an AUM that stood at around $2.6 billion in Saudi Arabia and $337 million in the UAE.

Although, the GCC ETF market is still in its early-stage adoption phase compared to more mature markets such as Europe and the United States. The GCC ETF market is expected to maintain its robust growth, with a projected compound annual growth rate (CAGR) of 10%-12% from 2025 to 2030.