Sharia-compliant finance refers to a system of financial activity governed by Islamic law (Sharia), which sets out principles for how money can be earned, invested, and distributed. At its core, Sharia-compliant finance seeks to align financial transactions with ethical, social, and economic objectives by linking capital to real economic activity and discouraging excessive risk-taking, exploitation, and speculation.

In practice, “Sharia-compliant” does not simply mean avoiding interest. It represents a broader framework that governs how risk is shared, how assets are financed, and how returns are generated.

At core, Financial structures must be transparent, asset-backed, and tied to productive activity to ensure that the gains are earned through participation in economic value creation rather than through purely financial engineering.

While Sharia-compliant finance is rooted in Islamic principles, its relevance extends well beyond the religion of Islam. The emphasis on risk sharing, tangible assets, and ethical constraints has attracted growing interest from non-Muslim investors, regulators, and institutions seeking alternatives to highly leveraged, debt-driven financial systems. In a world increasingly focused on sustainability, financial stability, and responsible investing, Islamic finance offers a distinct and well-established framework.

For GCC investors, Sharia-compliant finance is particularly important. The region is home to some of the world’s largest Islamic financial institutions, sukuk markets, and Sharia-compliant investment vehicles. As capital markets in the GCC mature and integrate further with global finance, understanding how Sharia-compliant structures operate is no longer just niche knowledge, it became essential for navigating both local and international investment opportunities.

1. Core Principles of Sharia-Compliant Finance

Sharia-compliant finance is built on a set of foundational principles that govern what is permissible (halal) and impermissible (haram) in financial activity. These principles are designed to promote fairness, transparency, and stability by ensuring that financial transactions are rooted in real economic value and shared risk.

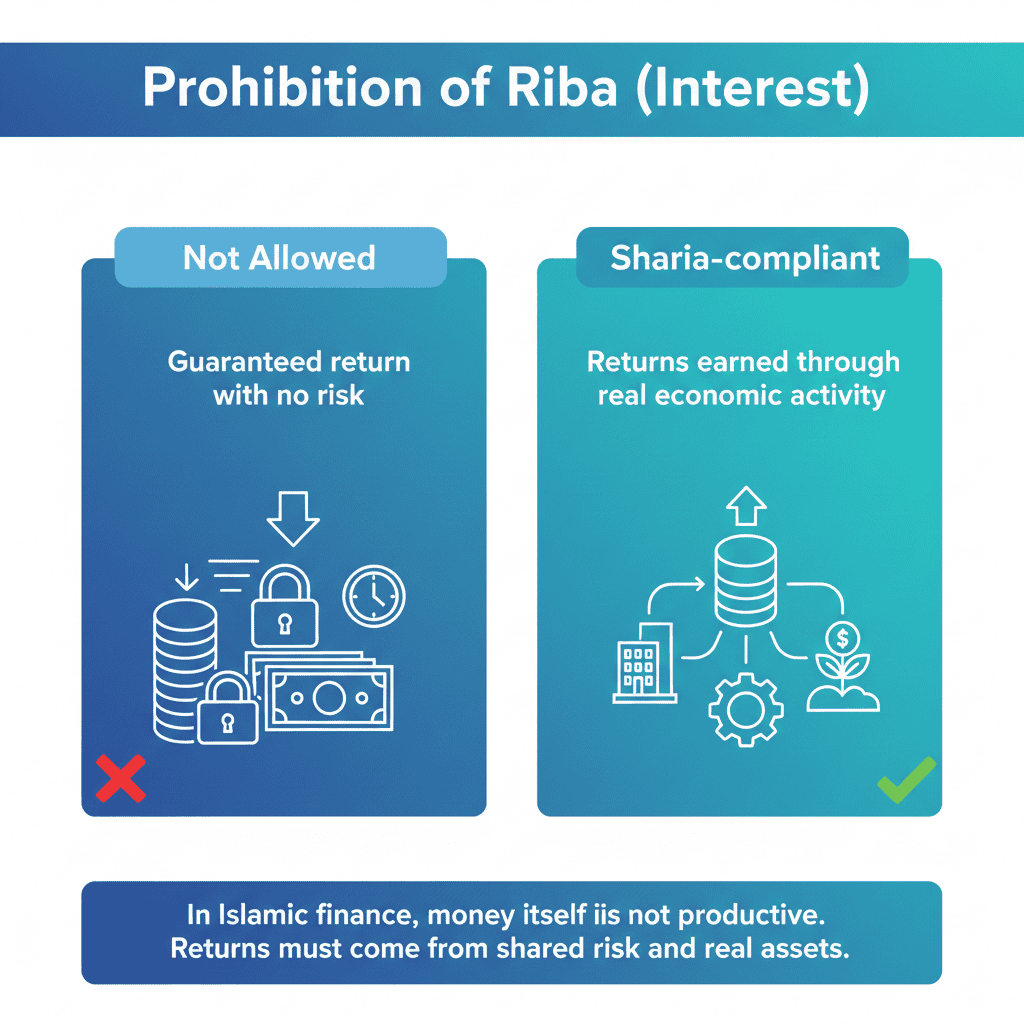

Prohibition of Riba (Interest)

The prohibition of riba, commonly understood as interest, is one of the most well-known principles of Islamic finance. Under Sharia, money itself is not considered a productive asset. It cannot generate a guaranteed return simply by being lent. Instead, returns must be earned through exposure to business risk or participation in productive activity.

This principle discourages debt-based structures where one party earns a fixed return regardless of outcome, and instead encourages financing arrangements where profits and losses are linked to the performance of an underlying asset or venture.

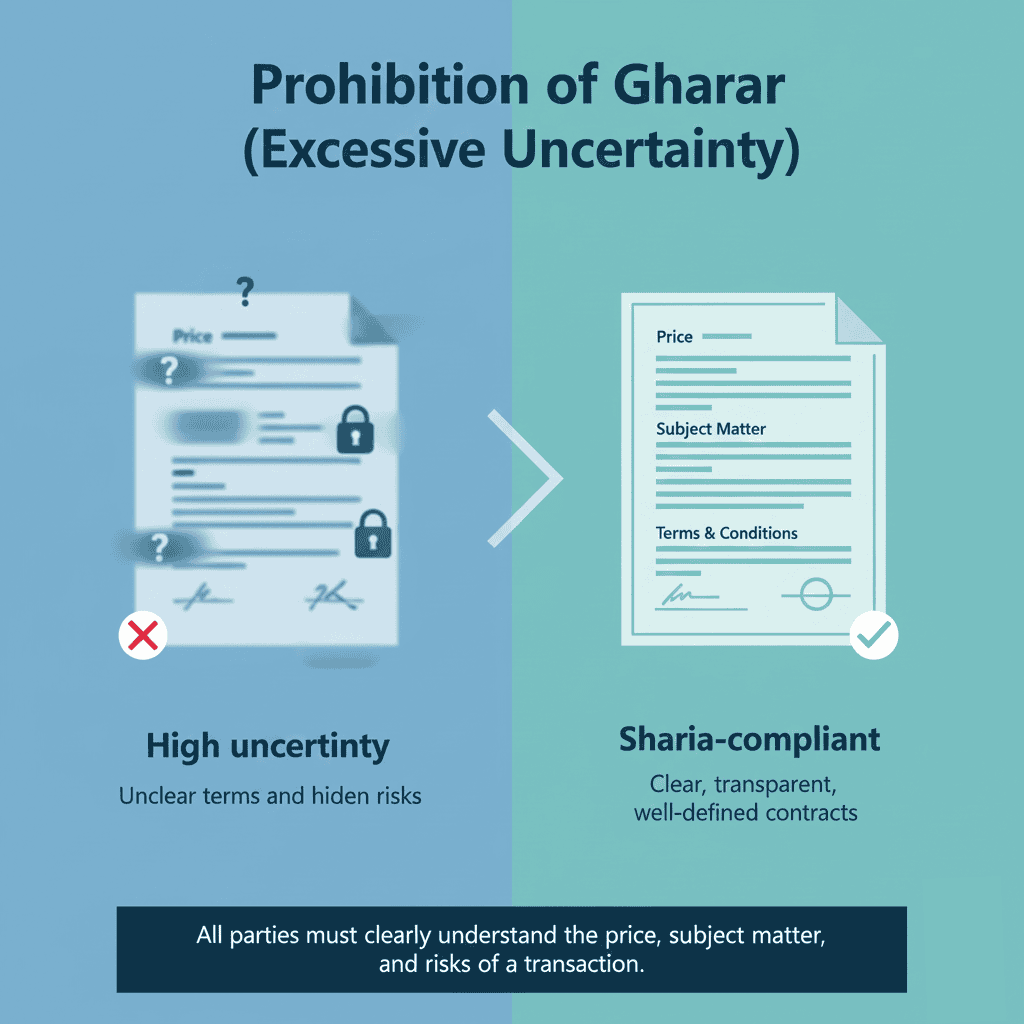

Prohibition of Gharar (Excessive Uncertainty)

Sharia-compliant finance also prohibits gharar, or excessive uncertainty. Contracts must be clear, transparent, and based on well-defined terms. The subject matter, price, delivery conditions, and risks involved in a transaction must be known to all parties.

This principle limits the use of highly complex or opaque financial instruments and promotes clarity in contractual relationships, reducing the likelihood of disputes and systemic instability.

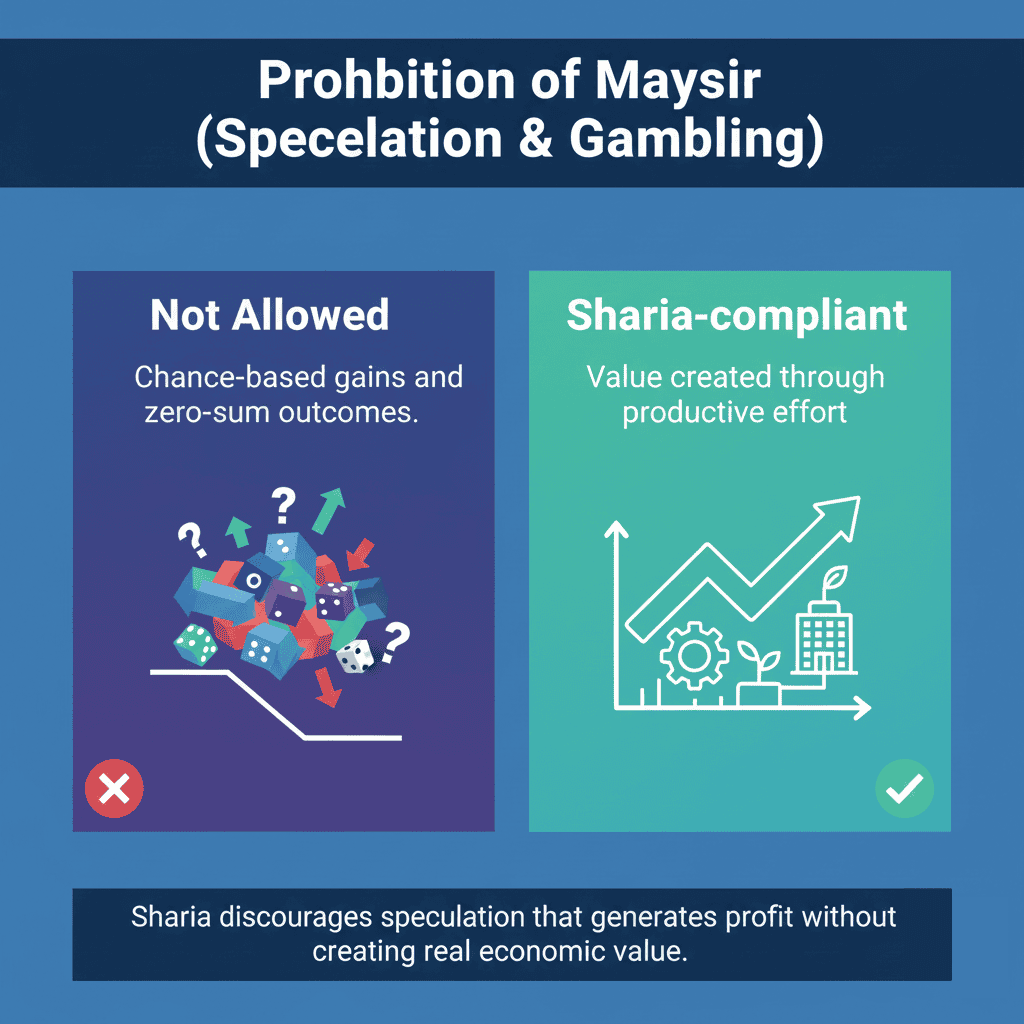

Prohibition of Maysir (Speculation and Gambling)

Maysir refers to gambling or speculative activity where gains are generated primarily through chance rather than productive effort. Sharia-compliant finance discourages transactions that resemble zero-sum bets, where one party’s gain is directly tied to another’s loss without creating real economic value.

As a result, purely speculative trading and instruments designed primarily for short-term price movements without an underlying productive purpose are generally excluded from Sharia-compliant structures.

Asset-Backing and Real Economic Activity

A defining feature of Sharia-compliant finance is the requirement that financial transactions be linked to tangible assets or genuine economic activity and that financing must be tied to goods, services, or projects that contribute to the real economy, such as property, infrastructure, trade, or productive enterprises.

This asset-backing requirement helps anchor financial activity to real-world value and limits the build-up of excessive leverage disconnected from underlying economic fundamentals.

Profit-and-Loss Sharing as a Risk-Sharing Mechanism

Rather than transferring risk entirely from one party to another, Sharia-compliant finance emphasizes risk sharing. In profit-and-loss sharing arrangements in a way that all parties involved bear exposure to outcomes in proportion to their participation.

This principle aligns incentives between investors, entrepreneurs, and financiers, encouraging more disciplined capital allocation and reducing the systemic fragility associated with guaranteed returns and excessive leverage.

2. How Islamic Finance Differs from Conventional Finance

The most effective way to understand Sharia-compliant finance is to compare it directly with conventional finance. While both systems aim to allocate capital efficiently and support economic activity, they differ fundamentally in how they treat risk, return, and the role of money itself.

Interest-Based Lending vs Asset-Backed Structures

In conventional finance, lending is typically interest-based. Capital is provided in exchange for a predetermined return, regardless of how the borrower’s underlying activity performs. Money is treated as a commodity that can generate income on its own.

Whereas in Sharia-compliant finance this framework is rejected. Capital cannot earn a guaranteed return simply through lending. Instead, financing must be structured around tangible assets, trade, or services. Returns are generated through the sale, lease, or productive use of real assets, not through the passage of time on a loan.

This distinction shifts the focus from debt creation to asset financing, anchoring financial activity more closely to the real economy.

Risk Transfer vs Risk Sharing

Conventional finance is largely built on risk transfer. Lenders seek to offload risk onto borrowers, often through collateral, covenants, or fixed repayment obligations. The lender’s return is typically insulated from the success or failure of the underlying venture.

Islamic finance operates on risk sharing. Parties involved in a transaction share exposure to outcomes, whether positive or negative. Profit-and-loss sharing arrangements require financiers to participate in both upside and downside, aligning incentives between capital providers and users of capital.

This approach promotes greater discipline in capital allocation and discourages excessive leverage, as returns are tied directly to performance rather than contractual guarantees.

Debt-Driven Finance vs Real-Economy Linkages

Conventional financial systems often expand through the creation of layered debt and financial derivatives that may have limited connection to productive economic activity. While this can increase liquidity and efficiency, it can also amplify systemic risk during periods of stress.

Sharia-compliant finance places strict emphasis on real-economy linkages. Financing must be connected to identifiable assets, services, or projects. This reduces the scope for purely financial speculation and reinforces the role of finance as a facilitator of economic activity rather than an end in itself.

For investors, this distinction matters. Sharia-compliant structures tend to exhibit lower leverage, clearer asset exposure, and risk profiles driven more by underlying economic fundamentals than by financial engineering.

Why This Difference Matters for Investors

For Muslim investors, these distinctions ensure compliance with religious principles. For non-Muslim investors, they offer an alternative financial framework that prioritizes transparency, discipline, and alignment between capital and economic value creation.

In a global environment shaped by financial crises, rising leverage, and growing scrutiny of speculative activity, the structural differences of Islamic finance are increasingly viewed not as constraints, but as risk-management features.

3. Evolution of Islamic Banking and Finance

Modern Islamic finance emerged as a response to the need for financial systems that aligned with Sharia principles while remaining compatible with contemporary economic realities. Although the underlying concepts of risk sharing and asset-backed trade date back centuries, the institutional development of Islamic finance is a relatively recent phenomenon.

The first modern Islamic commercial banks were established in the 1970s, marking a turning point for the industry. These early institutions demonstrated that banking operations could be conducted without interest while remaining commercially viable. Their success laid the groundwork for the expansion of Islamic finance beyond localized experiments into a structured and regulated financial system.

Over the following decades, Islamic banking grew rapidly, driven by rising demand in Muslim-majority countries and increasing recognition from global financial centers. Assets in the Islamic finance industry have since surpassed USD 2 trillion, positioning it as a meaningful segment of the global financial system rather than a niche alternative. Conventional banks also entered the space, offering Islamic windows or fully Sharia-compliant subsidiaries to serve growing demand.

Crucially, Islamic finance did not remain confined to retail and commercial banking. As markets matured, the industry expanded into capital markets, introducing sukuk as Sharia-compliant alternatives to conventional bonds, followed by Islamic investment funds, indices, and exchange-traded products. This shift allowed Islamic finance to scale beyond balance-sheet lending and participate more directly in global capital allocation.

Today, Islamic finance operates across banking, asset management, capital markets, and increasingly fintech. Its evolution reflects a broader transition from a banking-centric model to a diversified financial ecosystem capable of supporting institutional investors, sovereign entities, and cross-border investment flows.

4. Key Islamic Financial Structures Explained

Sharia-compliant finance operates through a set of well-defined contractual structures designed to replace conventional interest-based lending with asset-backed, risk-sharing arrangements. Understanding these structures is essential for investors, as they form the foundation of Islamic banking products, sukuk issuance, and Sharia-compliant funds and ETFs.

Rather than viewing these contracts as niche alternatives, it is more accurate to see them as financial building blocks that replicate the economic functions of conventional finance while adhering to Sharia principles.

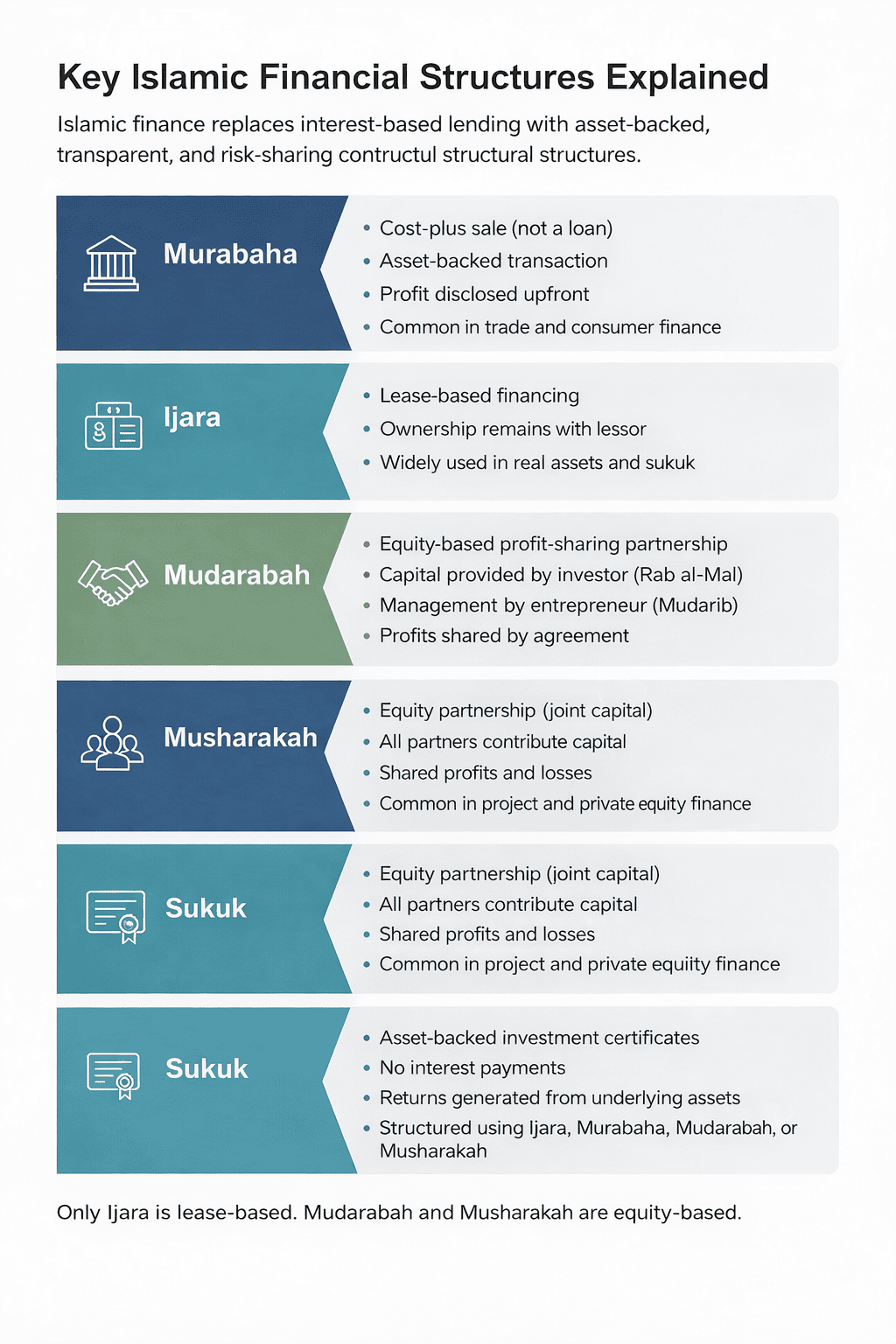

Murabaha (Cost-Plus Financing)

Murabaha is one of the most widely used structures in Islamic finance. It is a cost-plus sale rather than a loan. In a Murabaha transaction, a financial institution purchases an asset requested by a client and then sells it to the client at a pre-agreed price that includes a disclosed profit margin.

The key distinction from interest-based lending is transparency and asset ownership. The profit is fixed and known upfront, and the transaction is linked to a real asset rather than money being lent for a return. Murabaha is commonly used in trade finance, working capital solutions, and consumer financing, and it plays a significant role in Sharia-compliant banking balance sheets.

Ijara (Leasing)

Ijara is the Islamic equivalent of leasing. Under an Ijara arrangement, a financial institution acquires an asset and leases it to a client for an agreed period in exchange for rental payments. Ownership of the asset remains with the lessor, while the lessee benefits from its use.

Ijara is widely applied in real estate, infrastructure, and equipment financing. In capital markets, Ijara structures are frequently used in sukuk issuance, where investors effectively earn returns through lease payments rather than interest, maintaining Sharia compliance while offering predictable cash flows.

Mudarabah (Profit-Sharing Partnership)

Mudarabah is a profit-sharing arrangement between a capital provider and a manager or entrepreneur. One party supplies the capital, while the other provides expertise and management. Profits are shared according to a pre-agreed ratio, while losses are borne by the capital provider unless caused by negligence or misconduct.

This structure embodies the principle of risk sharing and is often used for investment accounts, asset management mandates, and certain fund structures. For investors, Mudarabah aligns returns directly with performance, reinforcing discipline in capital allocation and governance.

Musharakah (Joint Venture)

Musharakah is a partnership structure where all parties contribute capital and share profits and losses proportionally. Unlike Mudarabah, each partner participates financially and may also be involved in management.

Musharakah is commonly used in project finance, private equity-style investments, and joint ventures. It closely resembles equity participation in conventional finance and is particularly relevant for investors seeking exposure to real assets, businesses, or development projects within a Sharia-compliant framework.

Sukuk (Islamic Bonds)

Sukuk are often described as Islamic bonds, but structurally they are closer to asset-backed or asset-based certificates that represent ownership interests in underlying assets, projects, or cash flows. Returns to investors are generated through profit-sharing, lease income, or asset performance rather than interest payments.

Sukuk have become a core component of global Islamic capital markets, attracting sovereigns, corporates, and institutional investors. They are widely used for infrastructure financing, budget funding, and portfolio diversification, and they play a central role in Sharia-compliant funds and ETFs.

5. Sharia-Compliant Investing: Where Capital Markets Come In

As Islamic finance evolved beyond banking, the most significant shift occurred with its expansion into capital markets. This transition transformed Sharia-compliant finance from a primarily balance-sheet-based system into a scalable investment ecosystem capable of supporting institutional portfolios, sovereign allocations, and cross-border capital flows.

Today, Sharia-compliant investing is not limited to bespoke financing arrangements. It includes equities, indices, funds, sukuk, and exchange-traded products that allow investors to build diversified portfolios while remaining aligned with Sharia principles.

Sharia Screening of Equities

At the foundation of Sharia-compliant equity investing is a structured screening process. Companies are assessed based on two main criteria. First, business activity screens exclude sectors considered non-permissible, such as conventional banking, alcohol, gambling, and certain forms of entertainment. Second, financial ratio screens limit excessive leverage, interest income, and non-compliant receivables.

This dual screening framework results in equity universes that tend to exhibit lower leverage and cleaner balance sheets than their conventional counterparts. For investors, this introduces a distinct risk profile shaped more by operational performance and less by financial engineering.

Islamic Indices

To make Sharia-compliant investing scalable, screened equities are aggregated into Islamic indices. These indices apply standardized screening methodologies and periodic reviews, providing transparent and rules-based benchmarks for portfolio construction.

Islamic indices now exist across global, regional, and sector-specific markets, enabling investors to gain diversified exposure while maintaining Sharia compliance. They also serve as the underlying benchmarks for a growing range of funds and ETFs.

Sharia-Compliant Funds

Sharia-compliant mutual funds and investment vehicles use Islamic indices or actively managed strategies to allocate capital across permissible assets. These funds may focus on equities, sukuk, or mixed-asset portfolios and are widely used by retail and institutional investors seeking professionally managed exposure.

For many investors, Sharia-compliant funds represent the first step beyond direct asset ownership, offering diversification, governance oversight, and operational efficiency within an Islamic framework.

Sukuk Funds

Sukuk funds provide pooled exposure to Islamic fixed income instruments. Rather than earning interest, returns are generated through lease income, profit-sharing, or asset performance, depending on the sukuk structure.

Sukuk funds are particularly important for income-oriented investors and play a role similar to bond funds in conventional portfolios. They are commonly used for capital preservation, yield generation, and diversification within Sharia-compliant strategies.

ETFs as Scalable Halal Investment Vehicles

Exchange-traded funds have emerged as one of the most effective vehicles for scaling Sharia-compliant investing. Sharia-compliant ETFs combine rules-based screening, intraday liquidity, and low-cost access into a single structure.

These ETFs track Islamic indices across equities or sukuk markets, allowing investors to gain diversified halal exposure through a single, transparent instrument. For GCC investors, Sharia-compliant ETFs bridge traditional Islamic finance principles with modern portfolio construction, enabling efficient allocation alongside conventional ETFs and global assets.

This development marks a critical inflection point: Sharia-compliant investing is no longer limited by geography, product availability, or operational complexity. It has become fully compatible with institutional asset allocation frameworks and global investment strategies.

6. Regulation, Governance & Sharia Oversight

A defining strength of modern Sharia-compliant finance is the governance framework that underpins it. Contrary to the perception that Sharia compliance is interpretive or informal, the industry operates under structured oversight mechanisms designed to ensure consistency, transparency, and investor protection.

At the core of this framework are Sharia boards, financial regulators, and international standard-setting bodies, which together provide multilayered supervision of Islamic financial activities.

Role of Sharia Boards

Every Sharia-compliant financial institution or product is overseen by an independent Sharia board composed of qualified Islamic scholars with expertise in finance and jurisprudence. These boards are responsible for reviewing product structures, contractual documentation, and ongoing operations to ensure compliance with Sharia principles.

Importantly, Sharia oversight is not a one-time approval. Products and portfolios are reviewed continuously, and any income derived from non-compliant activities must be identified and purified according to established guidelines. This ongoing supervision provides investors with confidence that compliance is actively maintained rather than assumed.

Role of Financial Regulators

In addition to Sharia supervision, Islamic financial institutions are subject to the same prudential and market regulations as their conventional counterparts. Banking regulators, securities authorities, and exchange supervisors oversee capital adequacy, risk management, disclosure standards, and investor protection.

In the GCC, regulatory frameworks for Islamic finance are deeply integrated into national financial systems. This dual-layer oversight (religious and regulatory) distinguishes Sharia-compliant finance from informal ethical investing approaches and reinforces its institutional legitimacy.

Islamic Financial Services Board (IFSB)

At the international level, the Islamic Financial Services Board (IFSB) plays a central role in setting global standards for Islamic finance. The IFSB issues guidelines covering capital adequacy, risk management, governance, and supervisory review, tailored specifically to the unique features of Sharia-compliant institutions.

These standards help harmonize practices across jurisdictions, making it easier for investors to compare products and for institutions to operate across borders. For global and institutional investors, the presence of internationally recognized standards reduces fragmentation and enhances confidence in the industry’s stability.

Why Governance Matters for Investors

Strong governance is not merely a compliance exercise; it is fundamental to investor trust. Clear oversight mechanisms reduce ambiguity, limit operational risk, and ensure that Sharia-compliant products behave as expected under different market conditions.

For investors, Muslim and non-Muslim alike, this governance framework transforms Sharia-compliant finance from a values-based concept into a credible, regulated investment ecosystem that can operate alongside conventional markets without compromising transparency or discipline.

7. The Islamic Finance Industry Today

The Islamic finance industry has matured into a globally relevant segment of the financial system, with total assets now exceeding USD 2 trillion and continuing to grow at a steady pace. What began as a niche response to religious requirements has evolved into a diversified ecosystem encompassing banking, capital markets, asset management, and increasingly, technology-driven financial services.

Market Size and Growth

Growth in Islamic finance has been driven by a combination of demographic demand, regulatory support, and rising interest in ethical and risk-disciplined financial models. While banking remains the largest component by assets, capital markets activity particularly sukuk issuance and Sharia-compliant funds has expanded rapidly, reflecting investor demand for scalable and liquid investment products.

This shift toward market-based instruments has allowed Islamic finance to move beyond localized banking relationships and participate more directly in global capital flows.

Geographic Hubs: GCC, Malaysia, and the UK

The GCC remains the largest and most influential hub for Islamic finance, anchored by deep sukuk markets, sovereign participation, and a growing universe of Sharia-compliant investment products. Malaysia plays a complementary role, particularly in standard-setting, product innovation, and Islamic capital markets infrastructure. The UK has emerged as a key Western hub, facilitating cross-border issuance, asset management, and international investor access.

Together, these hubs have helped integrate Islamic finance into the global financial system rather than positioning it as a parallel or isolated market.

Integration with Global Finance

Islamic finance is increasingly intertwined with conventional markets. Many global banks offer Islamic windows or Sharia-compliant products, while international investors participate actively in sukuk and Islamic fund markets. This integration has improved liquidity, transparency, and standardization, making Sharia-compliant investments more accessible to a broader investor base.

Innovation: ETFs, Fintech, and Tokenization

Innovation is reshaping the industry. Sharia-compliant ETFs have expanded access to halal investing through transparent, low-cost structures. Fintech platforms are improving distribution and accessibility, while tokenization and digital infrastructure are being explored as ways to enhance settlement efficiency and broaden participation.

These developments signal a shift from traditional banking-led growth toward a more diversified, technology-enabled Islamic finance ecosystem.

8. Abu Dhabi & the GCC as a Global Hub for Islamic Finance

Within the global Islamic finance landscape, Abu Dhabi and the wider GCC occupy a uniquely strategic position. The region combines regulatory credibility, sovereign participation, and capital-market depth, making it one of the most important centers for Sharia-compliant finance worldwide.

Abu Dhabi’s Positioning

Abu Dhabi has positioned itself as a regional and international hub for Islamic finance by aligning regulatory frameworks with global standards while supporting product innovation. The emirate benefits from strong sovereign backing, institutional capital, and a long-standing role in sukuk issuance and Islamic banking.

Regulatory Environment

The UAE’s regulatory approach emphasizes transparency, investor protection, and market integrity. Sharia-compliant products operate within the same robust supervisory frameworks as conventional financial instruments, reinforcing confidence among both regional and international investors.

This regulatory clarity is particularly important as Islamic finance products increasingly target institutional portfolios and cross-border capital flows.

ADX, Sukuk Listings, and Sharia ETFs

The Abu Dhabi Securities Exchange plays a central role in this ecosystem. Abu Dhabi Securities Exchange hosts a growing range of sukuk listings, Islamic indices, and Sharia-compliant ETFs, providing investors with exchange-listed access to halal investment strategies.

The expansion of these products reflects a broader shift toward capital-market-based Islamic finance, enabling liquidity, price discovery, and portfolio integration alongside conventional assets.

Why the GCC Matters Globally

The GCC’s importance extends beyond regional demand. As global investors seek exposure to ethical finance, emerging-market growth, and income-generating assets, Sharia-compliant instruments issued in the GCC increasingly serve as a gateway to these themes.

With deep pools of capital, supportive regulation, and growing product diversity, the GCC led by Abu Dhabi has become a cornerstone of the modern Islamic finance ecosystem.

Why Sharia-Compliant Finance Matters for Modern Investors

Sharia-compliant finance has evolved far beyond its origins as a niche alternative to conventional banking. Today, it represents a mature and globally integrated financial framework that combines ethical principles with disciplined risk management and real-economy alignment. For investors, this evolution matters not because of its religious foundations alone, but because of the structural characteristics it promotes: transparency, asset backing, and shared risk.

For Muslim investors, Sharia-compliant finance provides a clear and credible pathway to participate in global capital markets without compromising faith-based principles. For non-Muslim investors, it offers exposure to a financial system that prioritizes balance-sheet discipline, limits excessive leverage, and anchors returns to productive economic activity rather than financial engineering.

In the GCC, the relevance of Sharia-compliant finance is particularly pronounced. The region sits at the intersection of sovereign capital, deep sukuk markets, and increasingly sophisticated exchanges offering Sharia-compliant funds and ETFs. As Islamic finance continues to integrate with global markets, it is no longer confined to bespoke structures or local institutions; it is accessible, scalable, and compatible with modern portfolio frameworks.

The growing availability of Sharia-compliant equities, sukuk funds, and exchange-traded products marks a turning point. Investors can now build diversified, liquid portfolios that align ethical considerations with performance objectives, risk management, and long-term capital allocation.

As global finance grapples with sustainability, leverage, and systemic risk, Sharia-compliant finance stands out not as an alternative system, but as a complementary one. Understanding how it works is no longer optional for investors operating in the GCC or engaging with global markets. It is a foundation for informed decision-making in an increasingly complex investment landscape.