The GCC reached a major ETF milestone on December 10, 2025, when the first U.S. cross-listed ETFs began trading on the Abu Dhabi Securities Exchange (ADX). Two globally recognized ETFs, KWEB and KRBN made their debut in Abu Dhabi, allowing investors to trade them during local market hours and in UAE dirhams.

This milestone was years in the making, requiring regulatory reforms, new market infrastructure, and close collaboration across the ecosystem. ADX established the operational link between the U.S. DTCC and the Abu Dhabi Central Securities Depository (ADCSD), enabling the seamless transfer of ETF shares between the two markets. An efficient institutional FX process was also introduced, while Oceane Global became the region's first ETF-focused market maker, providing continuous liquidity and facilitating efficient ETF pricing, creations, and redemptions across borders.

The launch marked a turning point for GCC capital markets, giving global asset managers a practical pathway to list ETFs on a regional exchange and significantly expanding investment options for local investors. KraneShares was the first international issuer to seize the opportunity, adding KWIN and AGIX in April 2026 after the initial cross-listings of KWEB and KRBN.

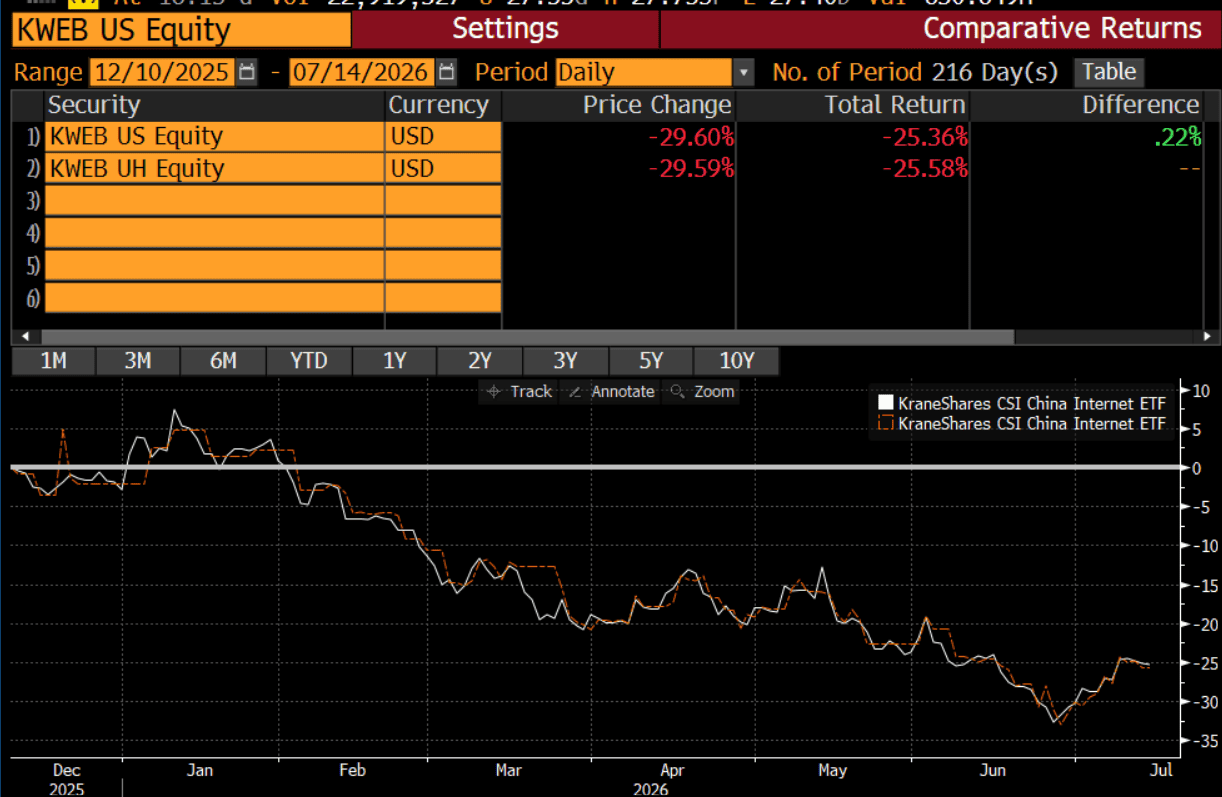

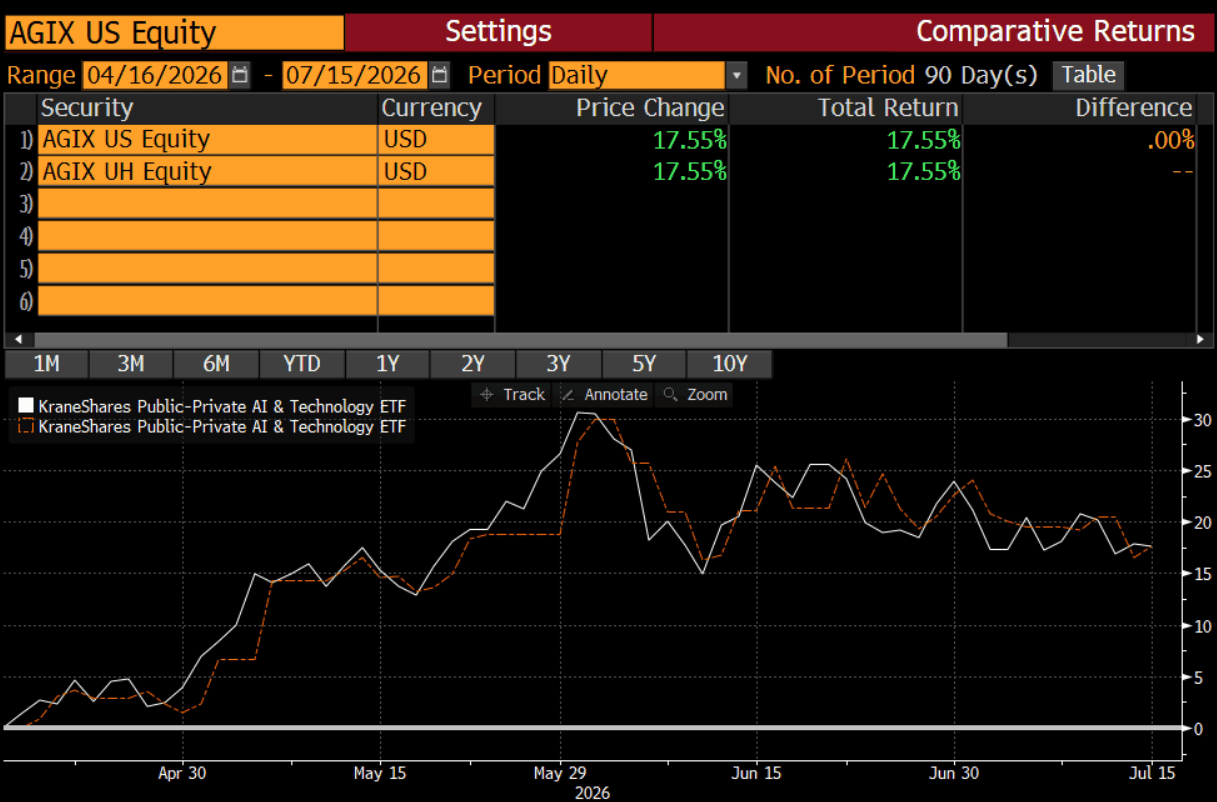

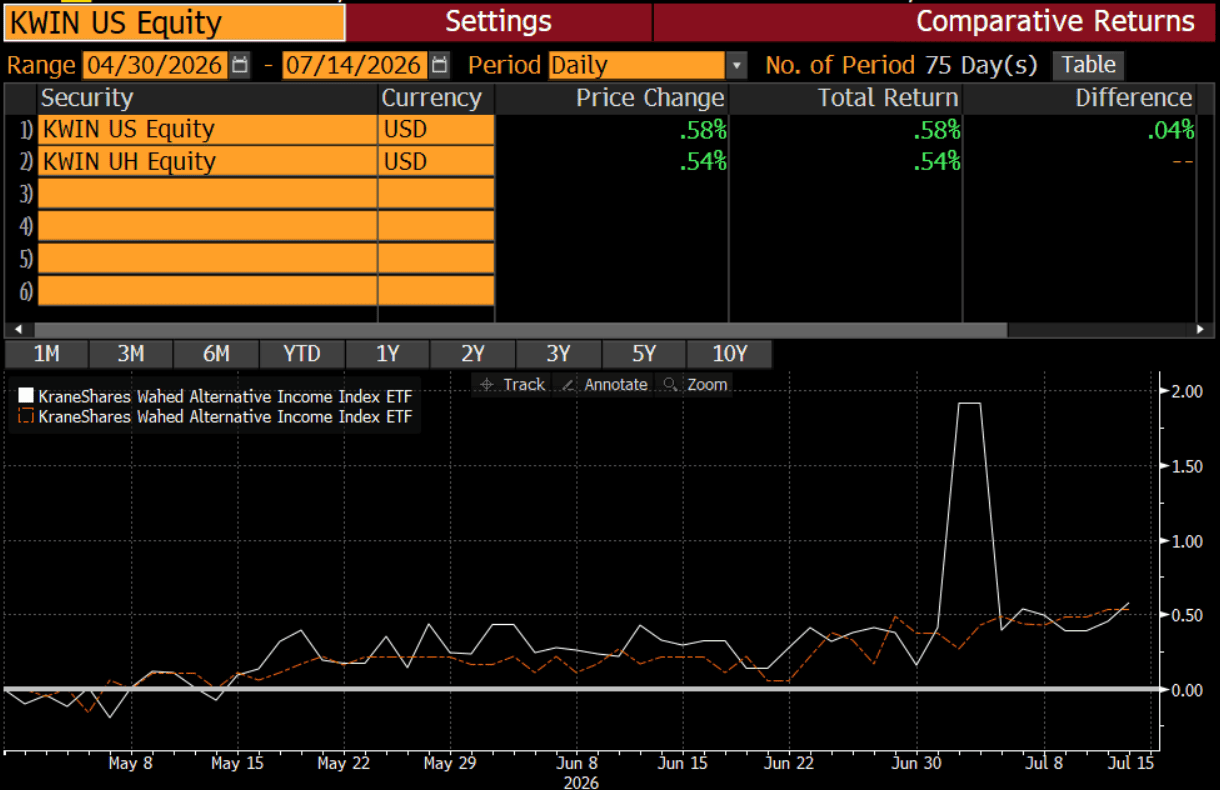

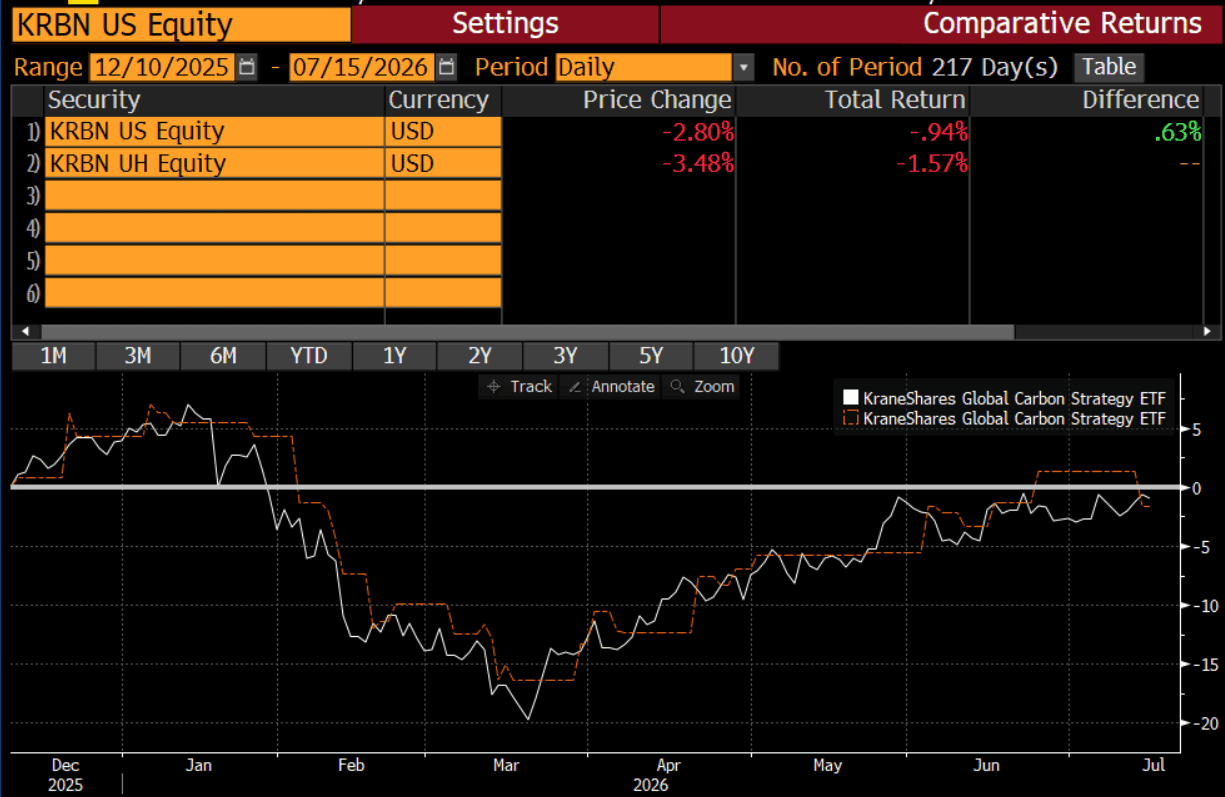

The four ETFs introduced unique exposures to the GCC: KWEB, the world's largest China internet ETF; KRBN, the region's first compliance carbon credit ETF; AGIX, the GCC's first actively managed AI ETF with public and private company exposure; and KWIN, the region's first Shariah-compliant option income ETF.

Why does it matter?

ETF cross-listing is designed to give both retail and institutional investors in the GCC direct access to globally recognized ETFs through their local exchange. Today, regional institutional investors allocate hundreds of billions of dollars to ETFs listed overseas, attracted by their broad market access and deep liquidity. For global asset managers, however, it is equally important that the local market infrastructure delivers an investment experience that meets international standards.

One of the clearest measures of success is how closely ADX cross-listed ETFs track the performance of their primary listings abroad. Total return captures all the key factors that influence investor outcomes, including time zone differences, foreign exchange conversions from USD and AED, and trading spreads. So, how have ADX's cross-listed ETFs performed relative to their parent funds?

Do ADX Cross-Listed ETFs Match Their U.S. Listings?

The performance of the ADX cross-listed ETFs has closely mirrored that of their primary listings on the New York Stock Exchange (NYSE), demonstrating that the cross-listing framework is functioning as intended. The charts below compare cumulative price returns since each ETF's ADX listing. Performance differences have been negligible, with KWEB at 22 bps, AGIX at 0.0%, KWIN at 4 bps, while KRBN tracking is 0.63 bps.

While the performance lines move almost in lockstep, they do not overlap perfectly because the two exchanges close at different times 3:00 p.m. in Abu Dhabi versus 4:00 p.m. in New York. Price movements that occur after the ADX close are reflected in the U.S. listing first and incorporated into the ADX price on the next trading day.

Importantly, there is only one official Net Asset Value (NAV) for each ETF, calculated in the United States. There is no separate NAV for the ADX listing, meaning both securities represent the same underlying portfolio and investment strategy.

This is Good News for Investors and Global Asset Managers

The results suggest that investors should be largely indifferent from a return perspective when choosing between the ADX and NYSE listings. The key advantages of the ADX listing lie instead in the operational experience: trading during GCC market hours, local settlement infrastructure, execution in UAE dirhams, and potentially fewer administrative and tax complexities associated with investing directly through overseas markets. These findings validate ADX's cross-listing model as an effective way to provide GCC investors with local access to global ETFs without compromising investment performance.

This development is likely to attract global asset managers, particularly those with an established presence in the GCC. By enabling ETFs to be listed directly on local exchanges and traded in local currency, issuers can improve accessibility, strengthen their regional footprint, and drive broader investor participation, particularly among retail investors.