For investors in the GCC, the distinction between cross-listed ETFs and locally listed ETFs relates primarily to market access, trading mechanics, and market structure, rather than differences in investment exposure. In most cases, the underlying portfolio, investment strategy, and risk-return characteristics are identical to those of the ETF listed in its home market, such as the United States or under UCITS frameworks in Europe.

Cross-listing, also referred to as dual listing, is a widely used global practice that allows established international ETFs to be traded on local exchanges. Through this process, investors can access the same investment exposure and economic benefits while trading on their domestic exchange and in local currency.

Compared to alternative structures such as feeder funds, cross-listing is generally more efficient and transparent. It also enhances regulatory oversight by enabling local regulators, such as the Securities and Commodities Authority (SCA), to better protect investors within their jurisdiction.

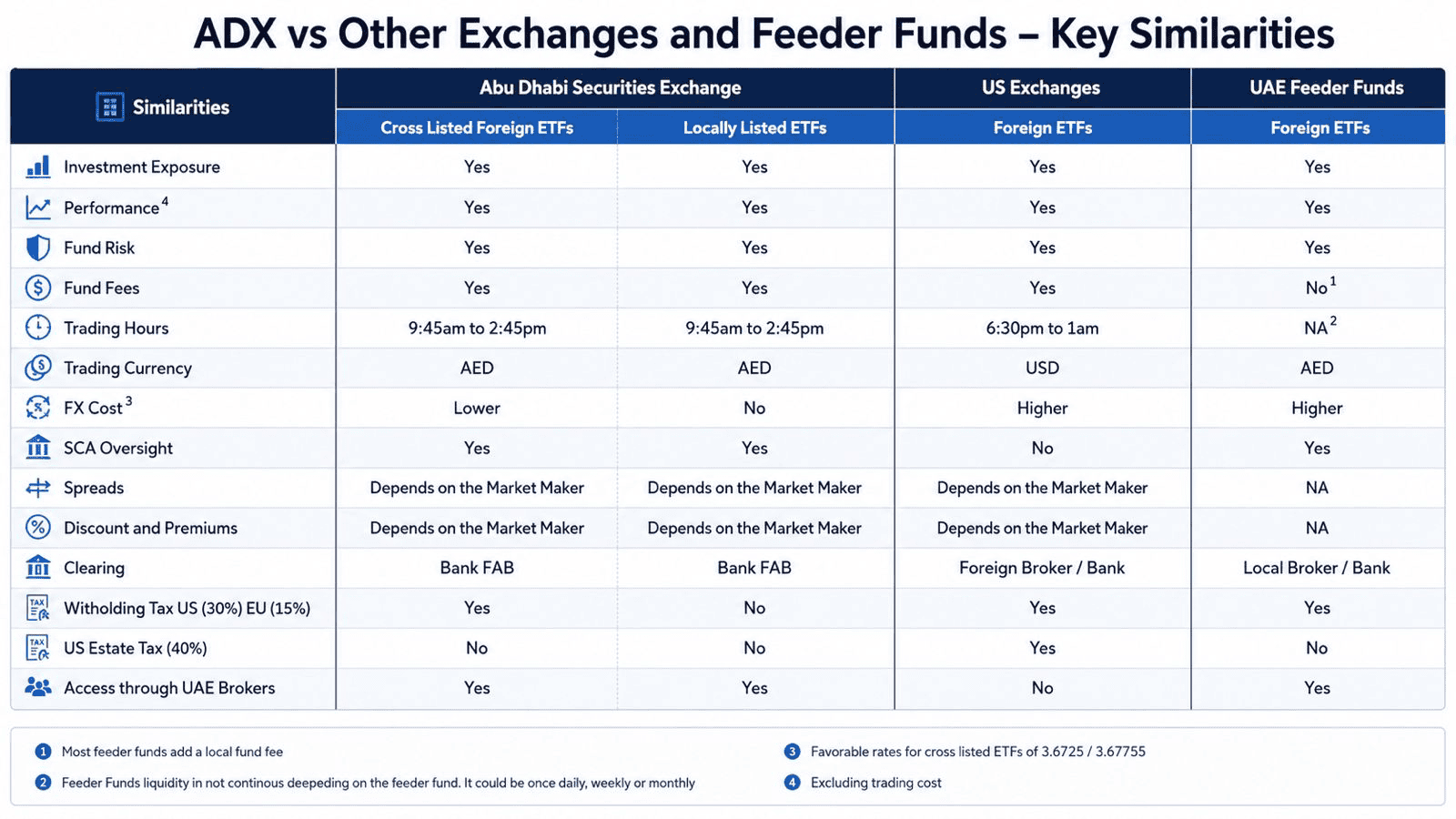

Similarities between ADX Local ETFs and Cross listed ETFs, US listed ETFs and Feeder Funds

The ETF Market Maker behind the cross listings of the four ETFs from the NYSE to ADX is Océane Invest

What Is the Same for Investors

From an economic standpoint, investors receive identical exposure whether they invest in the original overseas ETF or its GCC-listed equivalent. This includes:

· The same underlying assets and index or strategy

· The same global portfolio manager

· The same performance, before local trading costs

In other words, the investment outcome is driven by the global portfolio, not the exchange on which the ETF is traded.

How Cross-Listed Shares Are Settled on Abu Dhabi Securities Exchange (ADX)

The Abu Dhabi Securities Exchange (ADX) has established a solid framework that enables securities listed on major international exchanges, such as those in the United States and Europe to be traded and held locally in Abu Dhabi.

Under this framework, ADX’s central securities depository (ADX CSD) maintains the necessary custody and settlement arrangements with international clearing systems. When an investor places a trade on ADX, the designated market maker sources the shares from the home market (for example, the United States). These shares are then delivered through the international clearing infrastructure and registered with ADX CSD.

Once registered locally, the shares are credited to the investor’s account in Abu Dhabi and can be traded on ADX like any other locally listed security. Through this regulated process, and under the oversight of ADX CSD, shares can move efficiently between the home exchange and ADX, ensuring full alignment between the original listing venue and the cross-listed market.

Creation, Redemption, and Settlement of Cross-Listed ETF Units

While the investment exposure and economic outcomes for investors are identical, the operational process for creating, redeeming, and delivering ETF units differs between the home market and the local exchange.

ETF creation and redemption take place in the fund’s home market. When an investor submits an order locally on Abu Dhabi Securities Exchange (ADX), the appointed market maker executes the corresponding transaction in the home market, such as the United States. The ETF units are then transferred through ADX’s cross-border settlement framework and delivered to UAE investors.

This process is designed by ADX to ensure timely and efficient settlement, with delivery completed in accordance with local market requirements, including the standard T+2 settlement cycle.

Key Differences That Matter in the GCC

1. Market Access and Convenience - More control in trading

Cross-listed ETFs allow GCC investors to access established global ETFs directly through local exchanges such as ADX, Tadawul, DFM, and other regional venues. This removes the need for offshore brokerage accounts, foreign custody arrangements, or complex onboarding processes. GCC investors can now trade leading globally listed ETFs in GCC timezone rather than waiting for global exchanges like London or New York to open so they can book trades. This provides retail and institutional investors with more control over portfolios and risk.

2. Currency and Settlement - Lower Currency Cost

Both cross-listed and locally listed ETFs trade and settle in local currency through domestic clearing systems, eliminating the need for investors to manage foreign exchange transactions directly. Any currency exposure is embedded within the ETF itself rather than handled at the account level.

For cross-listed ETFs traded on Abu Dhabi Securities Exchange (ADX), currency conversion is facilitated through arrangements with First Abu Dhabi Bank (FAB). This allows trades to be settled at favorable FX rates of USD 3.6725 (sell) and USD 3.6775 (buy), significantly reducing currency conversion costs compared to standard bank or broker FX charges.

3. Liquidity and Trading Quality - More efficient execution

Cross-listed ETFs benefit from global liquidity in the primary market as creation and redemption happen at the home listing and it is supported locally by professional market makers like Oceane Invest, which was created for the purpose of providing local investors with the highest ETF liquidity services to lower transaction cost and encourage local ETF adoption. Prices are kept in line with the original listing through arbitrage, helping ensure tight spreads and efficient execution.

4. Fees and Costs - Same fund fees

Cross-listed ETFs typically carry the same expense ratio as their original overseas listing, with no additional management layer. Total investor cost is therefore driven mainly by local trading spreads and commissions. Locally listed ETFs may have higher or lower fees depending on fund size, structure, and scale.

5. Regulatory Framework - More Local Investor Protection

In 2023, the Emirates Securities and Commodities Authority (SCA) introduced new regulations governing the offering of foreign-listed investment funds in the UAE.

Prior to these changes, global asset managers could register foreign funds with the SCA, allowing local banks and wealth managers to invest in them without significant restrictions, including for retail investors. However, this structure provided the regulator with limited oversight and fewer mechanisms to protect local investors in situations such as missed dividend payments, corporate actions, or regulatory breaches.

Under the revised framework, funds offered locally are generally required to be domiciled in the UAE. Where this is not the case, higher minimum investment thresholds apply, including a minimum allocation of AED 500,000 per exchange-traded fund (ETF).

Cross-listing addresses these challenges by bringing foreign funds onto a UAE-regulated exchange, enhancing regulatory oversight and providing stronger protections for both the SCA and local investors.

6. Tax Considerations

Cross-listing does not fully eliminate foreign tax exposure for GCC investors; however, it can reduce certain tax-related risks compared to investing directly in ETFs listed abroad.

For U.S.-domiciled ETFs, investors are generally subject to two types of taxes: withholding tax on income distributions and U.S. estate tax. GCC investors remain subject to U.S. withholding tax on income distributions, currently applied to dividends only and not to capital gains. However, cross-listed ETFs remove exposure to U.S. estate tax, which may otherwise apply at rates of up to 40% in the event of death.

For EU-domiciled (UCITS) ETFs, GCC investors are generally subject to withholding tax on income distributions, typically at a rate of approximately 15%, with no withholding applied to capital gains.

Tax treatment may vary based on individual circumstances, fund structure, and applicable regulations, and investors should seek professional tax advice where appropriate.

Bottom Line for GCC Investors

For GCC investors, cross-listing is about access rather than compromise. It enables participation in large, liquid, globally proven ETFs through familiar local exchanges and infrastructure. Cross-listed ETFs act as a bridge, accelerating ETF adoption while locally listed products continue to develop alongside them.