In 2025, State Street and Apollo rolled out a pioneering daily-dealing ETF (PRIV) that mixes public investment-grade bonds with directly sourced private loans; BondBloxx launched PCMM, an ETF that buys tranches of private-credit CLOs; and several issuers debuted “private-equity replication” ETFs that try to mimic buyout/VC returns using liquid public equities.

For UAE and GCC investors who typically access markets via UCITS (European “Undertakings for Collective Investment in Transferable Securities”) ETFs, the expanding menu creates opportunity alongside tax wrinkles and hard questions about liquidity and valuation.

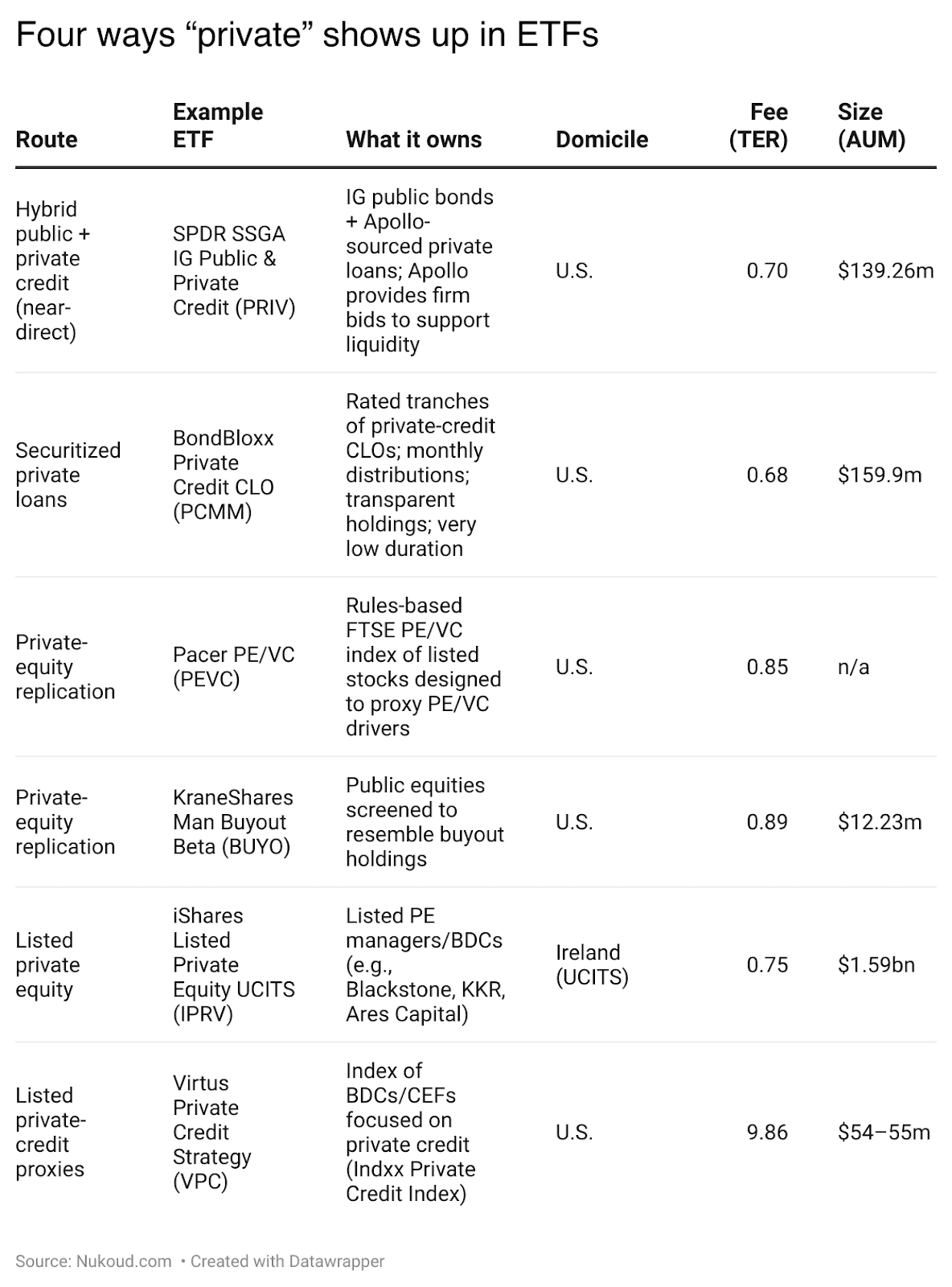

“Private assets in ETFs” really means three routes:

(1) near-direct exposure to private credit inside a ’40-Act ETF

(2) securitized exposure via instruments backed by private loans (e.g., private-credit CLOs)

(3) public-market proxies, either factor portfolios that aim to capture private-equity “beta” or long-standing funds holding listed private-asset managers and BDCs. Each path trades off purity of exposure versus daily liquidity, fees, tracking error, and (for GCC investors) domicile-driven tax treatment.

What’s driving this now?

Private credit has scaled rapidly: credible estimates put global AUM around $1.6–$1.7 trillion in 2024–2025, with forecasts between $2.6–$3.0 trillion later this decade.The growth tailwinds are tighter bank lending and institutional demand for higher, less-correlated income. Data and transparency are improving, too.

For example, Kroll and StepStone launched private-credit benchmarks in September 2025 to standardize performance tracking.

On the regulatory side, two U.S. rules matter most for any ETF touching private assets: SEC Rule 2a-5 (effective 2022) standardizes fair-value practices and board oversight for hard-to-price assets; Rule 22e-4 mandates liquidity risk programs, portfolio liquidity classifications, and a 15% illiquid investment limit at acquisition. These guardrails shape how far ETFs can push into illiquid markets while honoring daily creations/redemptions.

In UCITS, the bar is higher for illiquid assets. A UCITS can hold up to 10% in instruments that don’t meet standard eligibility (the so-called “trash bucket”), and direct loans are not an eligible asset under current interpretations (e.g., Luxembourg CSSF). That’s why “true” private-credit UCITS ETFs remain unlikely today; UCITS exposure tends to be via listed private-equity proxies or securitized instruments.

AUM = assets under management; TER = total expense ratio; AFFE = acquired fund fees & expenses; “30-Day SEC Yield” is the standardized U.S. yield metric.

How these structures actually work

Private-asset ETFs use different frameworks to deliver exposure inside a daily-dealing wrapper. PRIV combines an investment-grade bond core with privately sourced loans from Apollo affiliates; Apollo commits to firm bids on certain private positions to help support creations/redemptions but the portfolio still sits under Rule 22e-4 classifications and the 15% illiquid-at-acquisition cap.

PCMM accesses private credit through CLO tranches backed largely by middle-market/private loans, providing daily NAVs, position-level transparency, and very low duration. Replication ETFs like PEVC/BUYO don’t touch private assets; instead they target public-equity characteristics correlated with PE/VC outcomes liquid and transparent, but with expected tracking error versus actual buyout funds.

“Listed private asset” ETFs such as IPRV and VPC own the operators (PE managers, BDCs, CEFs), not the underlying deals, and fees can look elevated where AFFE applies.

The regulatory architecture

-U.S. ’40-Act ETFs: Rule 2a-5 governs fair-value determination and board oversight; Rule 22e-4 mandates liquidity programs, monthly (or more frequent) liquidity classification, and a 15% illiquid investment limit at acquisition. These apply to ETFs like PRIV and PCMM.

-UCITS (EU/UK): Loans are not a directly eligible asset for UCITS (e.g., CSSF guidance). UCITS can hold up to 10% in non-standard eligible assets (“trash bucket”), which constrains direct private-credit implementations and pushes UCITS toward listed proxies or securitized formats.

Risks and considerations

Liquidity mismatch remains the core challenge,

Even with Apollo’s firm bids and ETF creation/redemption, privately sourced loans are hard to exit quickly without price concessions. In stress, secondary-market discounts and wider ETF spreads are possible; Rule 22e-4 is a guardrail, not a guarantee.

Valuations are inherently model-driven like Rule 2a-5 requires a documented, board-overseen fair-value process, yet NAVs can look smooth between periodic re-sets. Replication funds are not private equity; they will diverge sometimes sharply during exit cycles or post-deal value creation because they own listed equities, not controlled private companies. Fees vary, and AFFE can inflate headline expense ratios when ETFs hold other funds (e.g., VPC).

Finally, on a Sharia screen, conventional private-credit strategies typically involve riba (interest) and are unlikely to pass; listed PE managers may also fail screens given leverage and revenue mix Sharia-compliant ETF choices in this niche remain limited.

Takeaways for GCC/UAE Investors

For GCC and UAE investors, private-asset ETFs represent a new frontier but one that requires discernment. While U.S.-domiciled funds such as PRIV and PCMM now offer genuine exposure to private loans and securitized credit, most UCITS vehicles (the default choice for regional platforms) remain limited to listed private-equity managers or replication strategies like IPRV, reflecting strict European eligibility rules.

This makes it essential to look past the label: “private” in an ETF might mean direct loans, CLO tranches, or public-equity proxies, each of which can behave very differently when markets come under pressure.

Finally, investors must prepare for liquidity and valuation surprises, regulatory caps and fair-value rules exist precisely because private assets do not trade with the same immediacy as public securities.

In short, private-asset ETFs broaden access but also shift risks into the wrapper; navigating them well will depend on a clear-eyed view of what’s inside, how it trades, and where it’s domiciled.