Access to Shariah-compliant U.S. equities has become significantly easier for GCC investors. Instead of relying solely on international brokerage accounts, investors can now choose between a locally listed ETF on the Abu Dhabi Securities Exchange (ADX) and one of the largest U.S.-listed Shariah equity ETFs. USGRWTH, the Lunate S&P US Shariah Growth ETF, provides direct access through ADX, while SPUS, the SP Funds S&P 500 Sharia Industry Exclusions ETF, manages more than US$ 2,066.86 million in assets and has been trading on the NYSE since 2019.

Although both ETFs provide exposure to U.S. large-cap Shariah-compliant equities and share many of the same technology leaders, they are designed for different investor priorities. USGRWTH offers GCC investors a convenient way to access the U.S. market through a locally listed ETF on ADX, with automatic dividend reinvestment and without requiring an international brokerage account. SPUS, by contrast, combines a multi-billion-dollar asset base, deep trading liquidity, and more than six years of operating history, making it well-suited to investors who prioritise scale, trading efficiency, and an established performance track record.

Although the two funds differ in areas such as liquidity, market access, trading currency, and tax treatment, the key differentiator for many investors is likely to be their level of exposure to the Magnificent Seven (Mag 7)

Overview of USGRWTH

USGRWTH is domiciled in the UAE under the Lunate Umbrella Fund structure, regulated under the CMA Umbrella framework, and managed by Lunate Capital LLC. It benchmarks the S&P 500 U.S. Shariah Top 30 35/20 Capped Index (US$), using full physical replication with in-kind basket settlement. Listed on 1 July 2022, it reinvests dividends on an accumulating (Acc) basis and carries a 0.45% total expense ratio, trading in AED on ADX.

As of 31 March 2026, Lunate reports the fund as holding 100 securities, with an underlying index market capitalisation of US$ 32,330.88 billion, a weighted average P/E of 42.28, P/B of 17.77, and ROE of 63.87%. Assets under management stood at approximately US$ 6.28 million, reflecting its early stage of asset growth.

For GCC investors, USGRWTH removes many of the practical barriers associated with investing internationally. By listing on ADX, the fund enables investors to access a portfolio of leading U.S. Shariah-compliant companies through familiar regional market infrastructure while benefiting from an accumulating structure that automatically reinvests dividends for long-term capital growth.

Overview of SPUS

SPUS is one of the largest and longest-established U.S.-listed Shariah equity ETFs, launched on 17 December 2019 and trading on the NYSE in US dollars. It tracks the S&P 500 Shariah Industry Exclusions Index, a related but distinct benchmark from USGRWTH, and distributes dividends rather than reinvesting them. As of 30 June 2026, the fund had net assets of US$2,066.86 million, 42,525,000 shares outstanding, an NAV of US$48.60, and a market price of US$48.64, representing a 0.08% premium to NAV. Like USGRWTH, it carries a 0.45% total expense ratio (TER) and offers a 30-day SEC yield of 0.43%. Its 0.02% median 30-day bid-ask spread reflects deep trading liquidity supported by more than six years of operating history and a multi-billion-dollar asset base.

SPUS's larger asset base and longer operating history also make it attractive for institutional investors and larger portfolios, where trading efficiency, liquidity, and established market depth are particularly important.

Fund Characteristics

*During U.S. Daylight Saving Time (EDT). During U.S. Standard Time (EST), regular NYSE trading hours are approximately 6:30 PM–1:00 AM GST.

Magnificent Seven: The Deciding Factor?

An investor's outlook on the Magnificent Seven (Mag 7) could be one of the most important factors when deciding between these two ETFs.

For much of the past decade, the Mag 7, which includes Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla, has dominated global equity market returns and investor attention. More recently, enthusiasm has shifted toward the broader artificial intelligence ecosystem, although many of these companies remain at the centre of that theme. Microsoft, Alphabet, and Amazon, for example, operate some of the world's largest cloud platforms and AI infrastructure, while Nvidia continues to power much of the industry's computing demand.

Performance, however, has become more mixed in 2026. Investors have begun scrutinizing the enormous capital expenditure required to build AI infrastructure, raising questions about when these investments will translate into sustainable earnings growth. As a result, returns among the Mag 7 have diverged significantly.

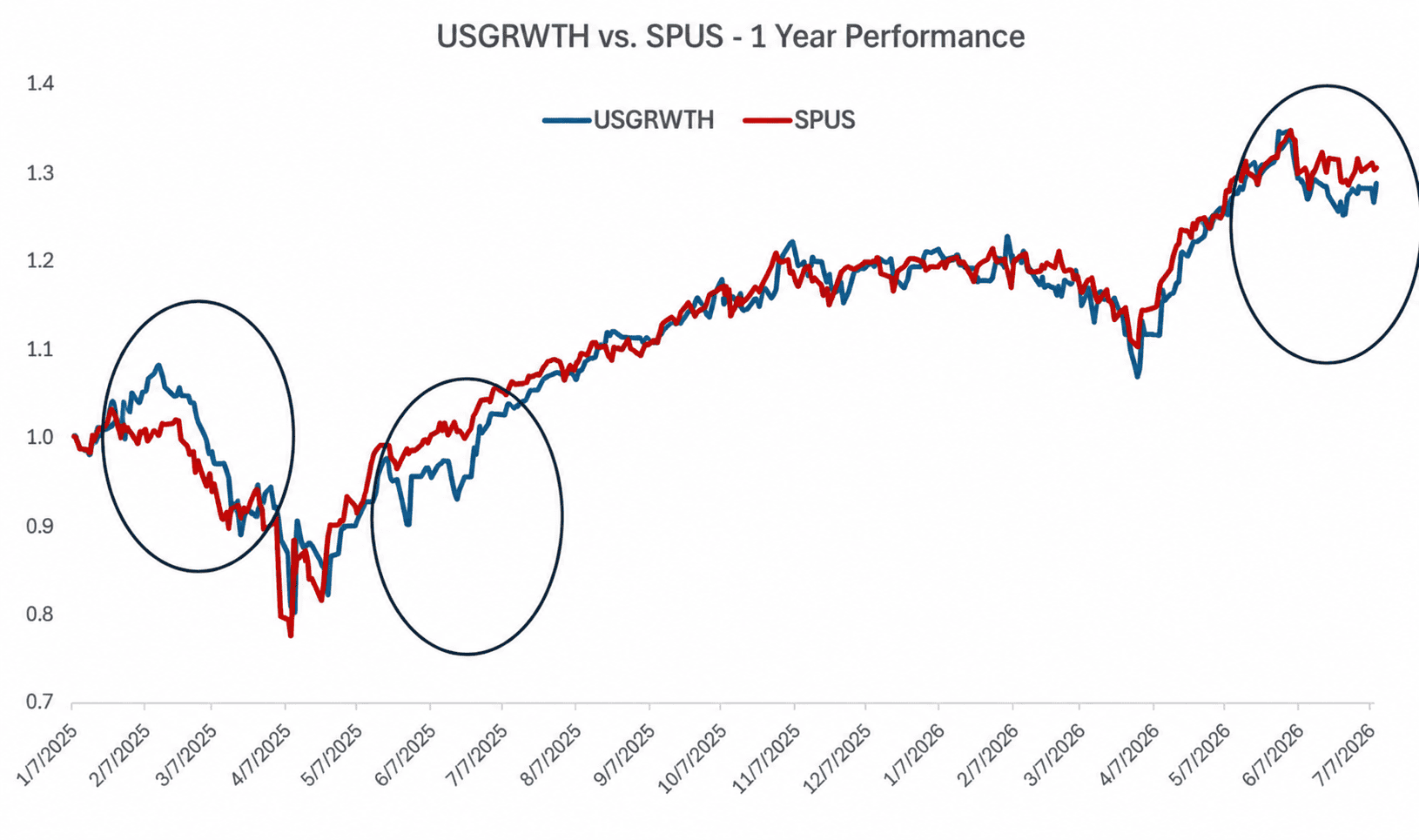

This difference is reflected in the two ETFs. USGRWTH has a higher allocation to the Magnificent Seven than SPUS, which has been an important driver of relative performance. As shown in the chart below, periods of Mag 7 outperformance have generally coincided with stronger relative returns for USGRWTH. Conversely, when mega-cap technology stocks have lagged, USGRWTH has tended to underperform SPUS.

Ultimately, the choice between the two ETFs may depend on your outlook for the Mag 7. Investors who remain constructive on mega-cap technology and believe AI leaders will continue to drive market returns may prefer USGRWTH's higher exposure. Those seeking broader diversification and lower concentration in the largest technology companies may find SPUS the more balanced option.

Performance Snapshot (cumulative)

Top 10 Holdings Comparison

Both funds draw from closely related S&P Shariah-screened US equity universes, so the overlap in mega-cap names is substantial, though weightings diverge.

The sector allocation highlights that both ETFs are heavily concentrated in technology, reflecting the composition of Shariah-screened U.S. equity indices. However, there are meaningful differences beneath the surface. USGRWTH carries higher exposure to Communication Services and Consumer Discretionary, while SPUS allocates relatively more to Health Care, Industrials, and Basic Materials. These differences reflect the funds' distinct benchmark methodologies and portfolio construction rather than fundamentally different investment objectives.

Sector Allocation

Although the two ETFs cannot be compared over identical investment horizons because they launched at different dates, both have delivered strong long-term returns. As of 7 July 2026, USGRWTH had returned 135.09% since inception. SPUS, benefiting from its earlier December 2019 launch, has generated a 206.68% cumulative NAV return since inception, while closely tracking and marginally outperforming its benchmark (198.60%). The strong performance of both funds reflects their significant exposure to U.S. mega-cap technology companies such as Nvidia, Apple, and Microsoft.

Tax and Currency Considerations

For GCC and other non-U.S. investors, tax may be a differentiating factor. USGRWTH is an ADX-listed accumulating ETF that automatically reinvests dividends, while SPUS distributes dividends, which may be subject to 30% U.S. withholding tax for investors from countries without an applicable tax treaty. In addition, investments in U.S.-domiciled ETFs such as SPUS may be subject to U.S. estate tax of up to 40% on assets above US$60,000 for many non-U.S. investors.

Currency is another consideration. While the UAE dirham is pegged to the U.S. dollar, investing in U.S.-listed ETFs can involve foreign exchange conversions, international transfers, and higher brokerage costs. USGRWTH, which trades directly on ADX in AED, offers GCC investors a simpler and potentially lower-cost way to access U.S. equities.

Risks

USGRWTH carries emerging-fund risk: its sub-US$ 10 million AuM base means spreads on ADX may run wider than for an established US-listed peer, and its shorter track record limits statistical confidence in risk metrics such as volatility, beta, and correlation.

SPUS, while deeply liquid, carries standard US equity market risk and concentration risk given its roughly 32% combined weighting in its top three holdings, alongside the volatility typical of growth-oriented, technology-heavy Shariah portfolios.

Bottom line

USGRWTH and SPUS are not competitors so much as regional counterparts within closely related Shariah-screened US equity universes. Both carry matching 0.45% expense ratios, both lean heavily into mega-cap technology, and both counted Nvidia, Apple, and Microsoft among their top holdings as of mid-2026. Both have delivered triple-digit cumulative returns since inception while remaining closely aligned with their respective benchmark indices. Investors are effectively choosing between convenience and scale rather than fundamentally different investment strategies. USGRWTH lowers the barriers to accessing U.S. Shariah equities through a locally listed ADX ETF with automatic dividend reinvestment, while SPUS offers the benefits of institutional scale, deeper liquidity, and a longer operating history. Both provide exposure to many of the same leading U.S. companies, making the choice primarily about how investors prefer to access the market rather than what they own.