China remains one of the world's most important investment markets thanks to its economic scale and its increasingly central role in two of the biggest structural trends of the past two decades: the digital economy and, more recently, artificial intelligence. Yet in 2026, investors have witnessed one of the widest performance gaps between China's offshore and onshore equity markets in years.

Many headlines have focused on the sharp correction in Chinese technology giants listed overseas, mainland China's domestic stock market, particularly its technology-focused STAR Market, has quietly become one of the world's strongest-performing equity markets.

Understanding China's Two Equity Markets

China's equity market is broadly divided into offshore and onshore markets.

The offshore market consists primarily of Chinese companies listed in Hong Kong and the United States. These include household names such as Alibaba, Tencent, JD.com and Baidu. Many of these firms originally chose overseas listings because they did not meet mainland China's profitability and listing requirements at the time, while also seeking access to international investors through Hong Kong listings or U.S. ADR structures.

The onshore market, commonly known as the A-share market, consists of companies listed on the Shanghai Stock Exchange and the Shenzhen Stock Exchange. In 2019, China also launched the STAR Market in Shanghai, designed specifically to support innovative technology companies that may not satisfy the traditional listing requirements of the main exchanges. Today, STAR has become China's flagship market for semiconductor, AI hardware and advanced manufacturing companies.

A Tale of Two Markets

Over the past six months, the performance gap between these markets has become striking.

- Offshore Chinese internet companies, represented by ETFs such as KWEB, have fallen roughly 37%.

- Broad onshore A-share ETFs, including KBA and CNYA, have gained approximately 12%.

- Meanwhile, China's innovation-focused STAR Market, represented by KSTR, has surged nearly 50%, making it one of the best-performing equity segments globally.

Such a divergence raises an important question for investors: Should investors continue chasing the strong momentum in mainland China, or does the weakness in offshore Chinese technology present a compelling contrarian opportunity?

Why Have the Markets Diverged?

Several factors help explain this growing divide.

1. AI Spending Has Become a Double-Edged Sword

Following the excitement surrounding DeepSeek earlier this year, investor expectations for China's internet giants increased significantly.

However, recent earnings reports from companies such as Alibaba and Tencent highlighted the enormous capital required to compete in artificial intelligence. Spending on AI infrastructure, chips and research has accelerated rapidly, placing pressure on free cash flow and near-term profitability.

While these investments may strengthen long-term competitiveness, investors have become increasingly concerned about earnings over the next several years.

Ironically, companies investing the most aggressively in AI are being penalized today for building tomorrow's growth.

2. China's Consumer Recovery Remains Uneven

China's property market and consumer spending continue to recover only gradually.

Many offshore technology companies generate significant revenues from e-commerce, online advertising and domestic consumption. As a result, softer retail spending and weaker consumer confidence continue to weigh on earnings expectations.

Recent economic data has generally disappointed markets, particularly when compared with last year's stimulus-driven rebound.

3. The Semiconductor Story Is Happening Onshore

Perhaps the biggest differentiator has been China's determination to build a self-sufficient semiconductor industry.

Following U.S. export restrictions on advanced chips, Beijing has accelerated investment into domestic chip design, manufacturing equipment and AI infrastructure.

The STAR Market is heavily exposed to these strategic industries through companies developing processors, semiconductor equipment and AI hardware.

Even NVIDIA CEO Jensen Huang recently acknowledged that U.S. chip restrictions may ultimately accelerate the rise of domestic Chinese competitors, potentially allowing companies such as Huawei and other local champions to capture an increasing share of the world's second-largest technology market.

This structural policy support has become a powerful tailwind for mainland technology companies.

4. Currency Stability Has Helped Both Markets

The relative strength of the Chinese yuan against the U.S. dollar has provided a supportive backdrop for Chinese assets overall.

Although currency has not been the primary driver of the performance divergence, it has helped reduce one traditional headwind for international investors allocating to China.

Momentum or Contrarian Opportunity?

The divergence leaves investors facing two very different investment approaches.

Momentum investors may continue favoring mainland A-shares and the STAR Market, where government policy, semiconductor investment and domestic innovation continue to attract capital.

Contrarian investors, however, may see an opportunity in offshore Chinese technology companies, many of which now trade near multi-year valuation lows despite remaining global leaders in e-commerce, cloud computing, digital payments and artificial intelligence.

Current valuations suggest much of the near-term pessimism may already be reflected in prices.

Why Investors May Need Both

Rather than choosing one market over the other, investors may benefit from owning both.

The two markets provide remarkably different exposures.

The onshore A-share market resembles a broad domestic economy benchmark, with significant representation across industrials, healthcare, consumer companies, financials, renewable energy, advanced manufacturing and China's rapidly expanding semiconductor ecosystem.

The offshore market, by contrast, remains concentrated in internet platforms, digital advertising, cloud computing, artificial intelligence and consumer technology leaders.

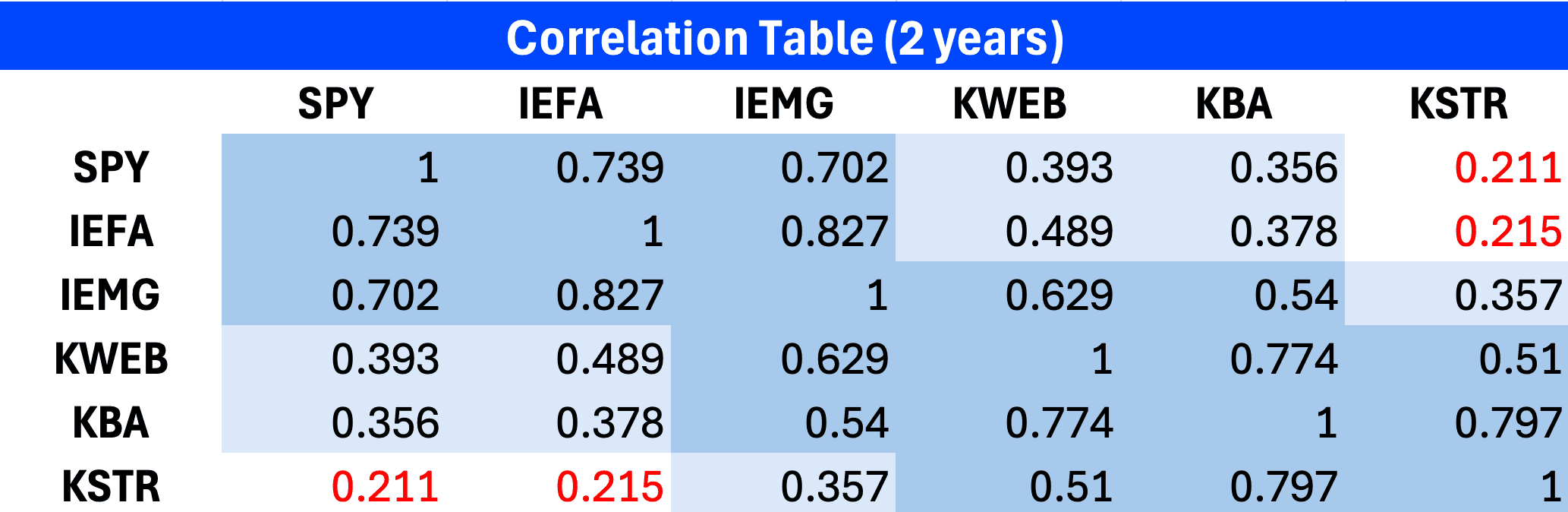

Perhaps most importantly, the STAR and A-share markets historically exhibit one of the lowest correlations with the S&P 500 among major global equity markets, providing meaningful diversification benefits within an international portfolio. Offshore Chinese technology stocks, meanwhile, tend to move more closely with global technology sentiment and AI-related headlines.

Bottom Line

China's equity market is increasingly becoming a story of two distinct economies.

One market reflects China's domestic industrial transformation, semiconductor ambitions and policy-driven innovation. The other reflects globally recognized internet platforms navigating slower consumer growth while investing heavily in the next generation of AI.

For investors, understanding this distinction has never been more important. Rather than viewing "China" as a single allocation, 2026 has demonstrated that where investors gain exposure may matter just as much as whether they invest in China at all.