China’s central bank extended its gold-buying streak in June, adding 480,000 fine troy ounces and lifting official holdings to 75.44 million ounces, according to People’s Bank of China data cited by Reuters. The addition, equal to nearly 15 tonnes, was China’s largest monthly increase since October 2023 and marked the 20th consecutive month of accumulation.

The better way to frame this is that China bought into a price pullback, rather than bought gold at a special discount. Spot gold fell 11.65% in June, its steepest monthly drop since October 2008, while the value of China’s reported gold reserves fell to $303.72 billion from $340.75 billion in May even though physical holdings increased. For GCC investors, that is the useful signal pointing that official-sector demand continued even as market pricing moved against the asset.

Central Banks Are Still Adding Gold

China’s move fits a wider reserve-management trend. The World Gold Council’s 2026 Central Bank Gold Reserves Survey, conducted between 5 February and 19 May with 76 central-bank responses, found that 89% of respondents expect global central-bank gold reserves to increase over the next 12 months. A record 45% expect their own institution’s gold reserves to rise over the same period.

The same survey said central banks accumulated an average of 1,000 tonnes of gold a year over the past four years, double the 500-tonne average over the previous decade. Reserve managers cited performance during crises, portfolio diversification, inflation hedging and geopolitical risk as reasons for holding or adding gold. For a region such as the GCC, where sovereign portfolios already sit at the intersection of oil revenue, dollar liquidity and geopolitical exposure, that official-sector behaviour is relevant even when ETF flows turn weaker.

Gold ETF Flows Tell a More Tactical Story

Data shows that physically backed gold ETFs lost $8.9 billion during the month, with outflows across all regions and North America recording the largest withdrawals. Even so, first-half flows remained positive at $8 billion, while collective holdings rose by 18 tonnes to 4,047 tonnes. Global gold ETF assets fell 6% in H1 to $526 billion, mainly because of the lower gold price.

Central banks appear to be using gold as a reserve asset, while ETF investors are more sensitive to real yields, dollar strength, price momentum and short-term macro positioning. GCC allocators should read China’s buying as a reserve signal, not as a timing instruction.

Why GCC Gold ETFs Are Part of the Story

For regional investors, the question is less “gold or no gold” and more “which structure delivers the exposure cleanly?”

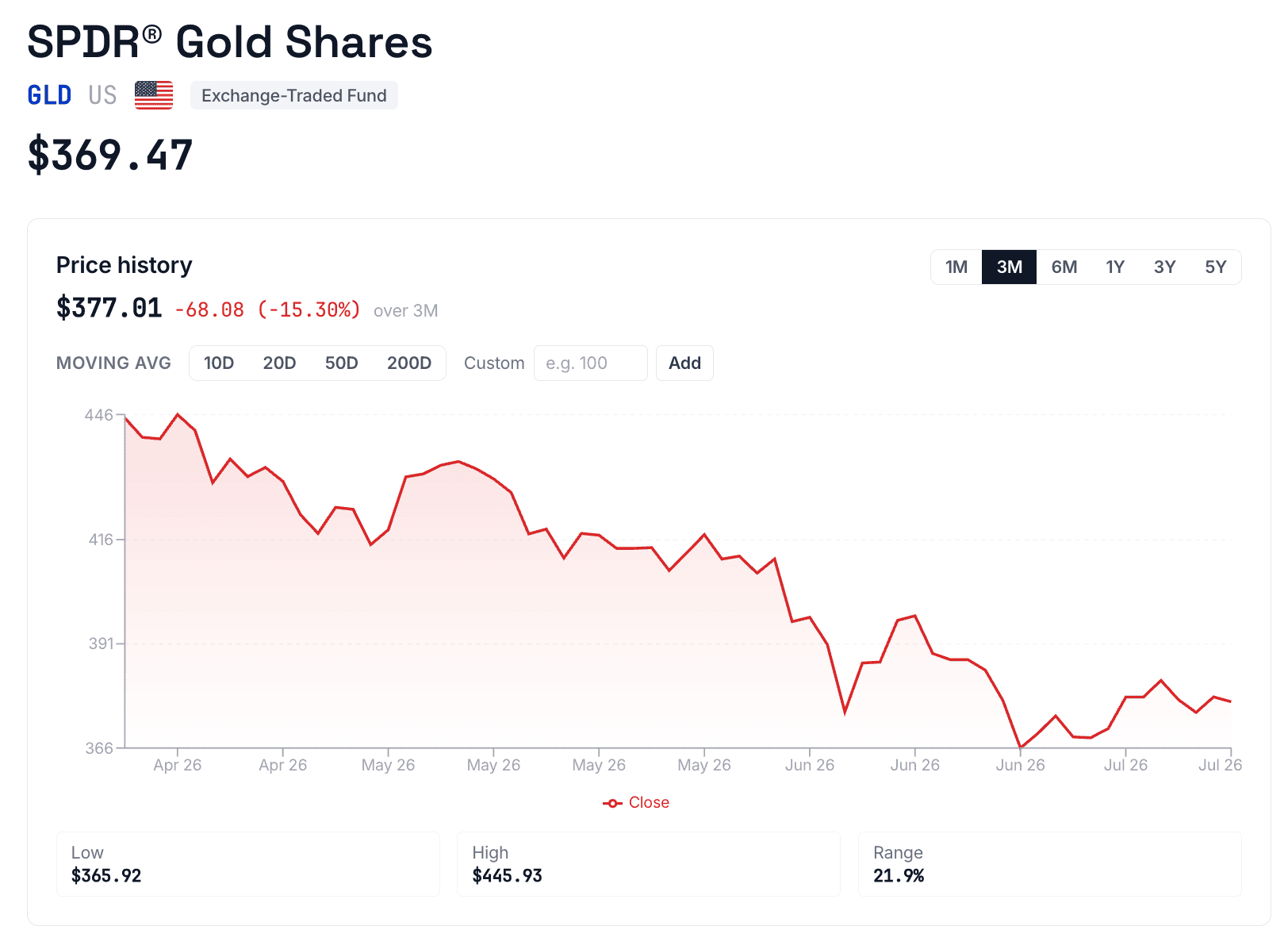

A global ETF such as SPDR Gold Shares offers deep liquidity and institutional familiarity, but GCC investors still need to assess domicile, withholding-tax treatment where relevant, custody arrangements and trading spreads.

The local route is developing through Albilad Gold ETF, ticker 9405 on Tadawul. Albilad Capital describes the fund as the region’s first Sharia-compliant commodity gold ETF, benchmarked to the DGCX spot gold price. Its Q1 2026 report says the fund buys physical gold, stores it in Dubai Multi Commodities Centre and uses Sharia-compliant DGCX spot gold contracts. The fund returned 6.33% in Q1 2026 and 48.55% over one year, versus 6.44% and 50.09% for its benchmark.

China’s latest purchase does not remove gold’s risks. A stronger dollar, higher real yields or calmer geopolitics can still pressure bullion and gold ETFs. The more useful point for GCC readers is that gold demand is becoming more institutional and more Asian, while Tadawul already gives regional investors a Sharia-screened route linked to Dubai’s bullion infrastructure.