Executive Summary

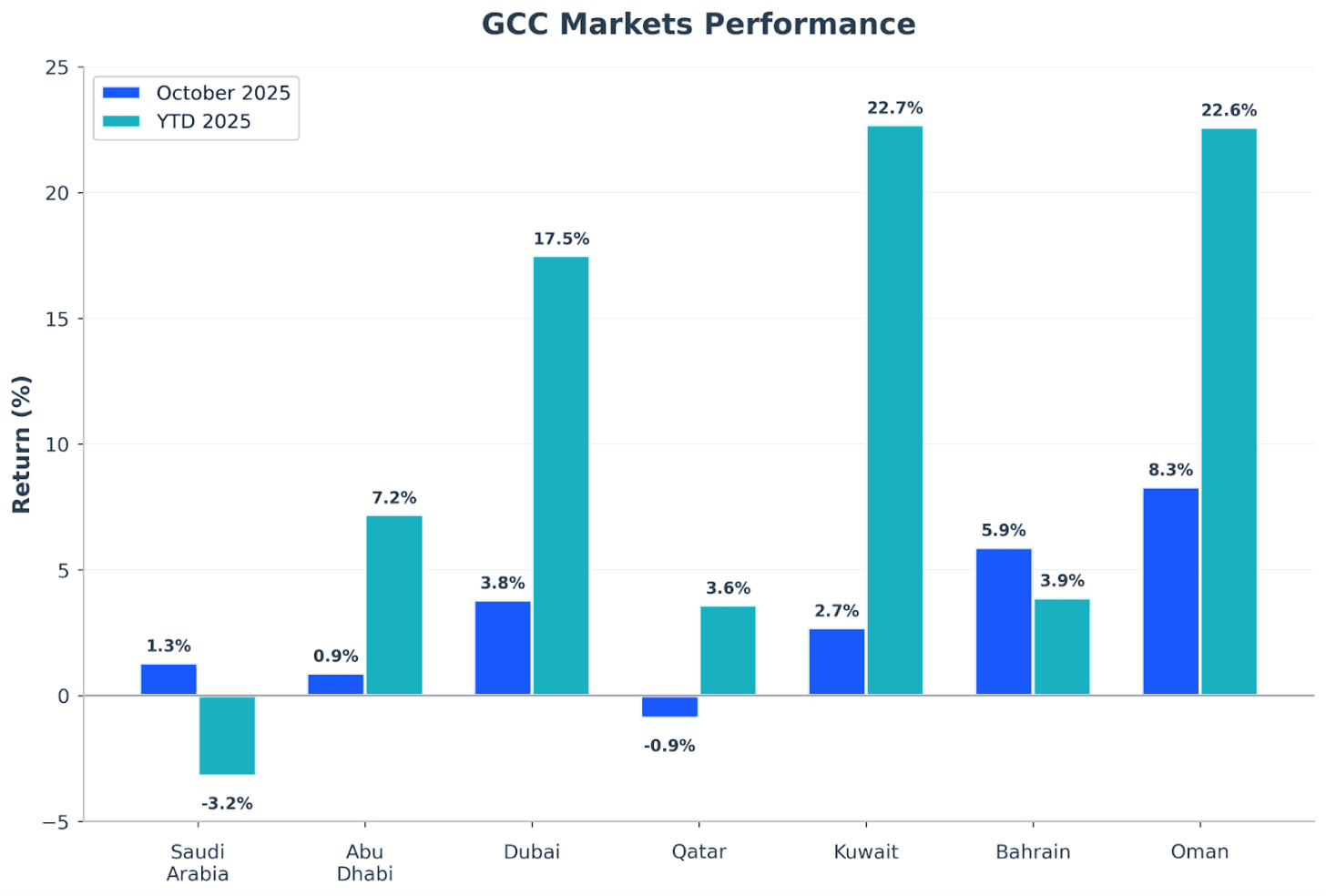

Gulf Cooperation Council (GCC) equity markets posted mixed but generally positive results in October 2025, with the MSCI GCC Index advancing 1.2% for the month, building on September’s momentum. The regional benchmark’s performance was underpinned by robust showings from Oman (+8.3%) and Bahrain (+5.9%), while Dubai’s 3.8% gain reflected continued strength in real estate and financial sectors. Saudi Arabia’s Tadawul, representing approximately 60% of regional market capitalization, edged up 1.3% despite lingering concerns over foreign ownership reforms. Qatar stood alone in negative territory, declining 0.9% amid mixed corporate earnings.

Year-to-date, Kuwait maintains its position as the region’s stellar performer with a 22.7% return, closely followed by Oman at 22.6%. The divergent performance across markets reflects varying exposure to oil price dynamics, real estate momentum, and structural reform progress.

Market Highlights

- Regional Benchmark: MSCI GCC Index +1.2% (October), +14.55% (1-year)

- Market Cap: $4.155 trillion aggregate GCC market capitalization

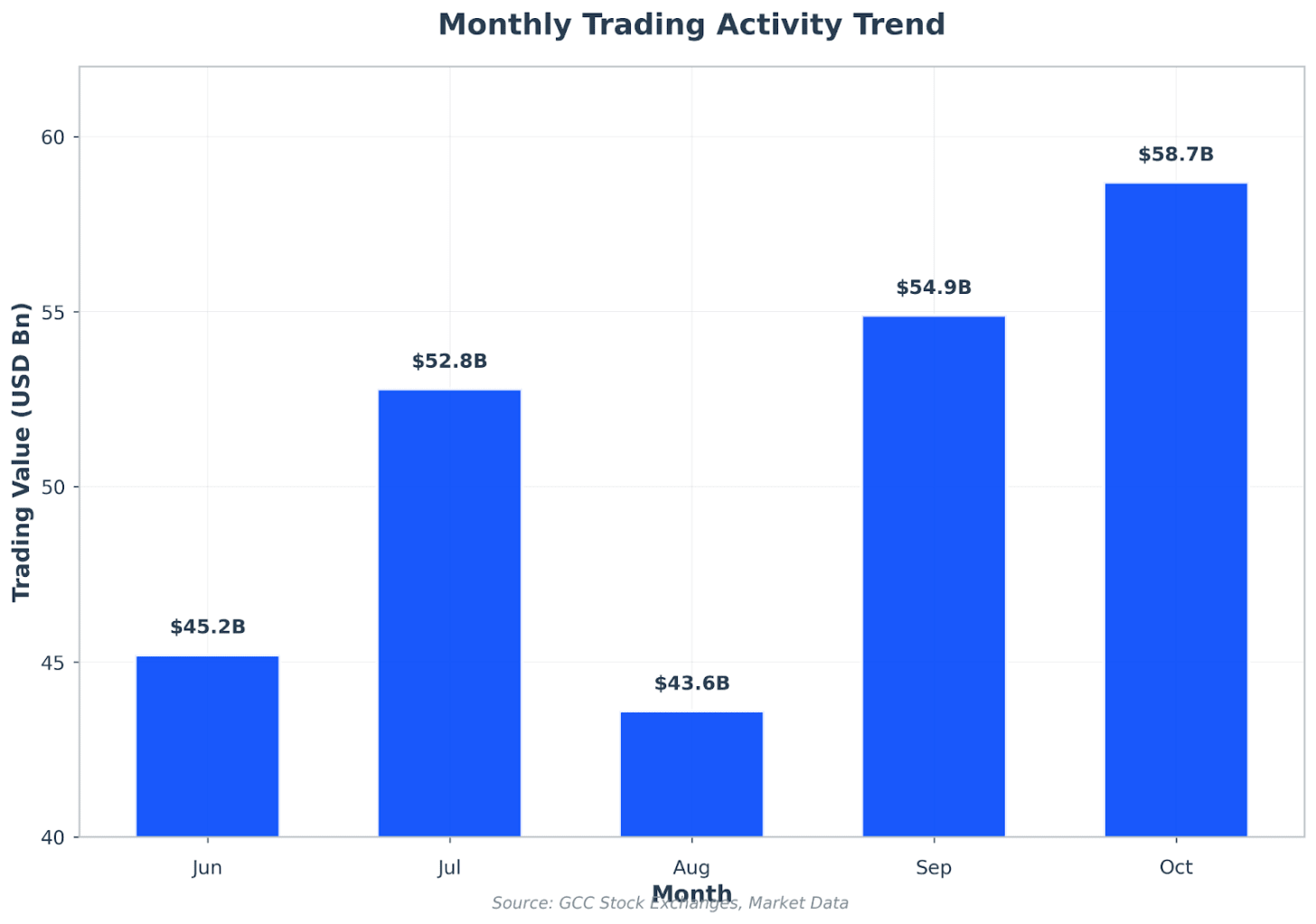

- Trading Activity: $58.7 billion monthly traded value, up 6.9% month-on-month

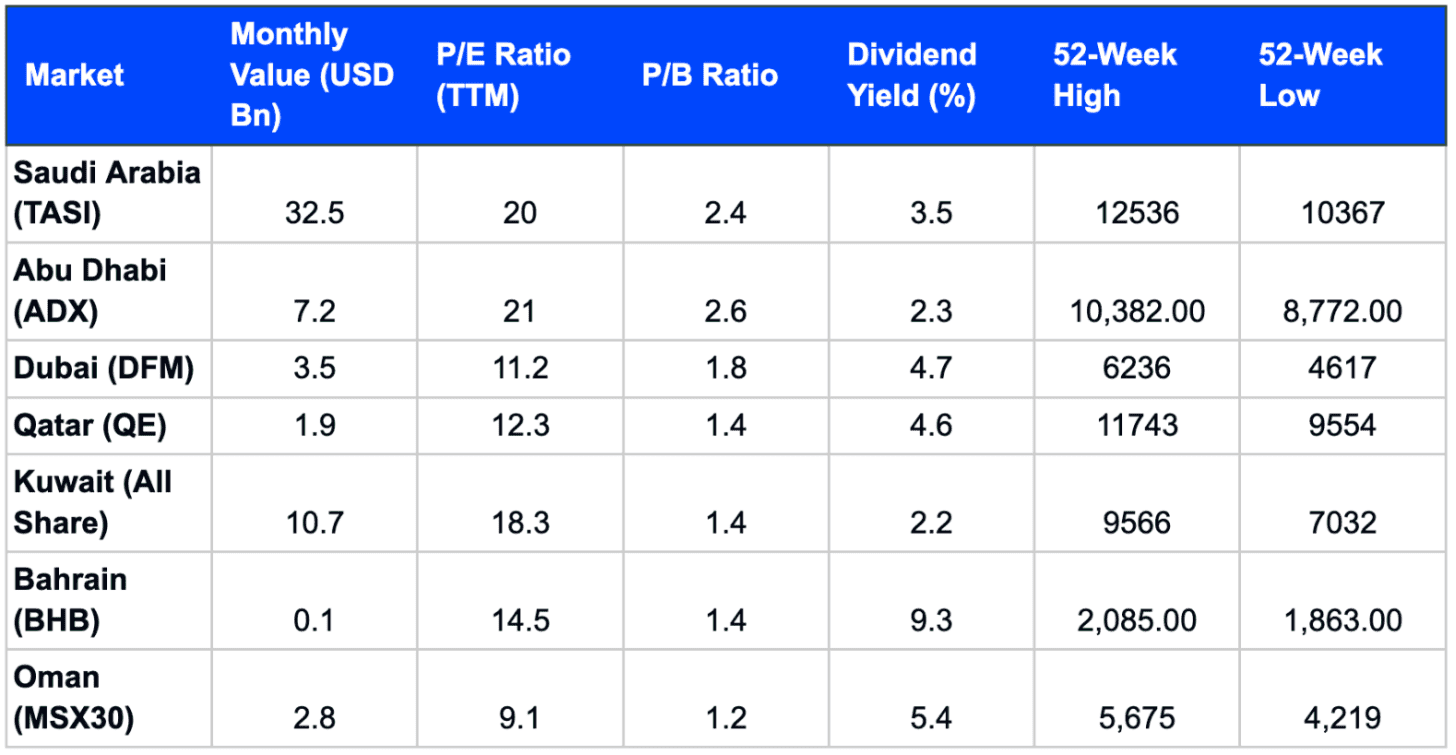

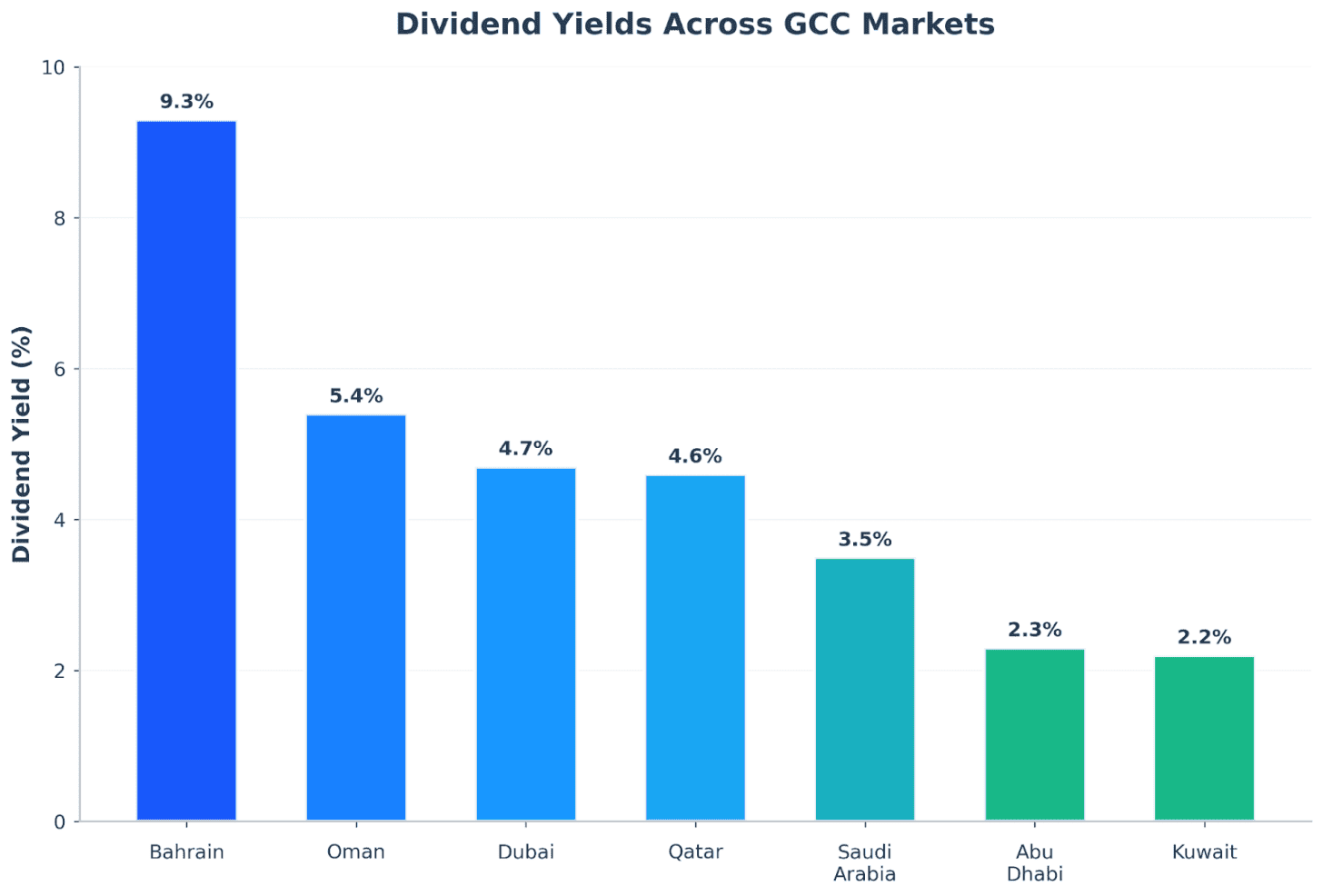

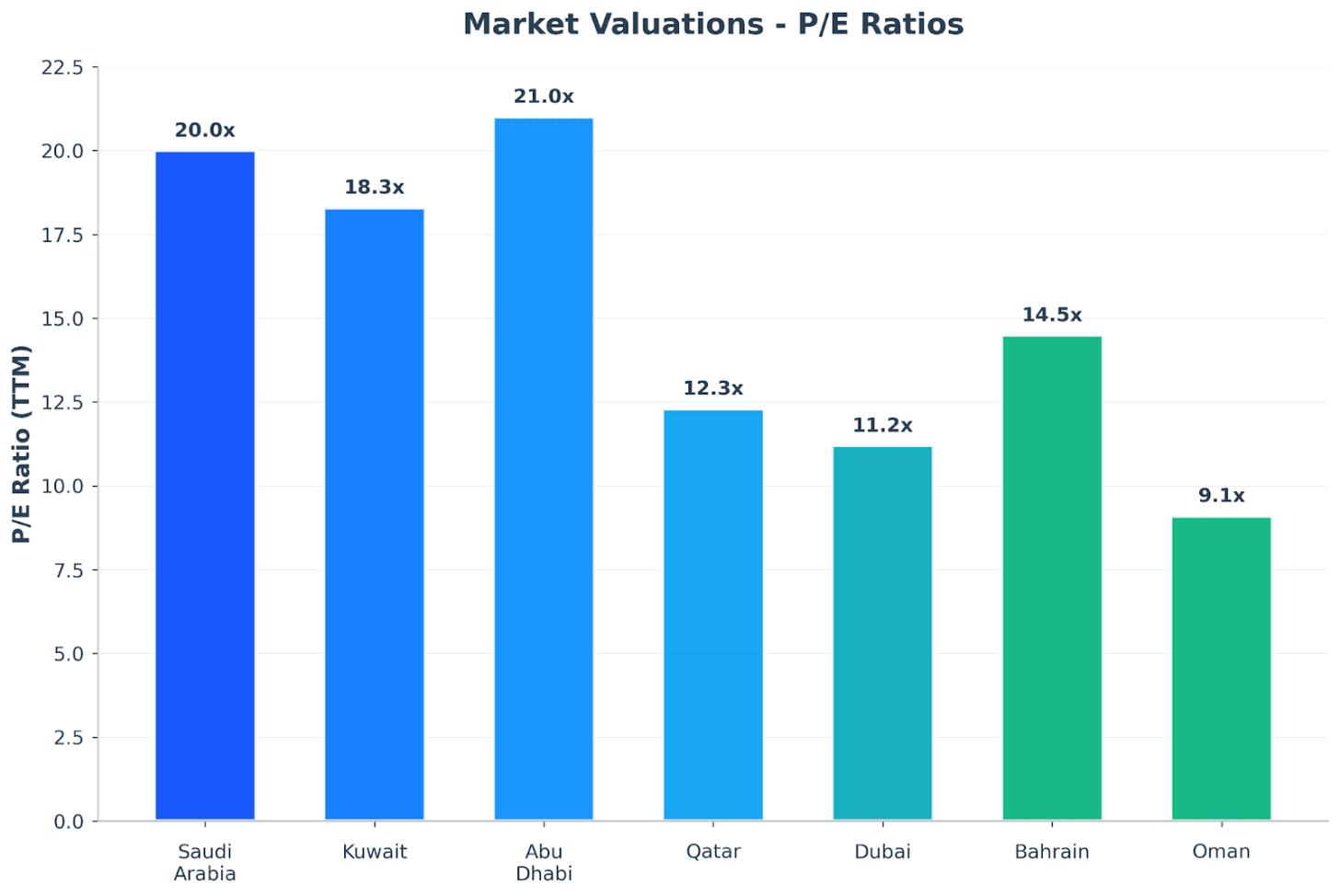

- Valuation: Regional P/E of 18.3x (trailing), dividend yield averaging 3.5%

- Best Performer: Oman MSX 30 Index +8.3% (fourth consecutive monthly gain)

- Laggard: Qatar Exchange -0.9% (third straight monthly decline)

Regional Overview

October’s positive momentum reflects a confluence of supportive factors: the U.S. Federal Reserve’s 25 basis point rate cut (matched by most GCC central banks), easing China-U.S. trade tensions following high-level talks, and generally solid third-quarter corporate earnings. The MSCI GCC Countries Domestic Index has now gained 14.55% over the trailing twelve months, outperforming MSCI Frontier Markets despite underperforming MSCI Emerging Markets.

Trading liquidity remained robust at $58.7 billion for the month, marking a 6.9% increase from September and the highest monthly level since January 2025. This uptick in activity suggests growing investor confidence despite persistent concerns over oil prices, which declined 2.9% in October to $65.10 per barrel.

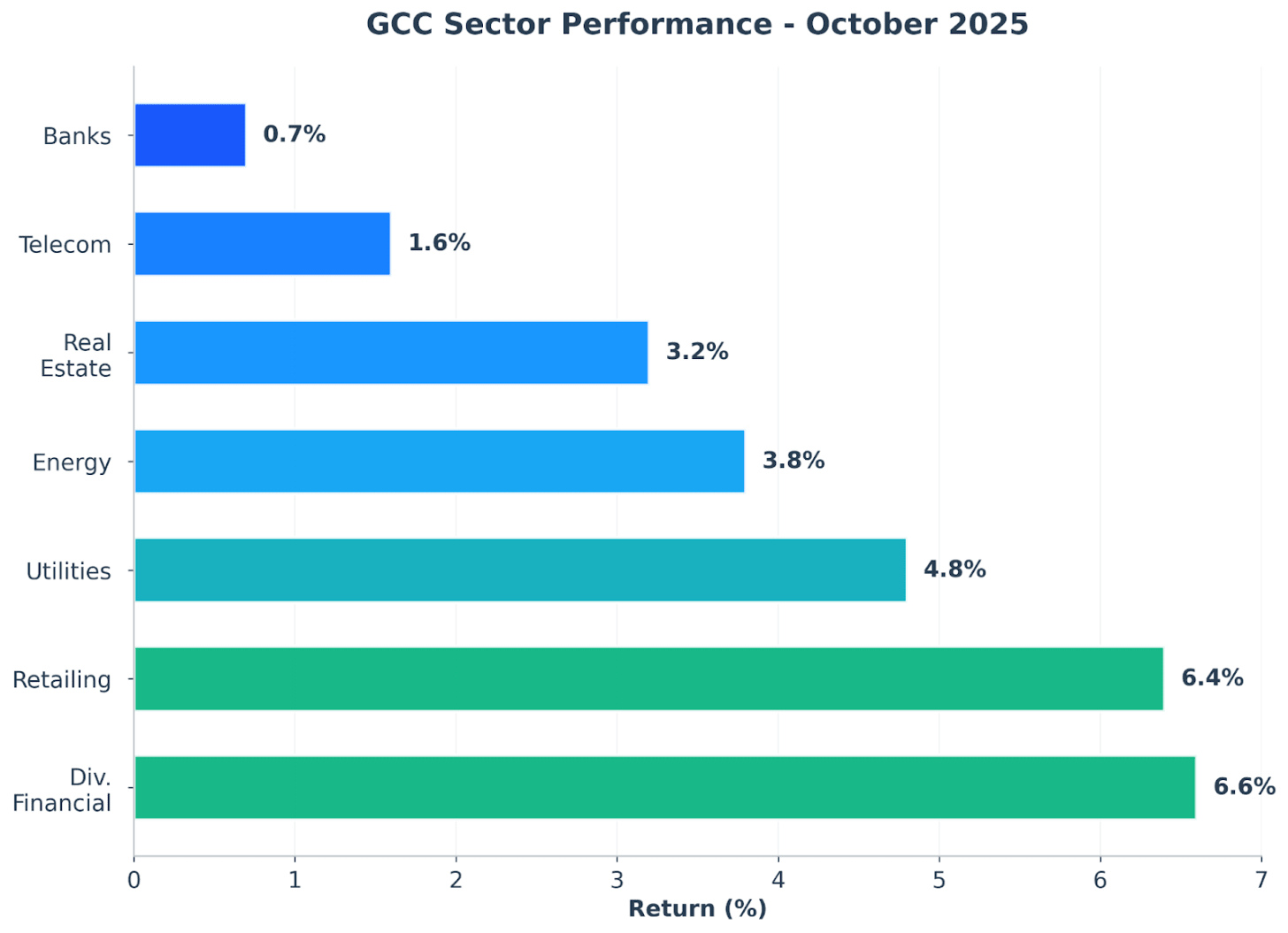

Sector performance was largely constructive, with Diversified Financials (+6.6%), Retailing (+6.4%), and Utilities (+4.8%) leading advances. The heavyweight Banking sector, representing nearly 60% of regional market capitalization, posted a modest 0.7% gain, while Energy rose 3.8% despite oil price weakness.

Saudi Arabia: Tadawul Navigates Reform Uncertainties

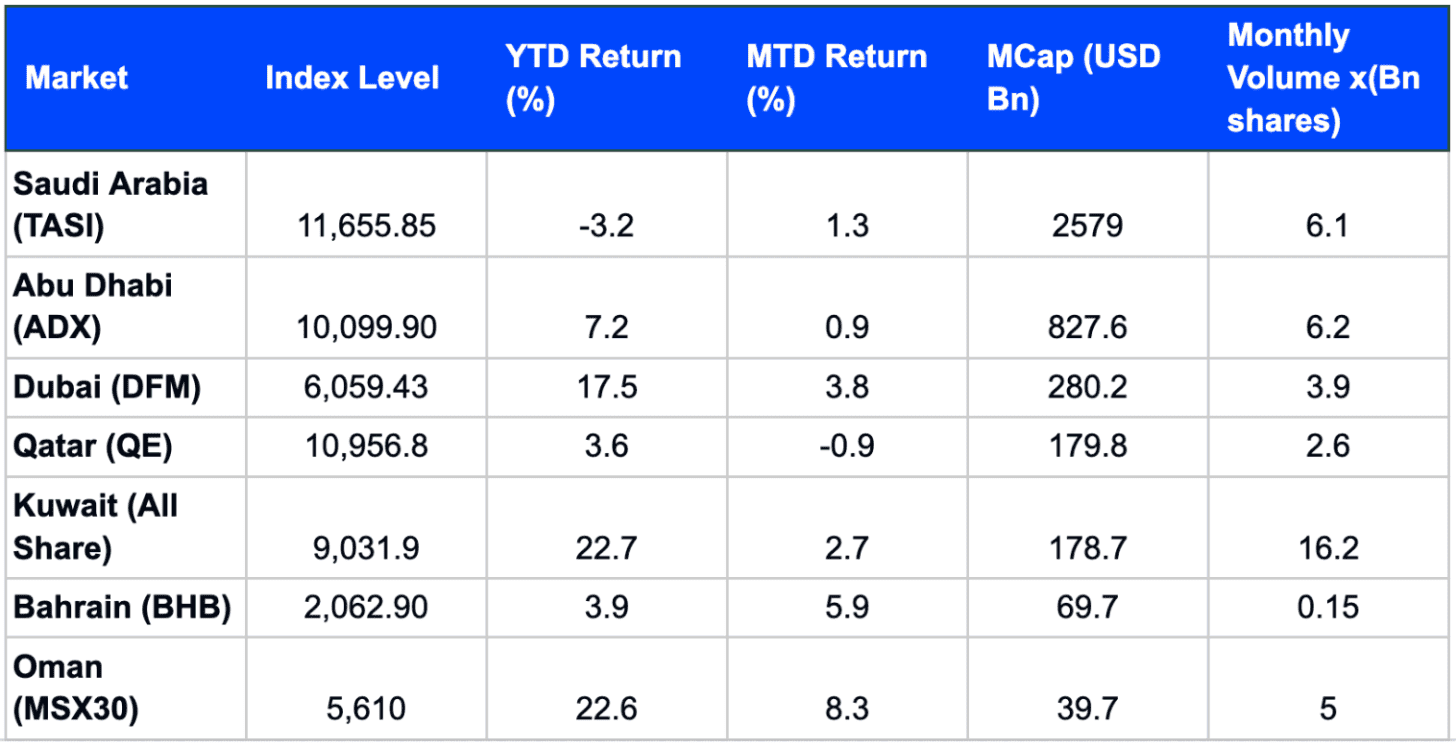

Performance: TASI +1.3% (October), -3.2% (YTD)

Saudi Arabia’s benchmark index closed October at 11,655.85 points, registering its second consecutive monthly gain despite ongoing deliberations over foreign ownership liberalization. The index briefly touched an intraday high of 11,752.08 on October 29, its strongest level since May 2025 before profit-taking in the final sessions capped gains.

Sector rotation was evident as investors positioned for potential reform announcements. The Utilities sector surged 10.9%, driven primarily by ACWA Power’s 12.9% advance following news that the company expanded its project portfolio to $115 billion across 110 projects globally. The Energy sector gained 5.4% despite weak crude prices, with Saudi Aramco adding 5.2% ahead of third-quarter results. Aldrees Petroleum (+22.3%) and Rabigh Refining (+21.8%) were standout performers following Saudi Aramco’s acquisition of a 22.5% stake in Rabigh Refining.

The Banking sector, however, weighed on the index with a 0.6% decline as investors remained cautious pending clarity on foreign ownership rules. Al Rajhi Bank, the index’s largest constituent by weight at 16.4%, slipped 1.4% despite reporting a 24.6% year-on-year increase in third-quarter net profit to SAR 6.4 billion. Saudi National Bank fared better, gaining 2.0% after posting a 20.5% profit increase.

Trading activity moderated slightly with monthly value traded declining 3.0% to SAR 121.9 billion, though volumes increased 5.2% to 6.1 billion shares. The market trades at 20.0x trailing earnings with a dividend yield of 3.5%.

UAE Markets: Dubai Real Estate Momentum Continues

Abu Dhabi (ADX)

Performance: ADX General Index +0.9% (October), +7.2% (YTD)

Abu Dhabi’s index reclaimed the 10,000-point psychological level, closing at 10,099.90 points as heavyweight financials and telecommunications stocks provided support. First Abu Dhabi Bank, the emirate’s largest lender, jumped 11.5% after reporting a 24% increase in nine-month net profit, while National Bank of Fujairah surged 13.5%.

The exchange saw increased foreign interest with trading value rising 5.8% to AED 26.5 billion. ADNOC Gas remained the most actively traded stock with 800 million shares changing hands, followed by Multiply Group and ADNOC Drilling. The market’s forward-looking indicators remain constructive with the IMF projecting 6% GDP growth for Abu Dhabi in 2025.

Dubai (DFM)

Performance: DFM General Index +3.8% (October), +17.5% (YTD)

Dubai outperformed regional peers, propelled by continued strength in real estate and banking stocks. The Real Estate Index surged 7.7%, with Emaar Properties gaining 8.8% after unveiling an AED 100 billion masterplan featuring 40,000 luxury homes. The developer’s ambitious expansion plans, including potential entry into the U.S. market, resonated with investors betting on sustained demand from international buyers.

Emirates NBD emerged as a star performer with a 15.6% advance following the announcement of its planned $3 billion acquisition of a 60% stake in India’s RBL Bank, marking the largest foreign direct investment in India’s banking sector. The bank’s nine-month net profit grew 12% year-on-year, supporting its international expansion strategy.

Trading activity was mixed with volumes up marginally by 0.9% to 3.9 billion shares, while value traded declined 7.7% to AED 12.9 billion. The exchange trades at an attractive 11.2x P/E ratio with a dividend yield of 4.7%.

Rest of GCC: Kuwait Maintains Regional Leadership

Kuwait

Performance: All Share Index +2.7% (October), +22.7% (YTD)

Kuwait retained its position as the GCC’s best-performing market year-to-date, with mid and small-cap stocks driving October’s gains. The Main Market Index surged 5.5% while the blue-chip Premier Market Index added a more modest 2.1%.

The Energy sector led with an 11.0% gain, powered by Senergy Holding’s 22.4% surge following contract extensions with Kuwait Oil Company worth KWD 8.2 million. Financial Services jumped 10.8% as Al-Deera Holding soared 83.6% and Osoul Investment gained 53.2%.

Notably, trading activity hit record levels with monthly value traded surging 43.5% to KWD 3.3 billion, the highest on record. This surge in liquidity coincided with Kuwait’s successful $11.25 billion bond issuance in October, its first following the passage of the public debt law in April 2025.

Qatar

Performance: QE 20 Index -0.9% (October), +3.6% (YTD)

Qatar’s benchmark extended its losing streak to three months, weighed down by profit-taking in real estate (-4.1%) and transportation (-3.0%) stocks. The weakness came despite generally positive third-quarter earnings, with the banking sector reporting flat profit growth of 0.08% year-on-year to QAR 23.3 billion.

Commercial Bank of Qatar led decliners with a 9.8% drop following a 23.7% decline in nine-month profits, while Ezdan Holding fell 9.2%. Trading activity reflected investor caution with volumes down 18.7% and value traded falling 22.9% to QAR 7.1 billion, the lowest monthly level since December 2024.

Bahrain

Performance: All Share Index +5.9% (October), +3.9% (YTD)

Bahrain posted the second-best monthly performance in the GCC, driven by a 22.2% surge in the Materials sector as Aluminum Bahrain (Alba) rallied 22.9% following the renewal of its strategic alliance with Norsk Hydro. GFH Financial Group led overall gainers with a 27.7% advance, contributing to a 2.9% rise in the Financials Index.

Trading activity spiked dramatically with volume up 190% to 148.6 million shares and value traded increasing 142% to BHD 36.1 million, primarily driven by speculative interest in GFH Financial Group.

Oman

Performance: MSX 30 Index +8.3% (October), +22.6% (YTD)

Oman’s remarkable run continued with the index posting its fourth consecutive monthly gain and reaching eight-year highs. The Services sector led with a 9.0% advance, while Financials gained 8.3% as OMINVEST surged 25.8% and Sohar Bank added 9.6%.

Asyad Shipping Company topped individual performers with a 35.9% gain after announcing the $209 million purchase of three Newcastlemax dry bulk carriers. Trading value more than doubled, surging 109.7% to OMR 1.1 billion as foreign investors increased exposure to the sultanate’s diversifying economy.

As we conclude the review of Oman’s domestic performance, it is useful to step back and consider how the region as a whole is currently valued. GCC markets exhibit a diverse mix of growth prospects, sector compositions, and income profiles, which shape relative attractiveness for investors.

To provide this context, the following charts illustrate comparative P/E ratios and dividend yields across the GCC ahead of the outlook section.

Outlook: Valuations Attractive Amid Reform Momentum

Looking ahead, GCC markets appear positioned for continued gains supported by several tailwinds:

Positive Factors:

- Monetary Easing: Further Fed rate cuts expected in 2025 should ease financial conditions

- Structural Reforms: Saudi Vision 2030 projects gaining momentum; UAE economic diversification accelerating

- Valuations: Regional P/E of 18.3x remains below historical averages

- Dividend Yields: Average 3.5% yield attractive in a lower rate environment

- GDP Growth: IMF projects 4.8% growth for UAE, 6% for Abu Dhabi specifically

Risk Factors:

- Oil Price Weakness: Sustained pressure below $70/barrel could weigh on fiscal positions

- Geopolitical Tensions: Regional conflicts remain a wildcard

- Foreign Flows: Implementation of Saudi foreign ownership reforms remains uncertain

- China Slowdown: Weaker demand from Asia could impact export-oriented sectors

Investment Implications

For ETF investors, the divergent performance across markets argues for selective country exposure rather than broad regional funds. Kuwait’s momentum and attractive valuations, coupled with Dubai’s real estate dynamism, offer the most compelling risk-reward profiles. Qatar’s underperformance may present a contrarian opportunity ahead of potential catalysts including further gas expansion projects.

The upcoming earnings season will be crucial in determining whether October’s gains can be sustained through year-end. With most markets trading below peak valuations and reform momentum building, the medium-term outlook remains constructive for selective opportunities across GCC equities.