For decades, luxury companies have been enduring symbols of growth and prosperity. Many have existed for over a century, evolving from European heritage brands into global powerhouses with deep roots across the West, China, and the Middle East. More than just businesses, they’ve come to represent success itself. It’s difficult to argue that this fundamental dynamic has changed. If anything, continued global wealth creation, particularly rising GDP per capita should support another long-term leg of growth.

As Geir Espeskog, the CEO of Boreas behind the Lunate S&P Absolute Luxury ETF, noted in a recent LinkedIn post, “Human nature never goes out of fashion.” The desire for status, quality, and exclusivity remains deeply embedded.

Still, the sector is clearly under pressure. After years of strong outperformance, leading luxury names from LVMH to Hermès have entered a sustained correction. This shift reflects a mix of cyclical and structural headwinds, from softer demand in key markets to changing consumption patterns. More recently, geopolitical tensions, including the conflict in the Middle East, have added another layer of uncertainty.

The question now isn’t whether luxury disappears, but whether this is a pause before the next cycle, as conflicts dissipate and China and Europe rebound from a consumer slump that extended for many years. Some of these stocks are trading well below their long term trends. Is this a strong buying opportunity for legendary companies that seem to be selling at a discount?

Recent Performance

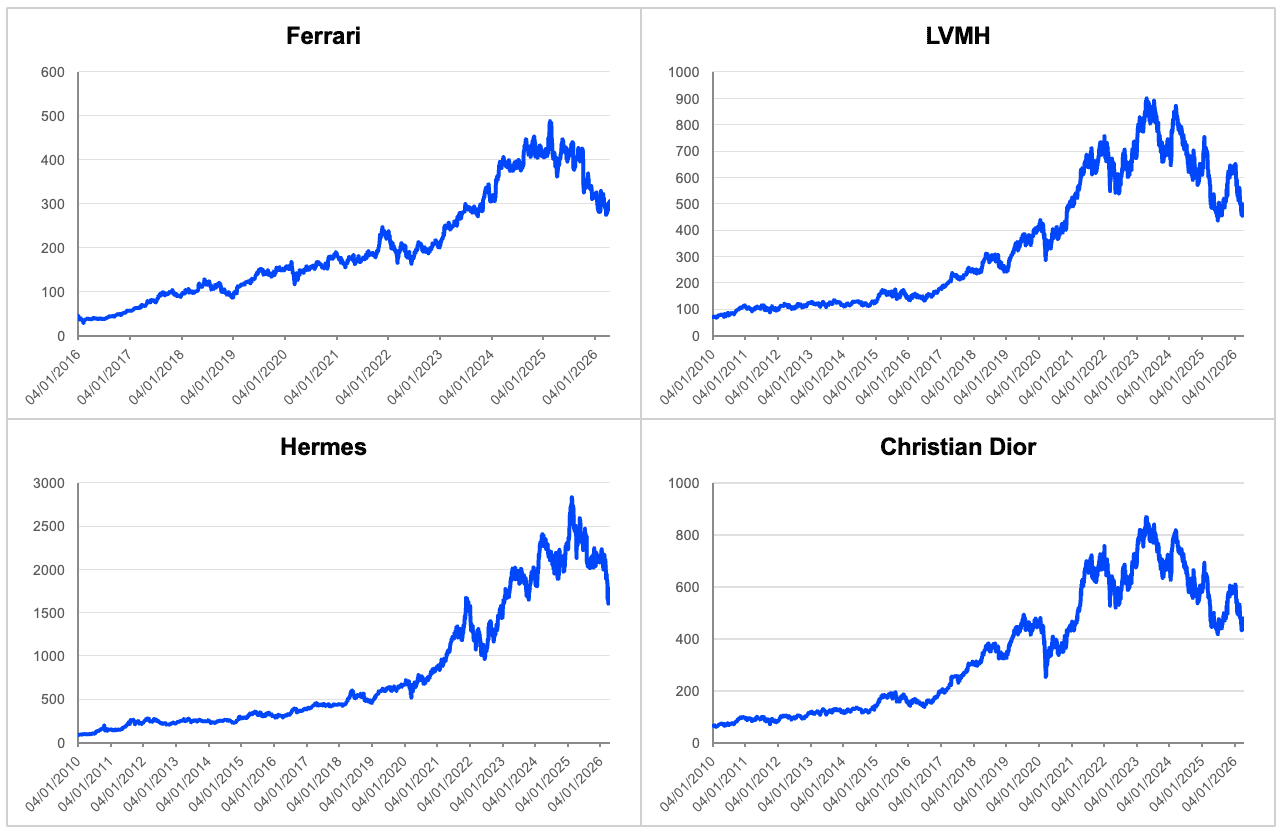

Many luxury stocks are down more than 30% from their peaks, with some exceeding 50% drawdowns. The sector tends to be highly momentum-driven, meaning that when sentiment turns bearish, declines often become broad-based and self-reinforcing. However, markets rarely move on momentum alone indefinitely. At some point, valuations and underlying fundamentals begin to reassert themselves. That inflection point where fundamentals outweigh sentiment could mark the early stages of a recovery in luxury stocks.

China, AI, and Sentiment Shock

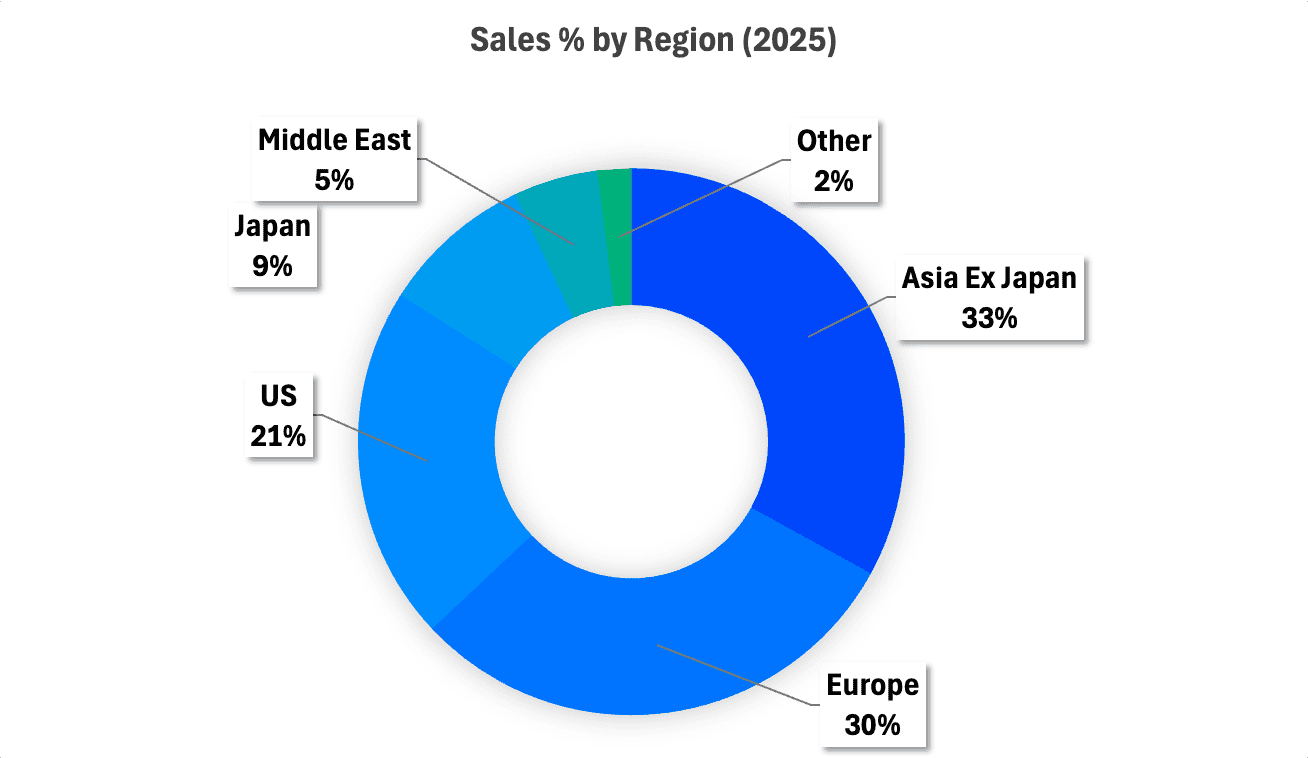

The first pressure point has been China, which at one stage accounted for more than 30% of global luxury demand. Amid a prolonged consumer and real estate slowdown, growth has moderated over the past few years. However, this is widely seen as cyclical rather than structural, with analysts expecting a pickup as conditions stabilize. China still represents roughly 20% of the world’s millionaires, and the underlying drivers of wealth creation remain intact. As the artificial intelligence and advanced manufacturing cycles continue to unfold, GDP per capita is expected to keep rising, supporting a renewed trajectory for luxury consumption.

The second pressure point is geopolitical. Recent shocks have heightened uncertainty while pushing oil prices and inflation higher. This dynamic is likely to weigh on discretionary spending, particularly in energy-sensitive regions such as Europe, India, and parts of emerging markets, where luxury demand tends to be more cyclical.

Structural Moats

Despite the near-term uncertainty, the underlying business models remain resilient. Luxury companies operate with some of the strongest competitive moats in global equities built on heritage, brand equity, and controlled scarcity.

“These are companies with 100- to 200-year histories,” Geir says. “They’ve survived the transition from horses to cars. They adapt.”

Unlike cyclical consumer sectors, luxury brands are less exposed to commoditization. Their pricing power, high margins, and global customer base tend to be sticky and hard to penetrate by new entrants. Luxury companies have also been trying to cater to lower income levels than their traditional consumers, by driving creativity and efficiency in design and production.

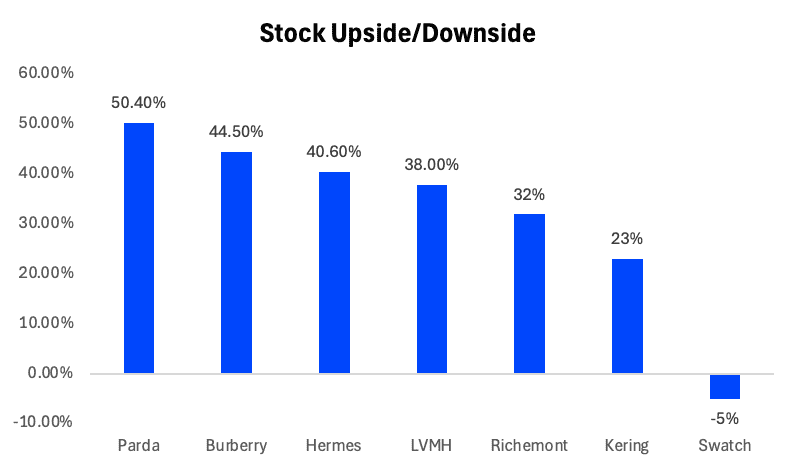

HSBC, in a recent report, reiterated its view that luxury stocks have been excessively beaten down. The bank maintains buy ratings across much of the sector, including LVMH, Hermès, Kering, Prada, and Burberry, among others. It expects a number of these names to deliver strong returns over the coming investment period.

Based on HSBC estimates

A Valuation Reset

What makes the current environment notable is the extent of the drawdown.

Geir Espesgok also highlighted in his post, many of the stocks are trading well below their long term averages with Hermes price two standard deviations below its 15-year trend, based on long-term log charts.

ETF Angle: Accessing Luxury Through Listed Vehicles

For investors, the question is not just whether luxury rebounds, but how to access it efficiently.

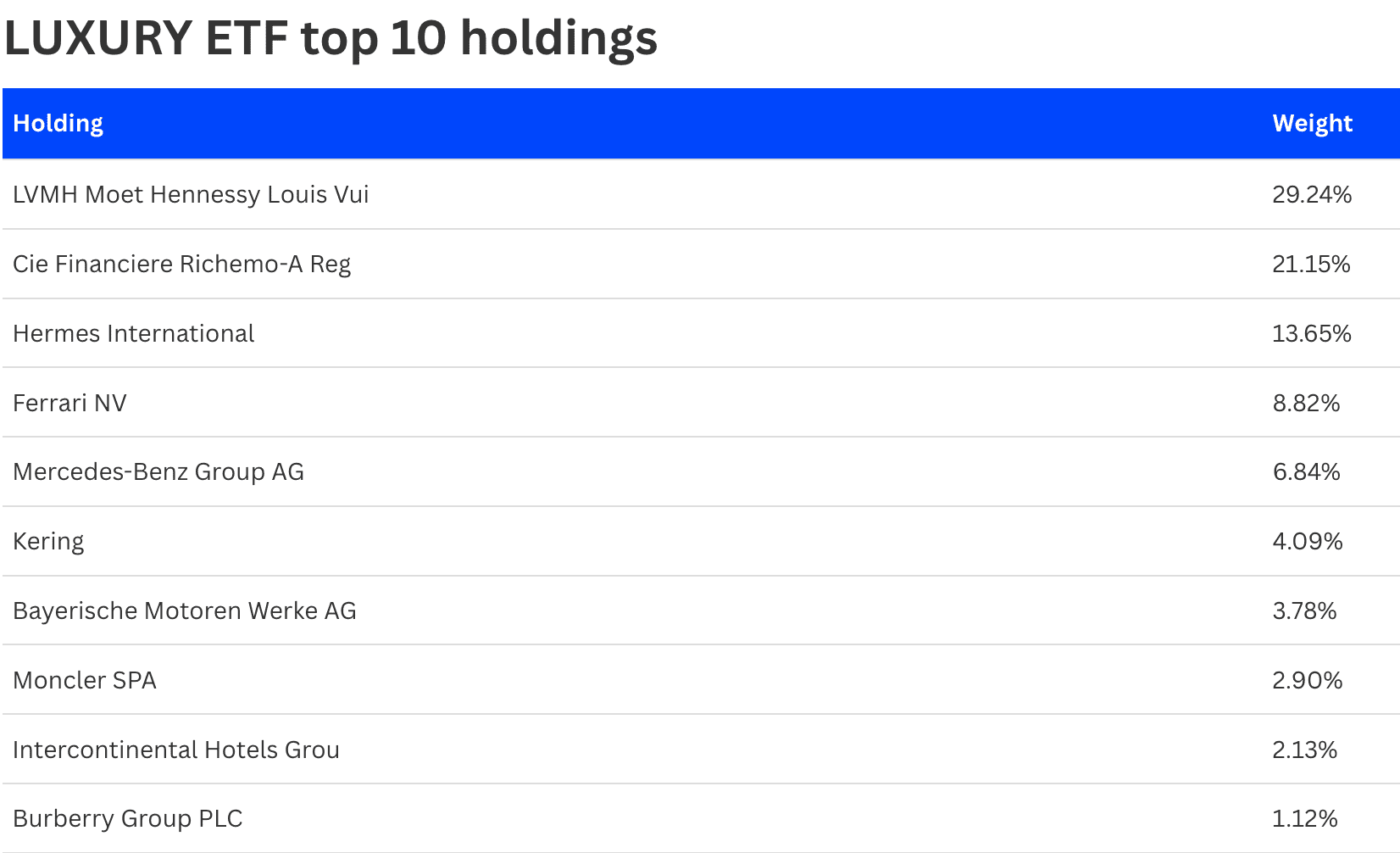

The Boreas S&P Absolute Lunate UCITS ETF provides targeted exposure to global luxury brands, capturing companies across fashion, automobiles, and premium consumer goods. Meanwhile, regional platforms such as Lunate are increasingly expanding thematic ETF offerings, reflecting growing demand for sector-specific exposures within the GCC.

Such vehicles offer a structured way to participate in the sector’s long-term dynamics, while mitigating single-stock risk, particularly relevant during periods of heightened volatility.

The Bottom Line

Luxury sits at the intersection of macro cycles, consumer sentiment, and long-term wealth creation. The current sell-off reflects a combination of all three: China slowdown, AI-driven rotation, and geopolitical uncertainty.

But it also raises a deeper question, whether the market is underestimating the durability of one of the most established sectors in global equities.