Why Is the SpaceX IPO Being Called the Biggest Listing in History?

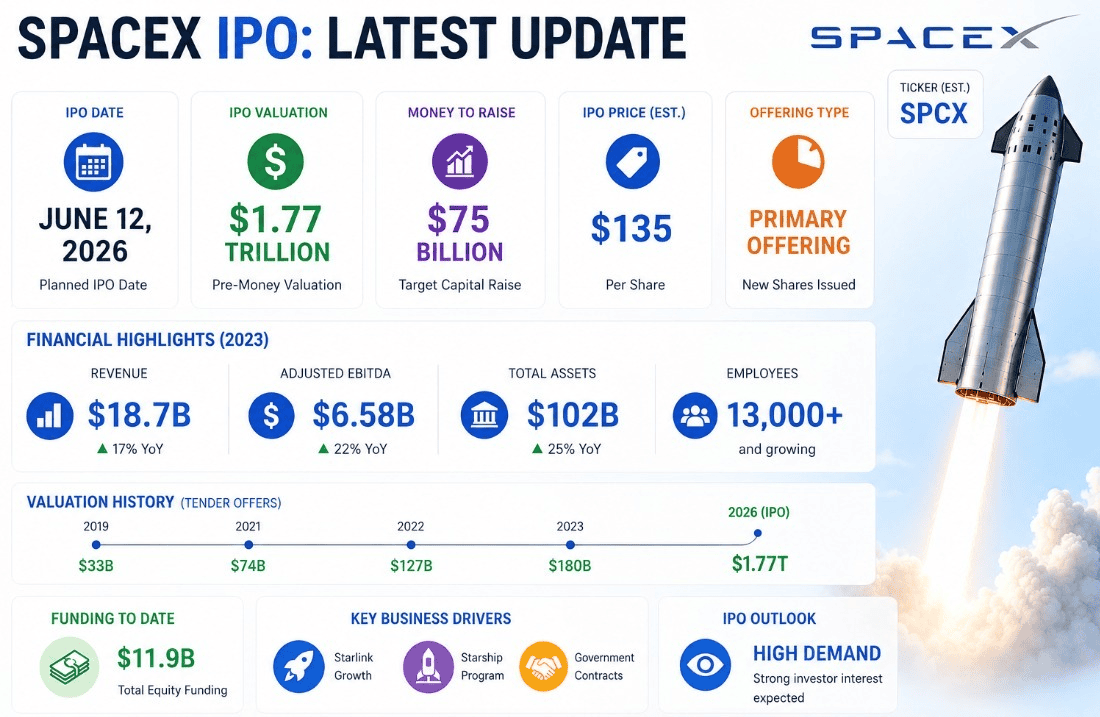

SpaceX is set to begin trading on Nasdaq (ticker: SPCX) on June 12, 2026, in what is expected to be the largest initial public offering (IPO) ever completed.

The company is offering 555.6 million Class A shares at a fixed price of $135 per share, raising approximately $75 billion and implying a valuation of about $1.77 trillion. That makes SpaceX larger than Tesla, Meta, and Berkshire Hathaway by market value and more than doubles the amount raised in Saudi Aramco's record-setting 2019 IPO.

The mechanics are unconventional. Rather than a traditional price-range-and-book-build process, SpaceX dictated $135 as a take-it-or-leave-it price. Retail investors are being allocated roughly 30% of shares (~$22.5 billion) through Fidelity, Charles Schwab, Robinhood, SoFi, and E-Trade, far above the typical 5-10% retail slice. Demand has been extraordinary: Reuters reported order books exceeding $250 billion, with the IPO running 3.5-4x oversubscribed.

The question for investors is whether SpaceX can justify a valuation that places it among the world's most valuable public companies from day one.

What Are Investors Actually Buying When They Buy SpaceX?

SpaceX operates across three business segments:

The company generated approximately $18.7 billion in revenue during 2025, representing growth of around 33% year-over-year. However, it remains loss-making on a GAAP basis, reporting a net loss of roughly $4.9 billion.

Investors are therefore paying for future growth rather than current profitability.

Can SpaceX Justify a $1.77 Trillion Valuation?

At $1.77 trillion on $18.7 billion in revenue, SpaceX prices at approx 95x trailing revenue, the highest multiple of any major tech IPO on record:

Even among highly anticipated technology listings, SpaceX stands in a category of its own. The valuation reflects investor expectations that Starlink, launch services, and future AI-related businesses will grow substantially over the coming decade.

Could ETF Buying Become the Next Major Catalyst for SpaceX Shares?

Nasdaq-100 (~July 6, 2026): A revised Nasdaq methodology effective May 1, 2026, allows any newly listed company ranked among the top 40 by market cap to enter the Nasdaq-100 after just 15 trading days, with the prior free-float requirement eliminated. That puts SpaceX in the index around July 6, triggering forced buying from QQQ ($496B AUM), QQQM ($98B AUM), and UCITS Nasdaq-100 ETFs available across GCC brokerage platforms.

S&P 500 (earliest: mid-2027): S&P Dow Jones Indices confirmed on June 4 that it would not relax profitability requirements. SpaceX's GAAP losses rule it out until at least mid-2027, deferring an estimated $50+ billion in additional forced buying, a second catalyst that active investors may look to front-run.

Even market participants across the Gulf who bypass direct SPCX purchases will likely gain exposure via structural index rebalancing over the coming 12–18 months. Potential index inclusion could generate substantial passive inflows from ETF and index-tracking funds.

What Does History Tell Us About Mega IPOs After the Hype Fades?

The historical record on large IPOs is instructive. The Ritholtz/FactSet chart covering the top 10 US IPOs by size since 1999 shows an average 1-year forward return of -28.5% from the first trading day's close.

Meta is the most instructive parallel. It debuted at $38 in May 2012 amid enormous hype, barely moved on day one due to a Nasdaq technical glitch, then fell more than 50% over the following four months, spending over a year below its offering price before eventually becoming one of the greatest wealth creators in market history.

Crypto perpetuals offer a live read on market expectations: SpaceX pre-IPO perps on Hyperliquid were trading around $162 as of yesterday, implying a ~20% day-one pop from the $135 offer price, but this has cooled sharply from a peak above $220.

Bottomline

The SpaceX IPO is one of the most significant public listings in modern market history. The company combines several of the most powerful investment themes of the coming decade, including space infrastructure, satellite communications, artificial intelligence, and large-scale computing.

For GCC investors, the story extends beyond the IPO itself. Potential inclusion in major global indices means many investors may ultimately gain exposure through ETFs and passive investment vehicles, regardless of whether they participate in the offering.

Yet history suggests caution. The largest IPOs in history have often struggled to meet the lofty expectations embedded in their valuations. SpaceX may ultimately become one of the world's most valuable businesses, but the first year as a public company will likely depend less on the quality of the business and more on whether investors believe a valuation approaching $1.8 trillion can be justified.