Global markets entered the week under pressure after a stronger-than-expected U.S. employment report reshaped expectations for interest rates.

For investors, the issue was not simply that the U.S. economy added jobs. It was that the labor market looked strong enough to give the Federal Reserve more room to keep policy tight, or potentially raise rates later this year if inflation remains sticky.

That matters for the GCC because regional markets are closely tied to global liquidity conditions, U.S. dollar strength, oil prices, and investor appetite for emerging-market risk. Yet the reaction across Gulf markets was not uniform. While global equities sold off, several GCC indices showed relative resilience, helped by oil prices, local earnings momentum, bank strength, and a market structure that remains less exposed to the high-duration technology trade driving U.S. volatility.

U.S. Market Reaction: Strong Jobs, Higher Rate Anxiety

The U.S. jobs report showed nonfarm payrolls rising by 172,000 in May, well above expectations, while unemployment remained steady at 4.3%. March and April payroll gains were also revised higher by 93,000 jobs.

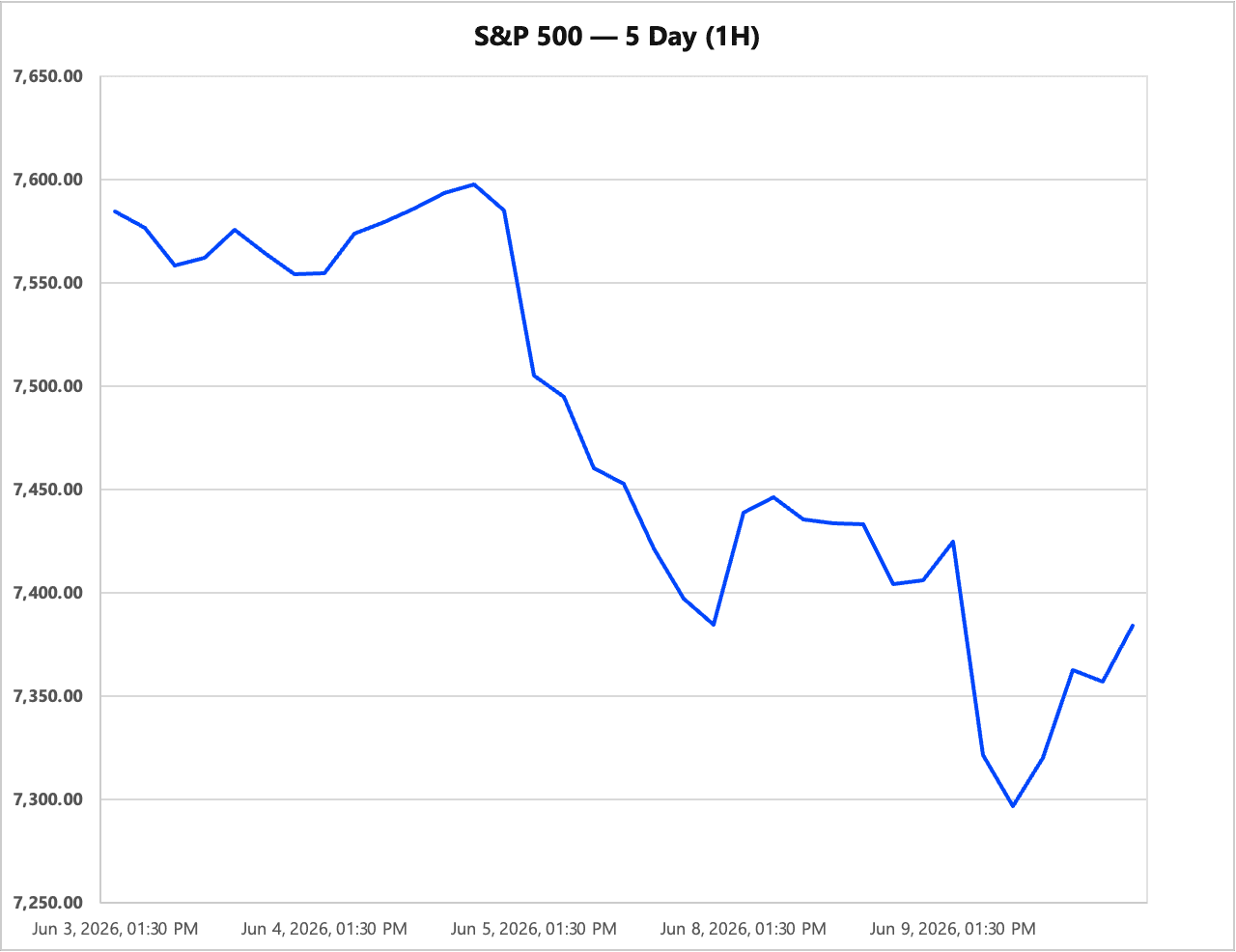

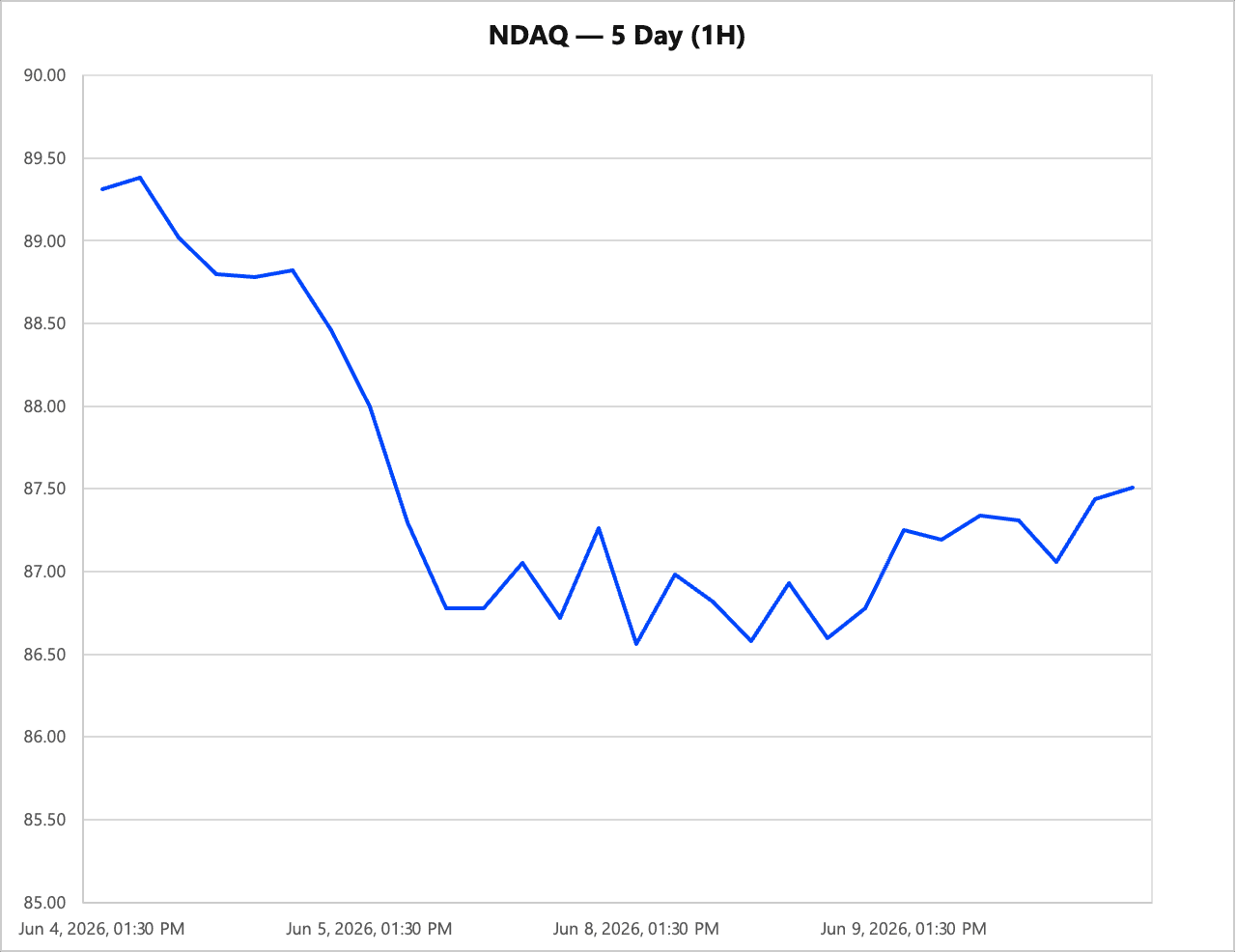

Markets reacted sharply because stronger employment reduces the urgency for the Federal Reserve to ease policy. Interest-rate traders increased the probability of a Fed hike by December, while Treasury yields moved higher and U.S. stocks sold off. The pressure was concentrated in growth and technology shares, with the Nasdaq Composite falling 4.2% on Friday, its worst single-day decline in more than a year. The S&P 500 dropped 2.65%, ending a nine-week winning streak, while the Dow Jones Industrial Average was comparatively more resilient as the selloff was concentrated in AI, semiconductor, and high-duration technology names.

When yields rise, future earnings become less attractive in today’s terms, which usually weighs on AI, software, semiconductors, and other long-duration equity themes. Reuters noted that the selloff extended a broader retreat from favored AI and chip names, with rate expectations moving higher after the jobs data.

This week’s inflation report now becomes the next major test. A soft CPI print could calm markets and revive rate-cut hopes. A hotter print would reinforce the idea that the Fed may need to stay restrictive for longer, keeping pressure on risk assets and global equity sentiment.

GCC Markets: A Different Kind of Market Reaction

Regional markets were not immune to global risk-off sentiment, but they were also not simply tracking the U.S. selloff. Since GCC indices are more heavily exposed to banks, energy, real estate, telecoms, and dividend-paying companies than to the high-growth technology sectors that dominate U.S. indices.

Saudi Arabia’s TASI initially came under pressure during the risk-off move, but later rebounded strongly, rising around 1% as heavyweight financials recovered. Saudi National Bank was among the key contributors, while energy names remained supported by elevated oil prices.

Dubai also showed resilience, with the DFM General Index gaining around 0.7% on Tuesday after earlier weakness. Emirates NBD and Emaar Properties helped support the move, reflecting the continued importance of banks and real estate to Dubai’s equity market.

Abu Dhabi was more volatile. The FTSE ADX General Index fell more than 1% during the initial risk-off session, pressured by large-cap names such as International Holding Company and Aldar Properties. However, it later recovered part of the decline as regional sentiment improved.

Qatar saw one of the sharper swings. The QE Index fell more than 2% during the initial selloff before rebounding nearly 2% the following session, helped by a recovery in banking and industrial names. Oman also held up relatively well, with the MSX 30 gaining modestly after a strong year-long run.

What the ETF Performance Shows

The reaction across GCC-focused ETFs broadly mirrored the resilience seen in regional equity markets.

The Chimera S&P UAE UCITS ETF, which provides exposure to leading UAE-listed companies, remained relatively stable compared with the sharp selloff seen in U.S. technology stocks. Its exposure to banks, real estate, utilities, and dividend-paying companies helped cushion volatility during the risk-off period.

A similar pattern was visible in the Albilad Saudi Sovereign Sukuk ETF and Saudi-focused equity products, which benefited from the Kingdom's strong banking sector, elevated oil prices, and continued domestic economic activity. While global investors were reducing exposure to high-growth technology names, GCC-focused funds remained supported by fundamentally different drivers.

The Albilad Gold ETF also attracted attention as investors sought defensive assets amid rising uncertainty around U.S. interest rates and inflation expectations. Gold has historically benefited during periods when markets become concerned about monetary policy, making it an important diversification tool within regional portfolios.

Perhaps most notably, the Chimera S&P KSA Shariah ETF continued to outperform many broader regional products on a year-to-date basis, reflecting investor confidence in Saudi Arabia's economic transformation story. Banking, infrastructure, tourism, and Vision 2030-related investments continue to support market sentiment even as global investors reassess risk assets.

GCC ETFs are increasingly driven by regional fundamentals rather than simply tracking moves in U.S. markets. While Wall Street remains an important influence, factors such as oil prices, government spending, banking profitability, and domestic economic growth are playing an increasingly important role in shaping returns across regional ETF products.

Why the GCC Environment Still Looks Different

While GCC markets have experienced volatility, much of the recent weakness was driven by geopolitical tensions rather than a deterioration in economic fundamentals. Several regional indices remain below their pre-conflict levels despite resilient earnings, strong bank profitability, and ongoing government spending.

As a result, GCC markets are increasingly trading on different drivers than U.S. equities. While Wall Street remains focused on inflation, interest rates, and AI valuations, GCC investors are paying closer attention to oil prices, banking sector earnings, dividends, and economic diversification initiatives.

Oil continues to provide a fiscal cushion for regional governments, while banks benefit from a higher-rate environment through healthy net interest margins. These factors have helped support regional markets even as global investors reassess risk assets.

Risks remain. Higher U.S. rates can still tighten liquidity and pressure investor sentiment. However, recent market performance suggests GCC assets are increasingly being driven by regional fundamentals rather than simply following Wall Street.

Conclusion

The latest market move shows that GCC equities are increasingly being tested by global macro forces, but they are not simply mirroring Wall Street.

The U.S. selloff was driven by a stronger labor market, higher rate expectations, and pressure on growth stocks. The GCC reaction was more balanced, shaped by oil, banks, dividends, local earnings, and regional liquidity.

The GCC market is becoming more diverse. Local income strategies, sukuk exposure, dividend ETFs, and Shariah products may behave differently from global thematic ETFs during periods of volatility.

That makes the next inflation report critical.

If U.S. inflation cools, risk appetite could recover quickly. If inflation surprises higher, markets may need to reprice again, and the divide between defensive GCC exposure and high-growth global themes could become even more visible.