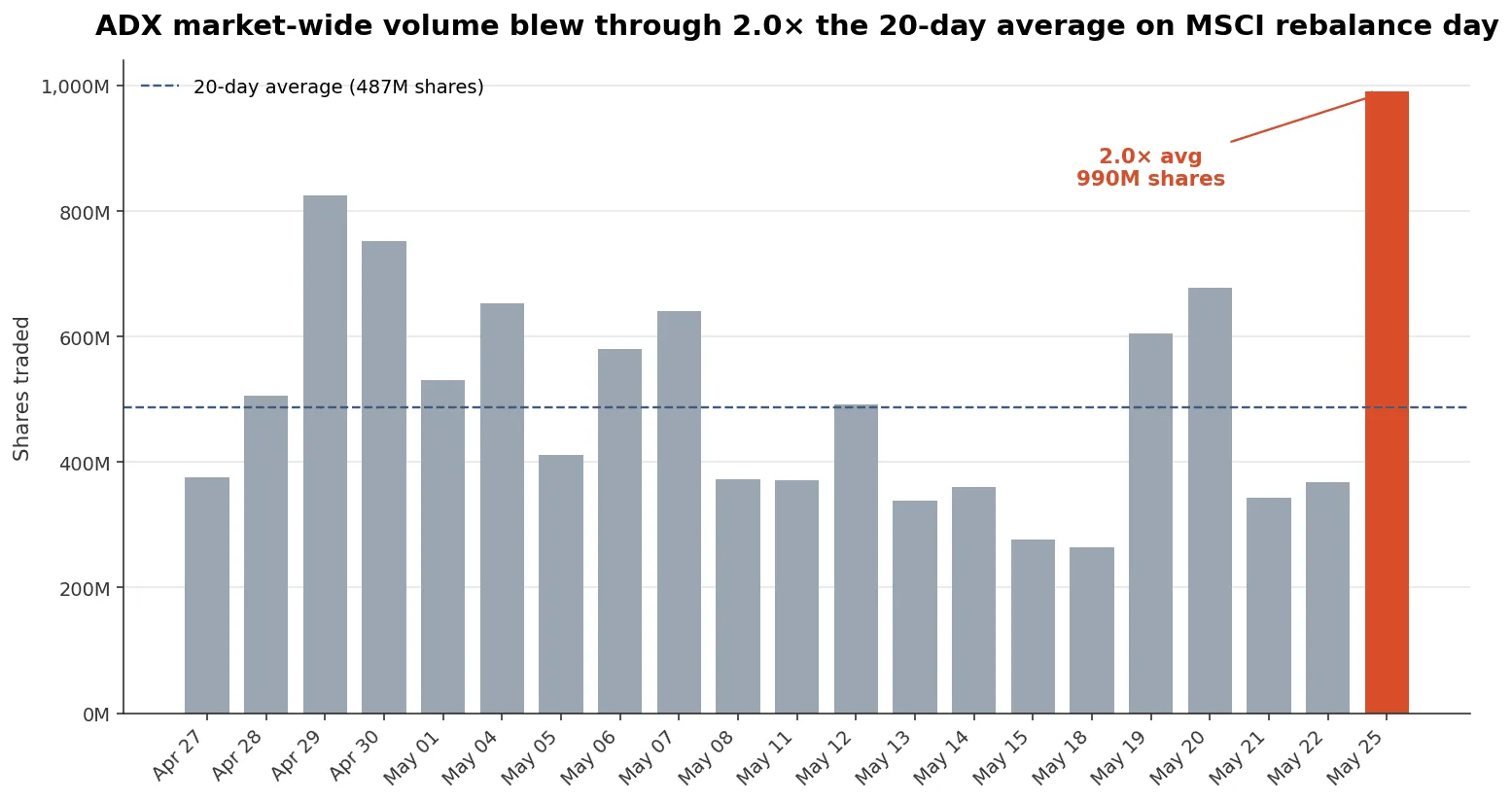

The semi-annual MSCI index rebalance landed in Abu Dhabi today, Monday May 25, 2026, a few sessions earlier than the calendar would suggest. The effective date is the first of June, which normally puts the rebalance trade on the last business day of May, but with ADX closed for Eid al-Adha from May 26 through the end of the week, May 25 became the last trading day of the month and the auction had to land here.

The footprint is impossible to miss. ADX cleared 990.3 million shares worth AED 4.50 bn in notional turnover, running 2.03× the 20-day average in share count and 3.17× the average in AED. The trailing-20-day session has been moving roughly 487.1 million shares and AED 1.42 bn, so a notional print north of three times average is the kind of session that only rebalance days produce.

The tape was more concentrated than even those headline ratios suggest, because the bulk of the print arrived in the closing auction, where passive funds tracking MSCI Emerging Markets and MSCI ACWI must transact at the same reference price on the same minute. The result is the kind of demand spike that single names rarely see outside of a tender, except today it happened simultaneously across the constituents being added, deleted, or re-weighted.

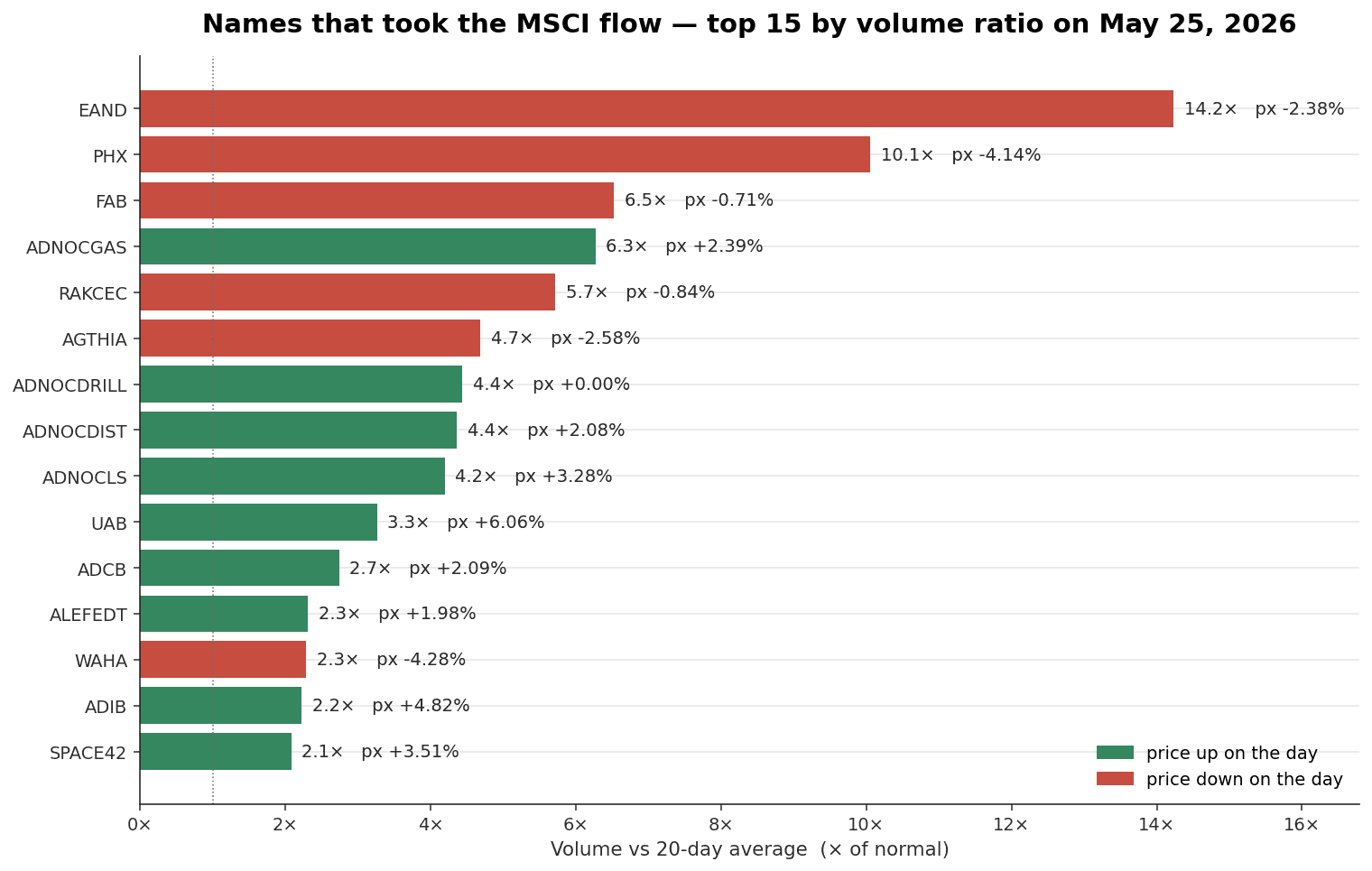

The clearest volume bursts on the day were EAND at 14.2× its 20-day pace finishing down 2.38%, PHX at 10.1× finishing down 4.14%, FAB at 6.5× finishing down 0.71%, ADNOCGAS at 6.3× finishing up 2.39%, and RAKCEC at 5.7× finishing down 0.84%.

These are the names where the rebalance arithmetic showed up most cleanly. A constituent being upweighted draws mechanical buying from every passive fund benchmarked to the index, and a deletion is met with the mirror image. Because the trades print at the close, the intraday tape often looks quiet right up until 14:45 GST, when the auction imbalance publishes and the matching engine prints in a single sweep.

These are the names where the rebalance arithmetic showed up most cleanly. A constituent being upweighted draws mechanical buying from every passive fund benchmarked to the index, and a deletion is met with the mirror image. Because the trades print at the close, the intraday tape often looks quiet right up until 14:45 GST, when the auction imbalance publishes and the matching engine prints in a single sweep.

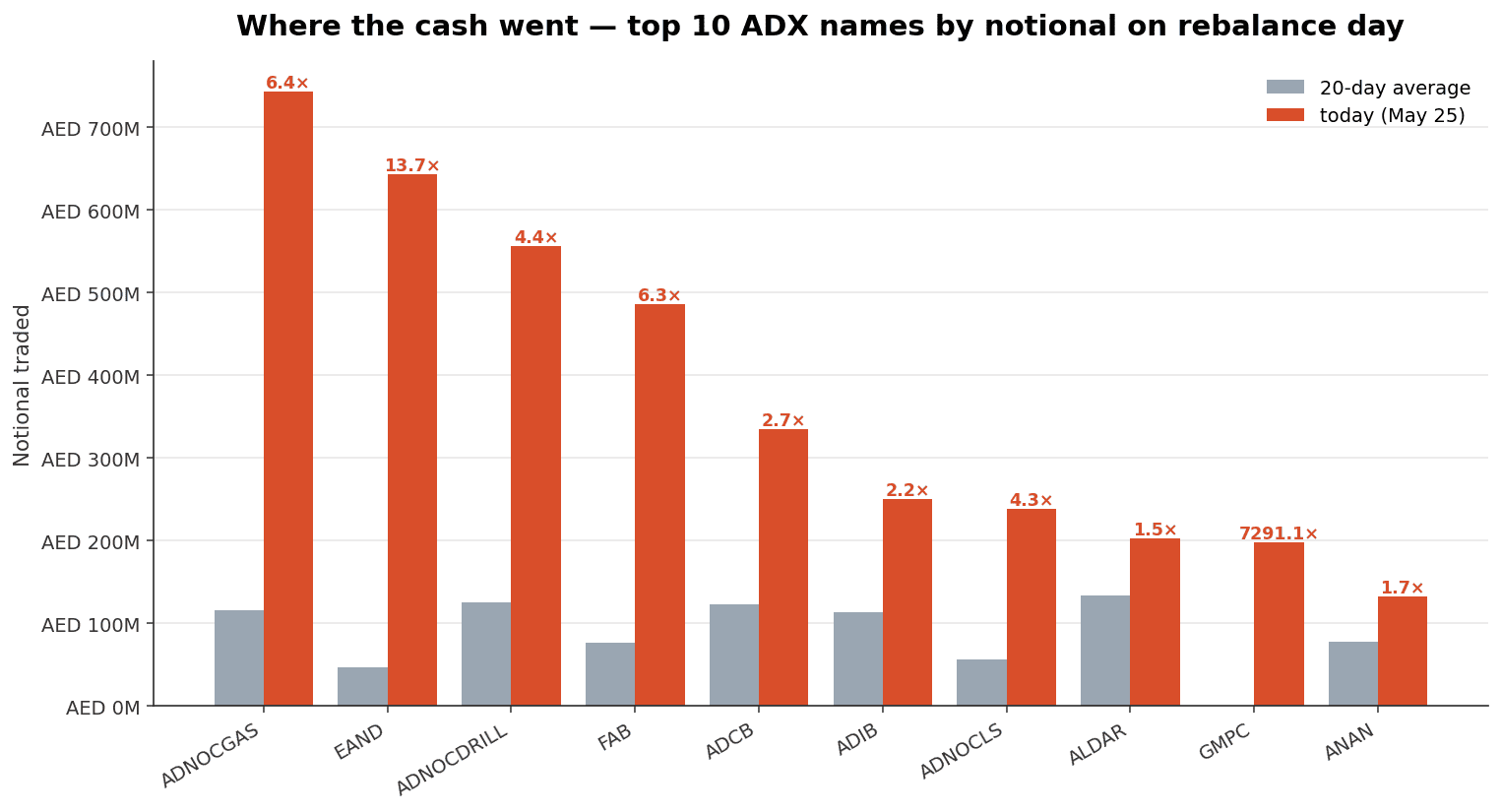

Volume ratios flatter the small names, so the absolute size of the print tells a different story. Ranked by AED notional, the top destinations of MSCI-driven flow were ADNOCGAS at AED 743 mn (6.4× average), EAND at AED 643 mn (13.7×), ADNOCDRILL at AED 556 mn (4.4×), FAB at AED 486 mn (6.3×), and ADCB at AED 335 mn (2.7×).

These are the ADX heavyweights, the names whose index weight changes by even a few basis points translate into hundreds of millions of dirhams in passive re-allocation, and they are also the names where the spread is tightest and the auction is deepest. Index providers route size through them for precisely that reason.

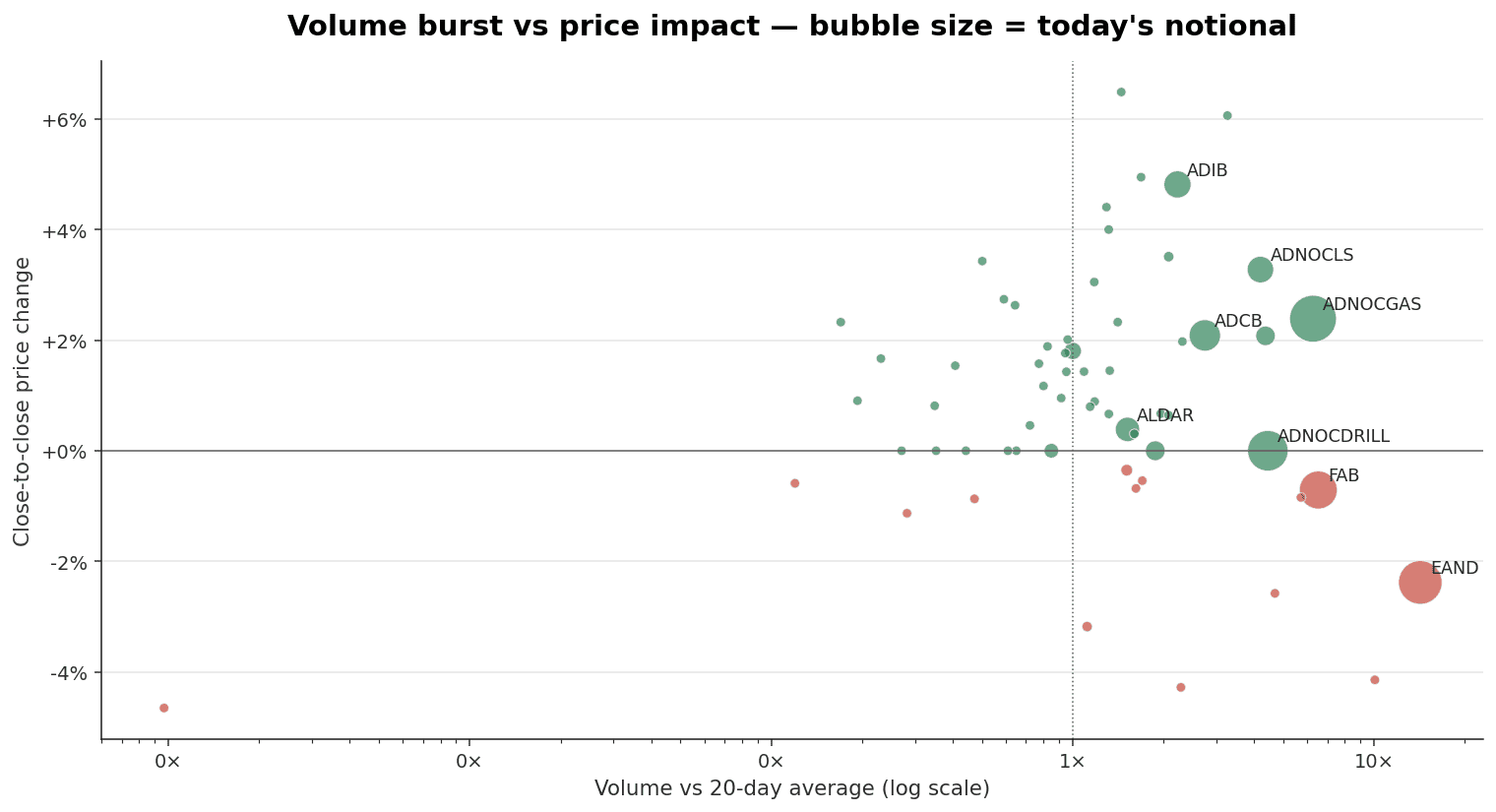

Among names with meaningful baseline liquidity, 40 finished higher, 14 finished lower, and 8 closed flat, with a median session move of +0.90%. That is a useful sanity check on the day. A rebalance is not a directional event for the market as a whole. Index-adds get bid, index-deletes get offered, and the aggregate typically cancels out.

What does not cancel out is volume, and the asymmetry between price impact and turnover is visible in the cross-section: the fattest notional prints sit close to the zero line, while the biggest percentage moves are pulled by names where the rebalance flow spiked the normal volumes.

Two patterns reliably follow a rebalance day: The session after, in this case on Monday June 1, sees partial mean-reversion in the names where price dislocated the most, as liquidity providers who absorbed the auction print work out of their positions and unwind. Daily volume on the affected lines also stays above the pre-rebalance baseline for a few sessions while index-aware arbitrageurs reconcile their books.

Both effects are tradable: the next two-to-three sessions will tell us how much of the closing print was sticky benchmark demand and how much was liquidity-provider inventory that still needs to come back out.