Three months ago, software and cybersecurity investors were pricing in something close to existential disruption. Anthropic’s expansion of Claude’s agentic coding and cybersecurity capabilities triggered a violent repricing across software, DevSecOps, and cybersecurity equities, wiping out hundreds of billions in market value in days. The fear was real, if AI agents could autonomously write, audit, secure, and fix code, entire layers of SaaS pricing power could collapse.

But markets are beginning to reassess that thesis. When Anthropic expanded Claude’s agentic coding and cybersecurity capabilities in February, investors initially treated the development as a direct threat to large parts of the SaaS and cybersecurity ecosystem.

The selloff was aggressive and indiscriminate, as markets rapidly repriced companies exposed to repetitive, rules-based workflows that AI agents could increasingly automate.

But several months later, markets are starting to differentiate between vulnerable point solutions and durable enterprise platforms.

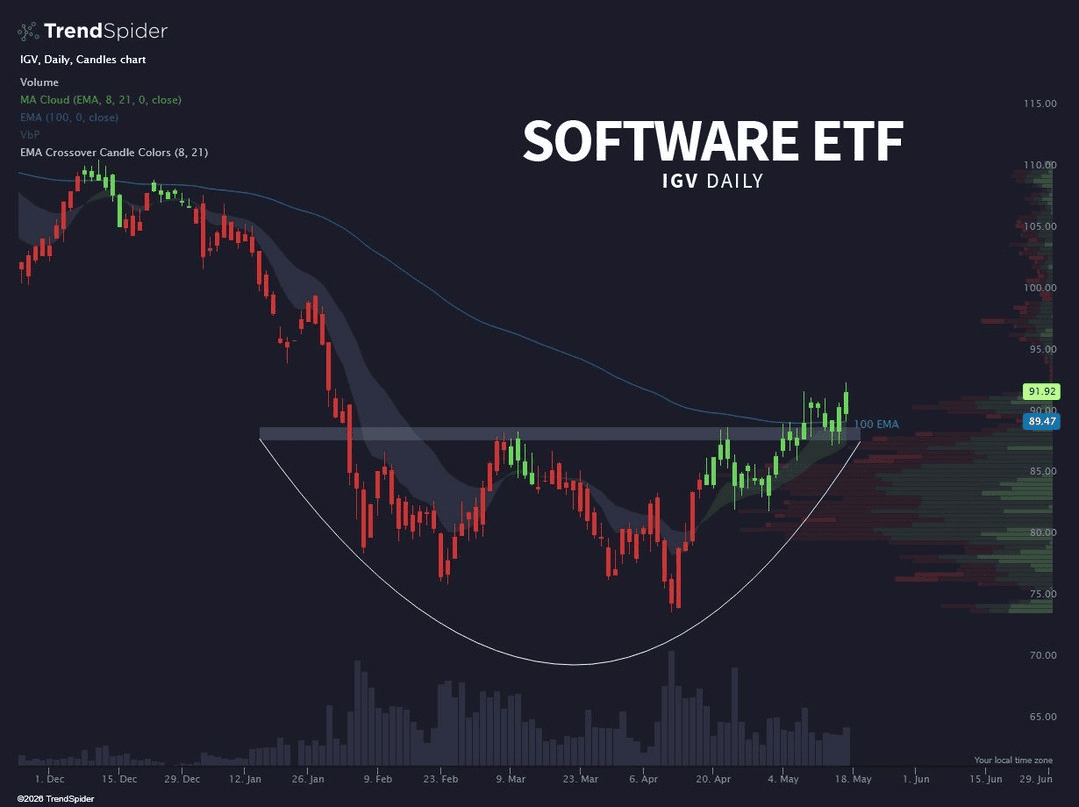

In hindsight, the February 20th selloff increasingly looks like a major buying opportunity for parts of the software sector, with the iShares Expanded Tech-Software ETF (IGV) now up roughly 15% since the panic lows.

What Happened on Feb 20th?

When Anthropic unveiled increasingly autonomous coding capabilities through Claude, investors rapidly repriced software companies most exposed to repetitive, rules-based workflows.

The selloff was severe.

On February 20 alone:

- JFrog fell 24.6%

- GitLab dropped 8.7%

- Okta lost 8.3%

- CrowdStrike declined 7.3%

- Cloudflare declined 7.1%

The broader software complex also came under pressure, with software and cybersecurity ETFs entering sharp corrections as investors reassessed long-term margins, pricing power, and enterprise software demand. At the time, the market narrative became binary where AI agents were either going to replace software companies or radically commoditize them.

The Market Is Starting to Differentiate

In February, investors largely treated software as a single trade, aggressively selling cybersecurity, DevOps, observability, and cloud-software companies under the assumption that increasingly autonomous AI agents would compress entire layers of the software stack. But several months later, markets are beginning to separate vulnerable point solutions from durable enterprise platforms.

The iShares Expanded Tech-Software ETF (IGV) has recovered materially from its March lows and recently broke above several key technical resistance levels, while software leaders tied to cloud infrastructure, enterprise workflows, and hyperscale ecosystems have started outperforming again. Institutional flows also appear to be rotating back toward AI infrastructure and platform software rather than exiting the sector altogether.

Importantly, investors are beginning to recognize that AI disruption inside software is unlikely to occur evenly.

Software Categories Facing the Most Pressure

The areas facing the greatest pressure remain software layers heavily exposed to repetitive, rules-based workflows that can be increasingly automated through agentic AI systems.

Several of these functions are rapidly becoming embedded directly into AI-native development environments offered by Anthropic, OpenAI, Microsoft GitHub Copilot, and Google rather than being sold as standalone SaaS products.

Many smaller software vendors historically relied on charging premium subscription multiples for narrowly specialized workflow tools. AI agents increasingly threaten those pricing models by collapsing multiple software functions into unified AI copilots capable of coding, reviewing, debugging, testing, and documenting simultaneously.

The repricing across parts of the software sector therefore reflects growing concerns around long-term margin compression and declining software-seat economics.

Layoffs Across AI-Exposed SaaS Companies

As agentic AI systems become more capable, several technology companies have increasingly tied layoffs and restructuring to AI-driven efficiency gains. Companies including Intuit, Meta, Salesforce, and Workday have all reduced headcount or reorganized teams while simultaneously increasing investment into AI infrastructure and automation.

The growing concern across parts of the SaaS industry is that AI agents could compress demand for standalone workflow tools, repetitive SaaS subscriptions, low-code platforms, and certain outsourced IT services by automating increasingly complex business functions directly.

Where Markets Still See Durable Value

At the same time, markets are increasingly recognizing that not all software businesses are equally exposed. Companies with deep enterprise integration, identity infrastructure, workflow ownership, cloud-scale distribution, and embedded security ecosystems continue to appear structurally more resilient than narrowly specialized point solutions.

In many cases, AI may actually strengthen incumbent platforms rather than weaken them.

The expansion of agentic AI systems is driving a parallel surge in demand for:

- compute infrastructure,

- cloud workloads,

- observability platforms,

- data governance,

- identity verification,

- cybersecurity orchestration,

- and enterprise auditability layers.

As AI systems become more autonomous, enterprises may ultimately require more oversight, monitoring, and infrastructure, not less.

That dynamic increasingly benefits hyperscale software ecosystems and integrated enterprise platforms capable of managing AI deployment at scale.

ETFs Giving Exposure to the AI Software and Cybersecurity Repricing

Investors looking to position around the evolving AI-software landscape increasingly use ETFs to gain diversified exposure across cloud software, cybersecurity, semiconductors, and AI infrastructure.

While some SaaS categories remain vulnerable to AI-driven commoditization, markets are increasingly favoring hyperscale software, cybersecurity infrastructure, semiconductors, and broader AI ecosystems powering the next phase of enterprise AI deployment.

The Bigger Investment Question

For long-term investors, that was always the more likely outcome. Markets are now beginning to separate infrastructure from commoditized tooling, durable ecosystems from vulnerable wrappers, and mission-critical enterprise platforms from narrowly specialized products.

That differentiation increasingly matters more than the initial AI panic itself.