Central banks have been among the most influential buyers of gold in recent years, helping to reshape demand for the metal at a time of elevated geopolitical risk, persistent inflation concerns and questions around the future role of the U.S. dollar in global reserves.

This year’s survey is especially notable because it recorded the highest level of central bank participation to date. Many responses were also submitted shortly after the latest escalation in the Middle East, making the findings particularly relevant for investors assessing gold’s role as a reserve asset, safe haven and portfolio diversifier.

The results point to a clear direction: central banks remain committed to gold. That matters for investors, especially as gold prices trade near multi-month lows. If official-sector demand continues, central bank buying could remain an important source of support for the gold market and may help shape the next phase of the cycle.

The Survey

The World Gold Council is a leading global authority on the gold market, providing research and insights on gold’s role as a reserve asset, portfolio diversifier and store of value. Its annual Central Bank Gold Reserves Survey, conducted with YouGov, gathers anonymous views from central banks on gold, reserve management, the U.S. dollar, inflation and geopolitical risk.

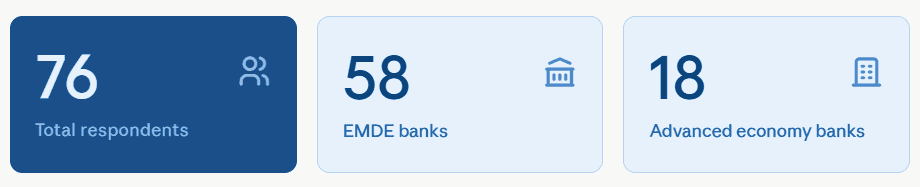

The 2026 survey recorded its highest participation in nine years, with 76 eligible central bank responses, including 58 from emerging market and developing economy central banks and 18 from advanced economy central banks. The survey offers broad coverage across geographies and gold ownership levels. Many responses were submitted after the latest escalation in the Middle East, making the findings especially relevant for investors assessing gold’s role during periods of uncertainty.

The findings

- Central banks remain bullish: Official-sector demand is expected to stay strong.

- Gold buying may continue: More central banks plan to add reserves.

- Gold is becoming strategic: Reserve managers increasingly see gold as a core asset.

- Dollar diversification supports gold: Central banks are looking beyond traditional reserve currencies.

- Gold remains a crisis hedge: Its role rises during geopolitical and financial stress

Assessing Gold Demand By Central Banks

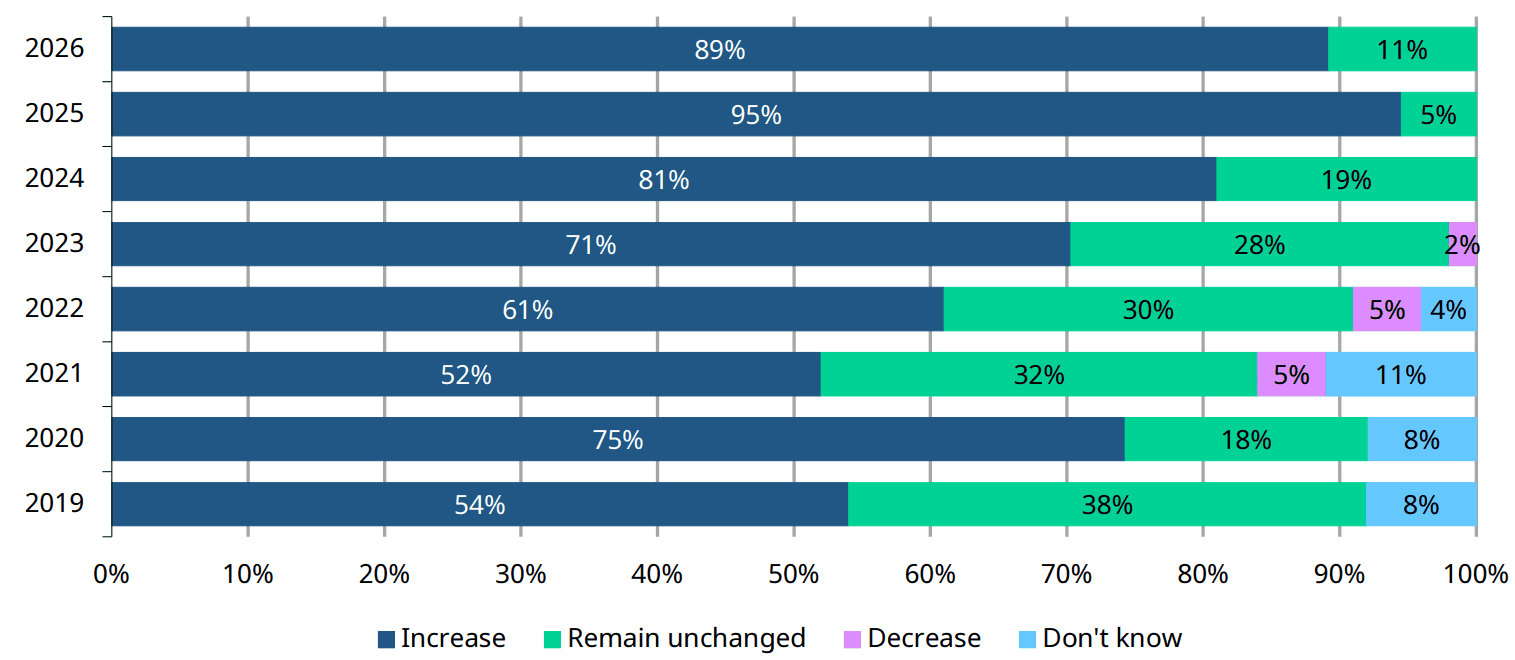

The verdict was striking: 89% of respondents expect global central bank gold reserves to increase over the next 12 months while 11% said they remain unchanged. These findings are similar to last year's. When asked if their own gold is expected to increase next year, 45% said yes while 54% said remain unchanged. The 45% is a record high for the survey.

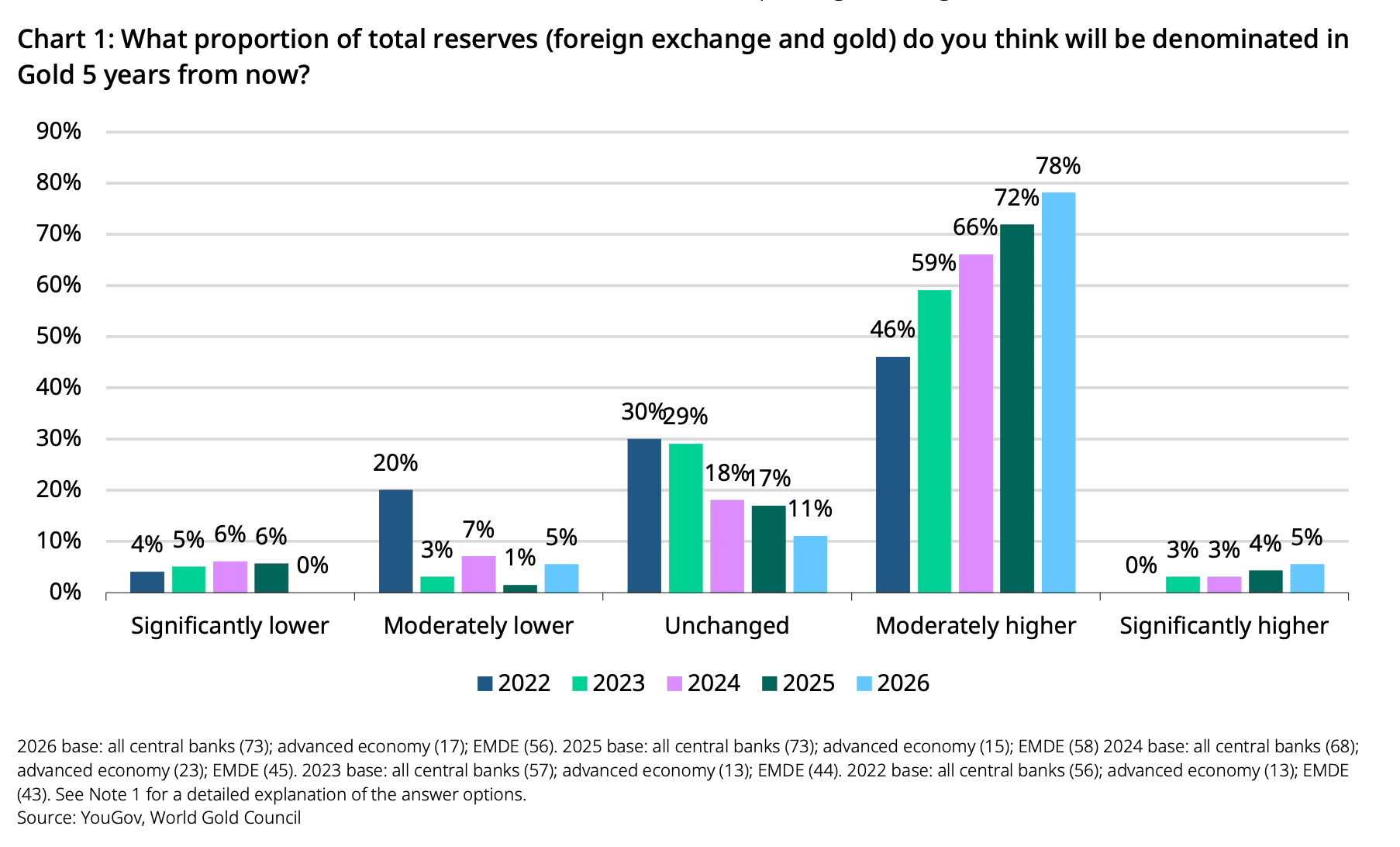

That matters because central banks buy assets for strategic reasons and often hold them for decades. When reserve managers collectively move in one direction, investors should pay attention. The survey shows that confidence in gold continues to strengthen. In 2026, 78% of respondents expected gold to represent a moderately higher share of global reserves over the next five years, up from 72% in 2025 and 46% in 2022. This steady increase suggests that central bank views on gold are becoming more positive each year, raising the likelihood that official-sector buying remains supportive for the market.

Central Banks Prioritize Gold Amid Rising Geopolitical Risks

The 2026 survey highlights that central banks continue to place significant weight on economic and geopolitical factors when managing reserves. Interest rates remain the most important consideration, while geopolitical instability has overtaken inflation concerns as a key risk factor, likely reflecting heightened tensions in the Middle East. Emerging market and developing economy (EMDE) central banks were notably more concerned about inflation, geopolitical risks, and trade conflicts than their advanced economy counterparts.

Gold continues to play a central strategic role in reserve management. Central banks overwhelmingly cited gold’s performance during times of crisis, its role as a long-term store of value, and its diversification benefits as the primary reasons for holding the metal. EMDE central banks, in particular, place greater importance on gold as a hedge against geopolitical risk. The consistency of these findings over recent years underscores gold’s enduring status as a trusted reserve asset during periods of economic uncertainty and global instability.

What does this mean for the US Dollar?

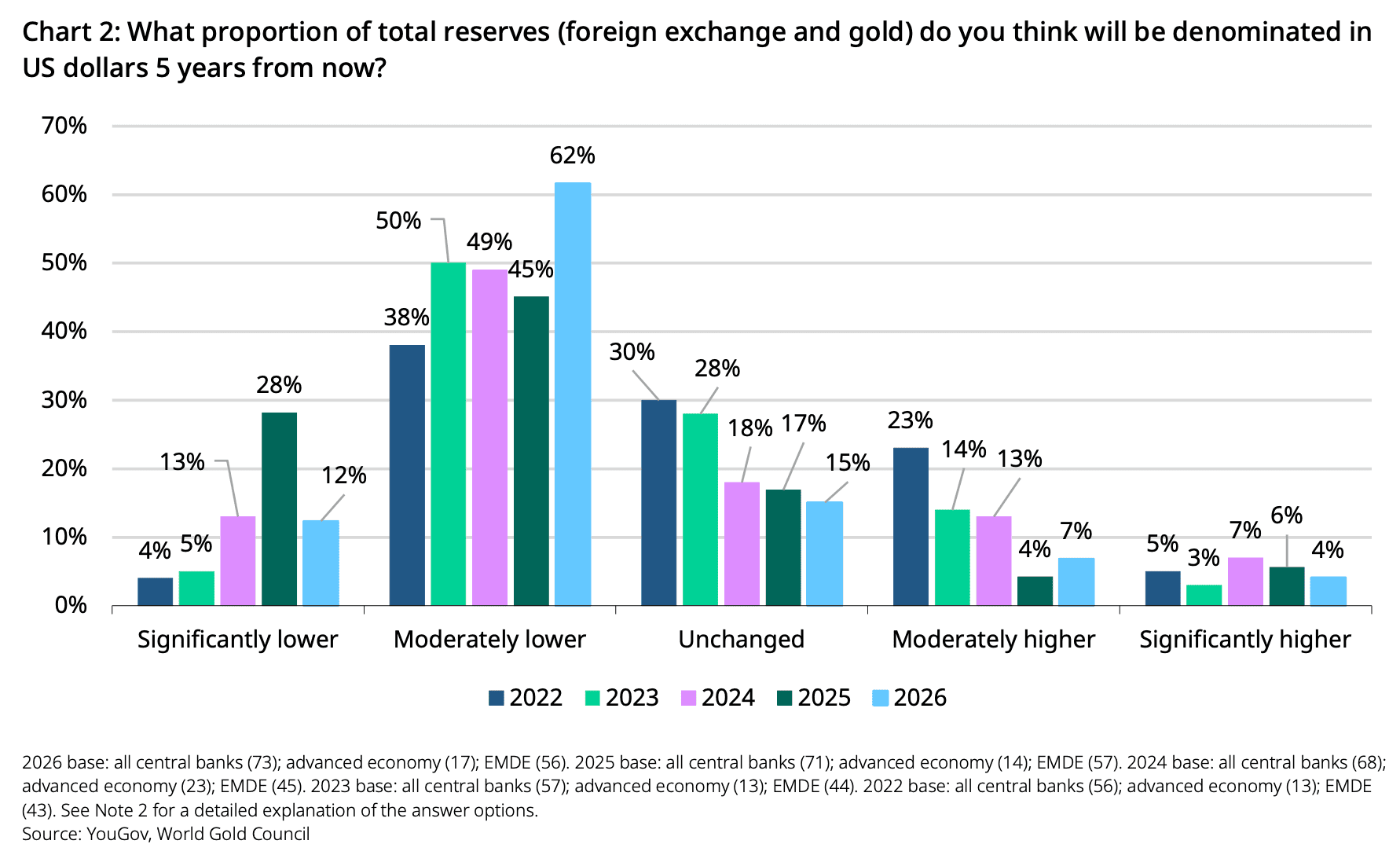

This helps explain another important finding that 74% of respondents expect the U.S. dollar's share of global reserves to decline over the next five years, while most expect gold's share to increase.

That does not mean the dollar is about to lose its status as the world's dominant reserve currency. Even central bankers acknowledge that no alternative currency currently matches the dollar's liquidity and depth. But it does suggest a gradual diversification trend that has been underway for years is continuing. Gold is emerging as one of the primary beneficiaries.

Historically, central banks were often sellers of gold. During the 1990s and early 2000s, many reduced their holdings as globalization expanded and confidence in financial markets grew. Today's environment looks very different. Rising geopolitical tensions, sanctions risks, concerns about sovereign debt, and a more fragmented global order have encouraged reserve managers to seek assets that sit outside the traditional financial system. Gold fits that description better than almost any other reserve asset.

Gold demand remains strong

If an investor is buying gold solely because central banks are accumulating it, much of that narrative is already well known. Gold prices have responded accordingly over recent years. Yet the survey suggests central bank demand is unlikely to disappear anytime soon. In fact, many institutions indicated they plan to fund new purchases by selling other reserve assets or through domestic gold-purchase programs.

Perhaps the most important takeaway is that central banks do not appear to believe the world is returning to "business as usual." If reserve managers expected geopolitical tensions, inflation concerns, and financial fragmentation to fade, they would likely slow their gold purchases. Instead, the opposite is happening. The institutions tasked with safeguarding national wealth are increasing allocations to an asset designed for uncertain times. Among respondents, 91% of those planning to buy more gold cited reserve diversification as a key motivation, while nearly 70% pointed to rising economic risks in major reserve-currency economies.

For investors, that is not necessarily a signal to rush out and buy gold. But it is a reminder that the world's most patient and influential asset allocators are positioning for a future that may look less stable, less predictable, and more multipolar than the past.

And for now, gold remains one of their preferred ways to prepare for it.