Oil prices recently surged amid escalating Middle East tensions and fears surrounding the Strait of Hormuz. The 30-year US Treasury yield climbed above 5.1%, its highest level in roughly 19 years. Inflation remains sticky, tariffs and trade tensions continue resurfacing, and geopolitical fragmentation across global supply chains has intensified.

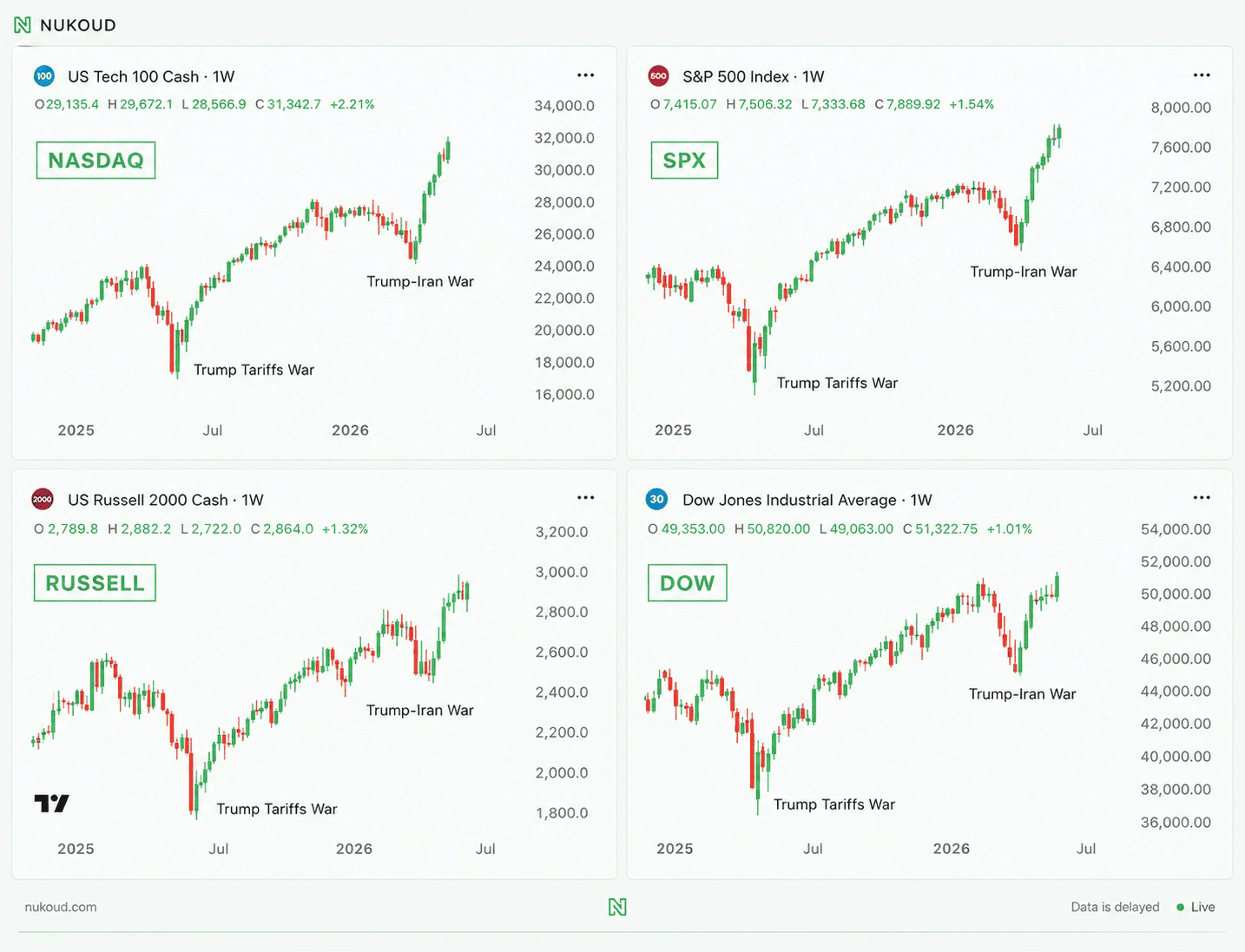

Over the past two months alone, the Nasdaq rallied roughly 28%, the S&P 500 gained around 18%, and even the small-cap Russell 2000 recovered sharply alongside the broader rally.

The question increasingly dominating Wall Street is simple:

What exactly is overpowering the macro fear trade?

Earnings Are Still Supporting the Rally

Despite concerns around slowing growth and elevated interest rates, major US companies continue posting resilient profits, particularly across technology, financials, and communication services. AI-linked infrastructure spending has certainly helped parts of the market, but the broader earnings environment has also remained far stronger than many investors expected earlier this year.

Nvidia’s recent results became symbolic of that strength. The company reported quarterly revenue of approximately $81.6 billion, up 85% year-over-year, while operating cash flow surged 147% to roughly $53.5 billion. The scale of those numbers reinforced the idea that AI infrastructure spending is not slowing despite broader macro concerns.

Importantly, however, the rally is no longer concentrated only in Nvidia or semiconductors. Market participation has broadened across software, industrials, financials, utilities, and even select consumer names.

That broadening has helped markets sustain momentum rather than relying on a handful of mega-cap stocks alone.

Buybacks Are Flooding the Market With Demand

US companies are once again repurchasing shares at an extraordinary pace, with total announced buybacks this year already approaching record levels. Large technology firms, banks, energy companies, and industrial firms continue deploying enormous amounts of cash toward share repurchases, effectively creating structural demand underneath the market.

Nvidia alone recently announced an additional $80 billion buyback authorization.

This matters because buybacks reduce available share supply while simultaneously supporting earnings-per-share growth, often helping equities remain resilient even during periods of elevated macro uncertainty.

Markets Are Betting Growth Will Hold Up

The current rally also reflects growing investor confidence that the US economy may avoid a deep recession despite elevated rates and persistent inflation pressures.

Labor markets remain relatively stable, consumer spending has held up better than expected, and corporate balance sheets across many sectors remain healthy. At the same time, investors increasingly believe the Federal Reserve may eventually move toward rate cuts if inflation continues stabilizing later this year.

That combination has created an environment where markets are increasingly willing to look through short-term macro shocks in favor of longer-term earnings and liquidity trends.

Risks Have Not Disappeared

Valuations across parts of the market have become increasingly stretched, Treasury yields remain elevated, geopolitical tensions could escalate further, and the market is still heavily dependent on continued earnings resilience from major technology companies.

But for now, markets appear comfortable making one very large bet:

that corporate earnings, buybacks, liquidity, and structural investment trends can continue overpowering inflation, geopolitics, and recession fears.